ARTICLES

Explore our latest insights on the beauty, luxury, and lifestyle industries. At Carrara Advisory, we combine decades of hands-on experience with deep market understanding to provide actionable perspectives on strategy, innovation, and growth. Here, we share our thinking on the trends, challenges, and opportunities shaping the future of your business.

Search by Category

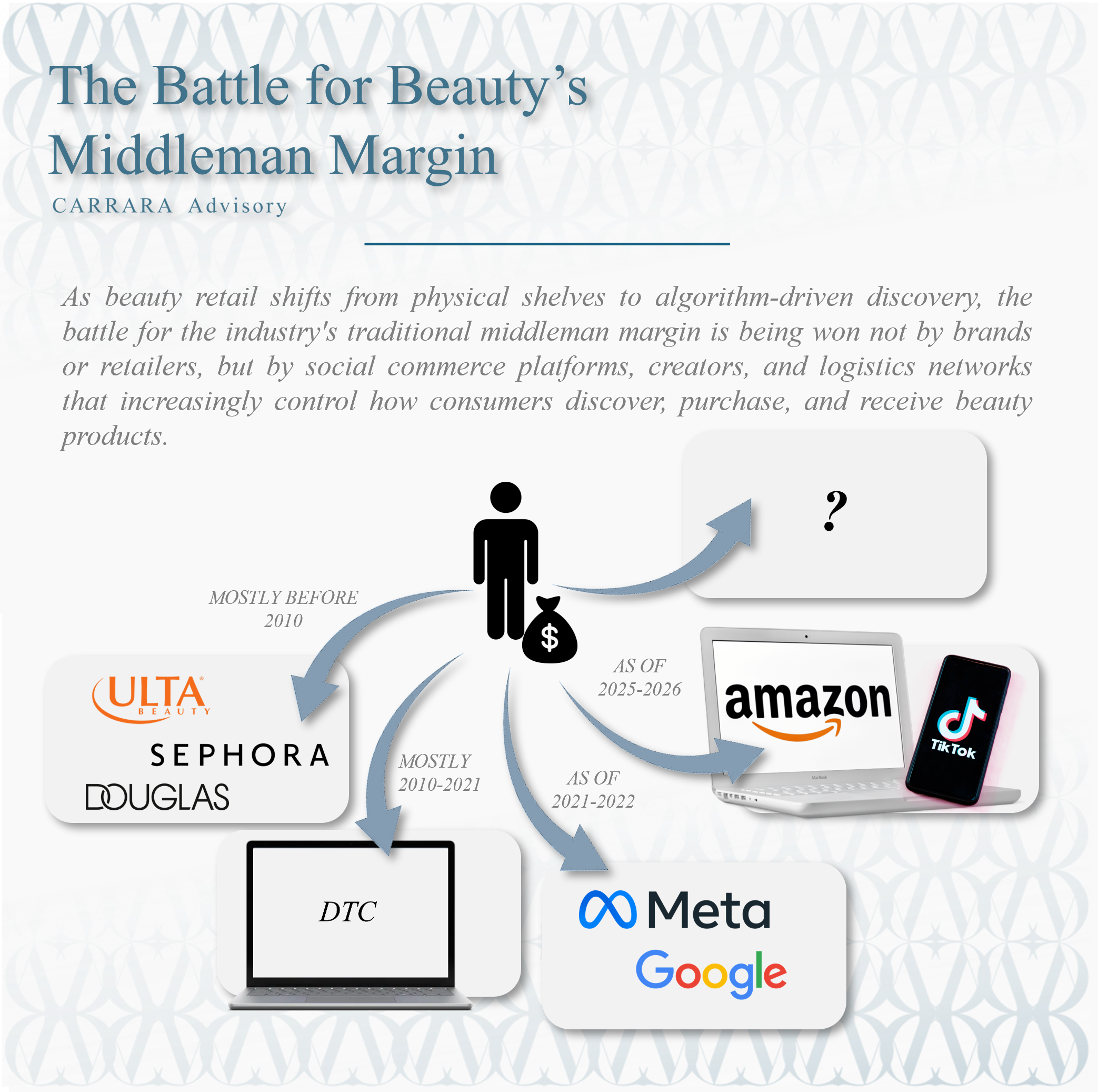

The Battle for Beauty's Middleman Margin

As beauty retail shifts from physical shelves to algorithm-driven discovery, the battle for the industry's traditional middleman margin is being won not by brands or retailers, but by social commerce platforms, creators, and logistics networks that increasingly control how consumers discover, purchase, and receive beauty products.

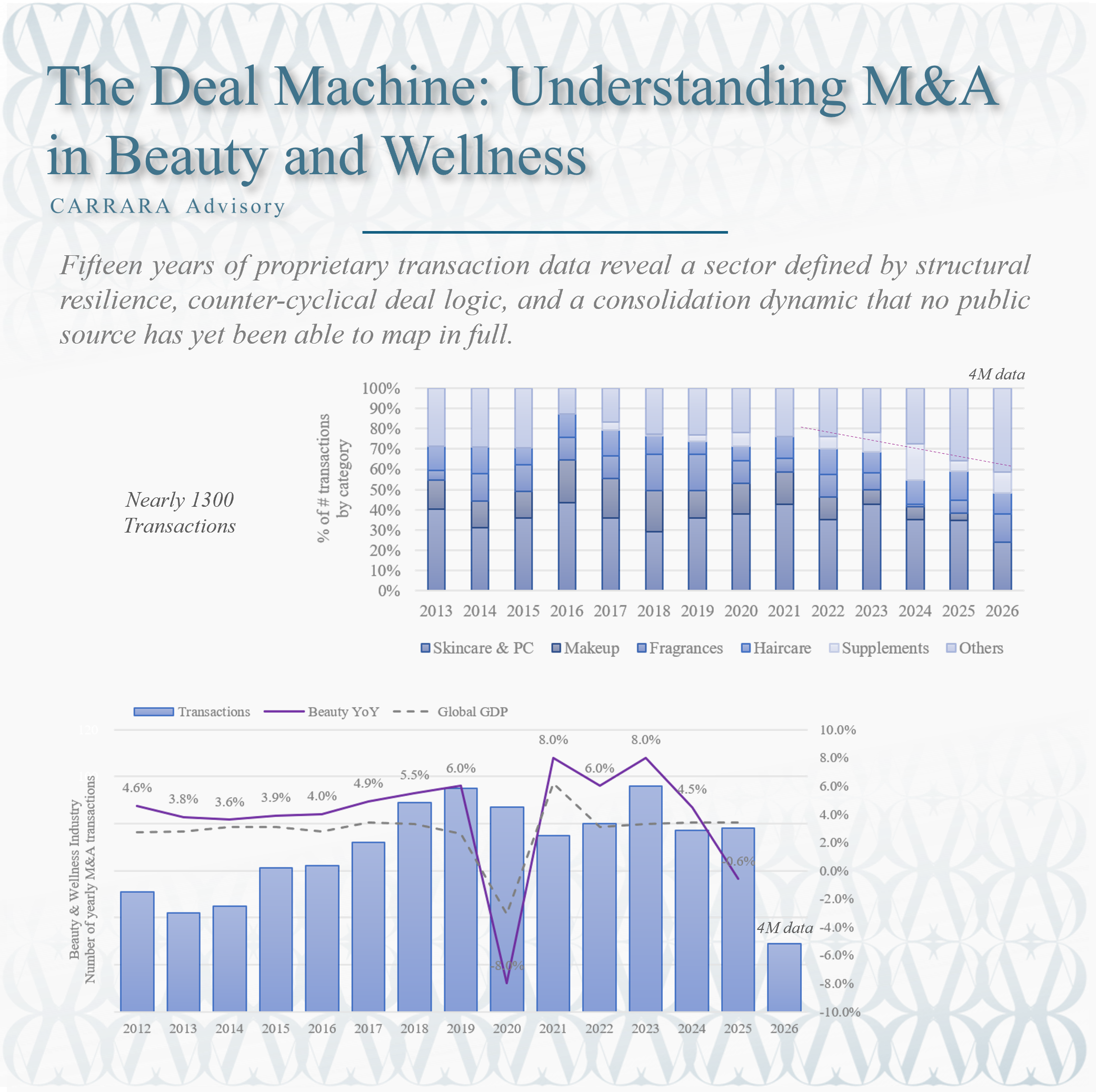

The Deal Machine: Understanding M&A in Beauty and Wellness

Fifteen years of proprietary transaction data reveal a sector defined by structural resilience, counter-cyclical deal logic, and a consolidation dynamic that no public source has yet been able to map in full.

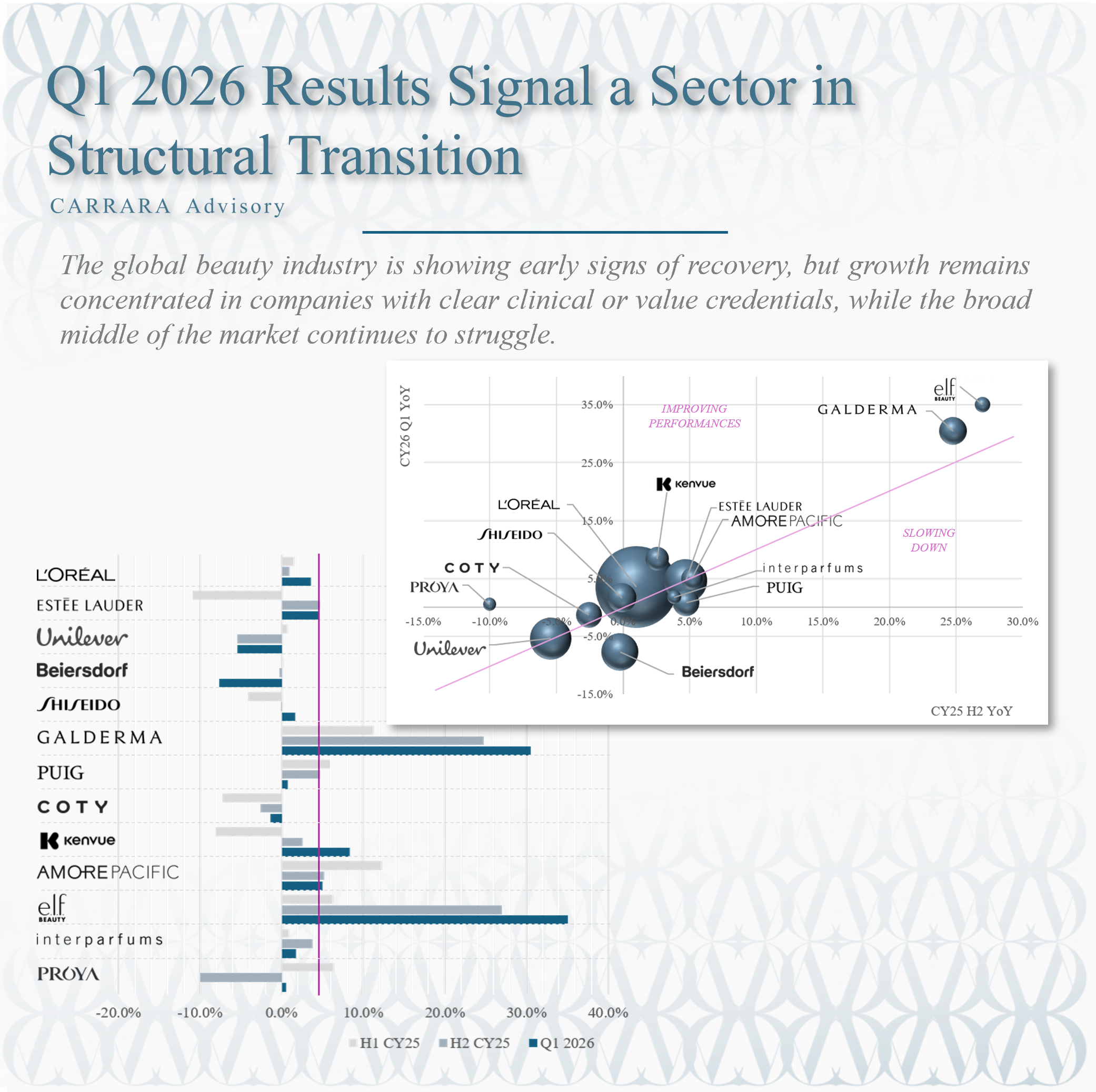

Q1 2026 Results Signal a Sector in Structural Transition

The global beauty industry is showing early signs of recovery, but growth remains concentrated in companies with clear clinical or value credentials, while the broad middle of the market continues to struggle.

Beauty Private Label Beauty: Success Stories, Innovations, and Award-Winning Products

Retailer-owned beauty brands have moved from cheap alternatives to genuine market leaders, with proof points ranging from No7 outscoring Chanel and Dior on UK brand health metrics to Kirkland Signature generating $86 billion in annual sales.

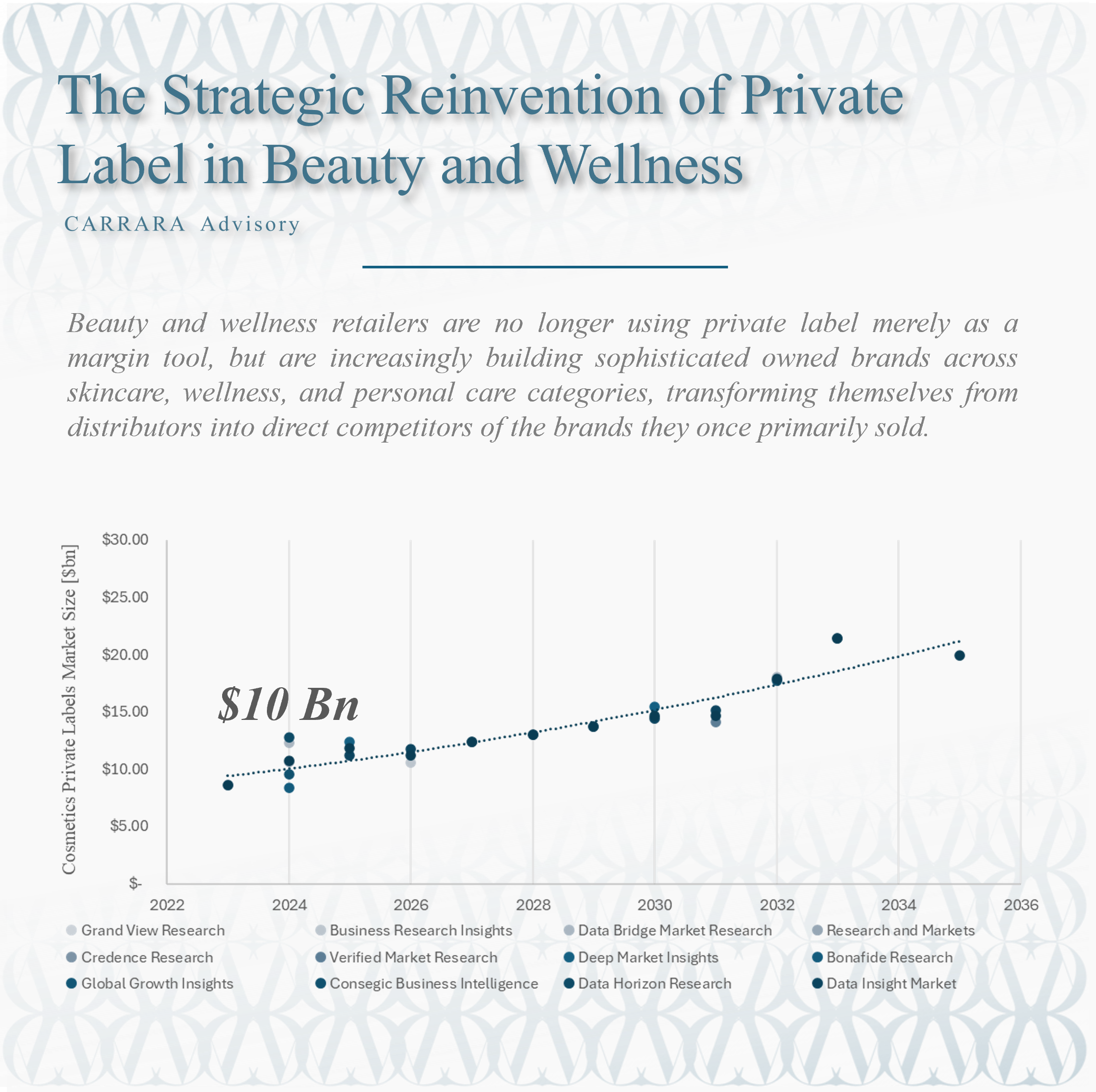

The Strategic Reinvention of Private Label in Beauty and Wellness

Beauty and wellness retailers are no longer using private label merely as a margin tool, but are increasingly building sophisticated owned brands across skincare, wellness, and personal care categories, transforming themselves from distributors into direct competitors of the brands they once primarily sold.

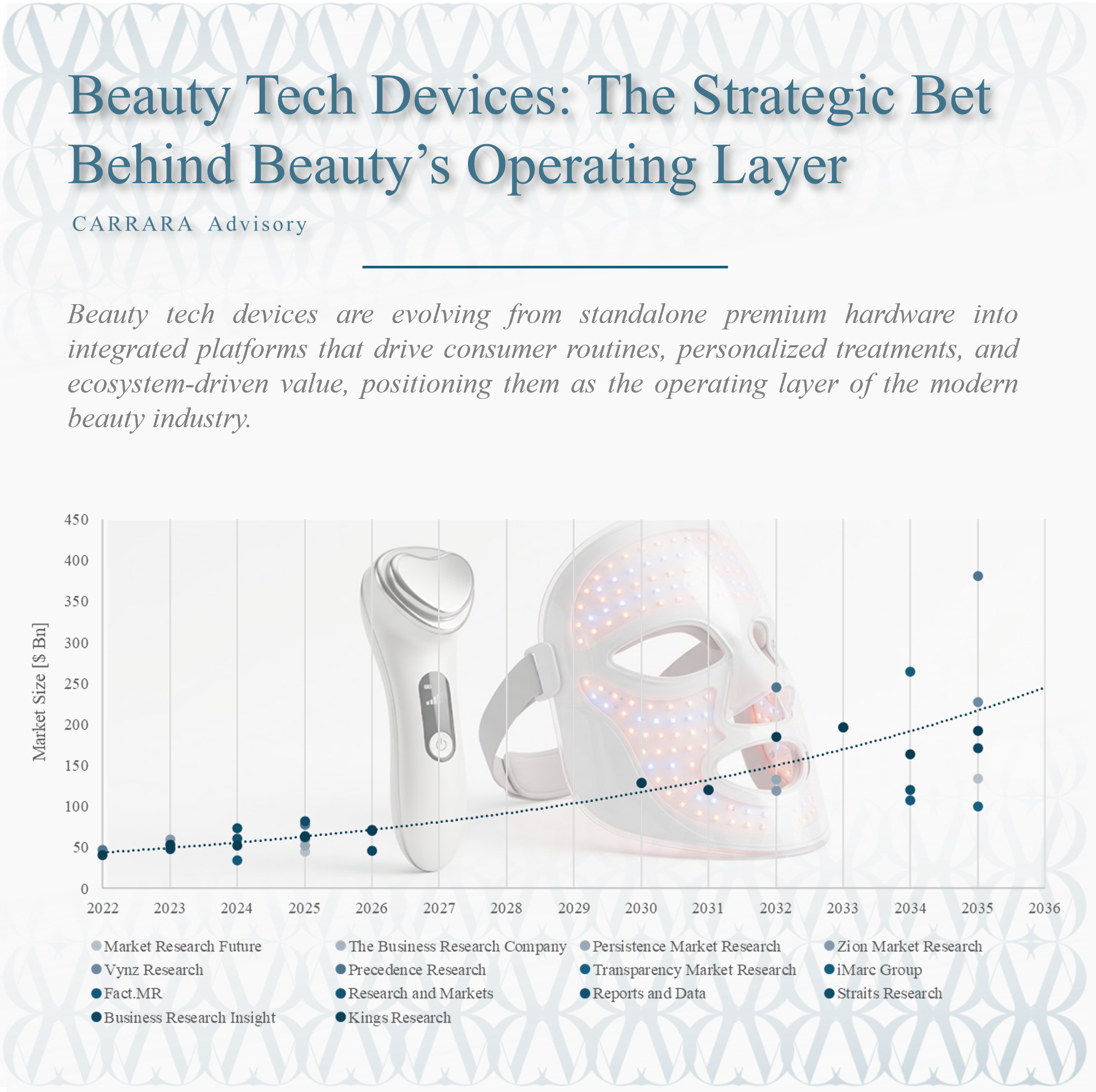

Beauty Tech Devices: The Strategic Bet Behind Beauty’s Operating Layer

Beauty tech devices are evolving from standalone premium hardware into integrated platforms that drive consumer routines, personalized treatments, and ecosystem-driven value, positioning them as the operating layer of the modern beauty industry.

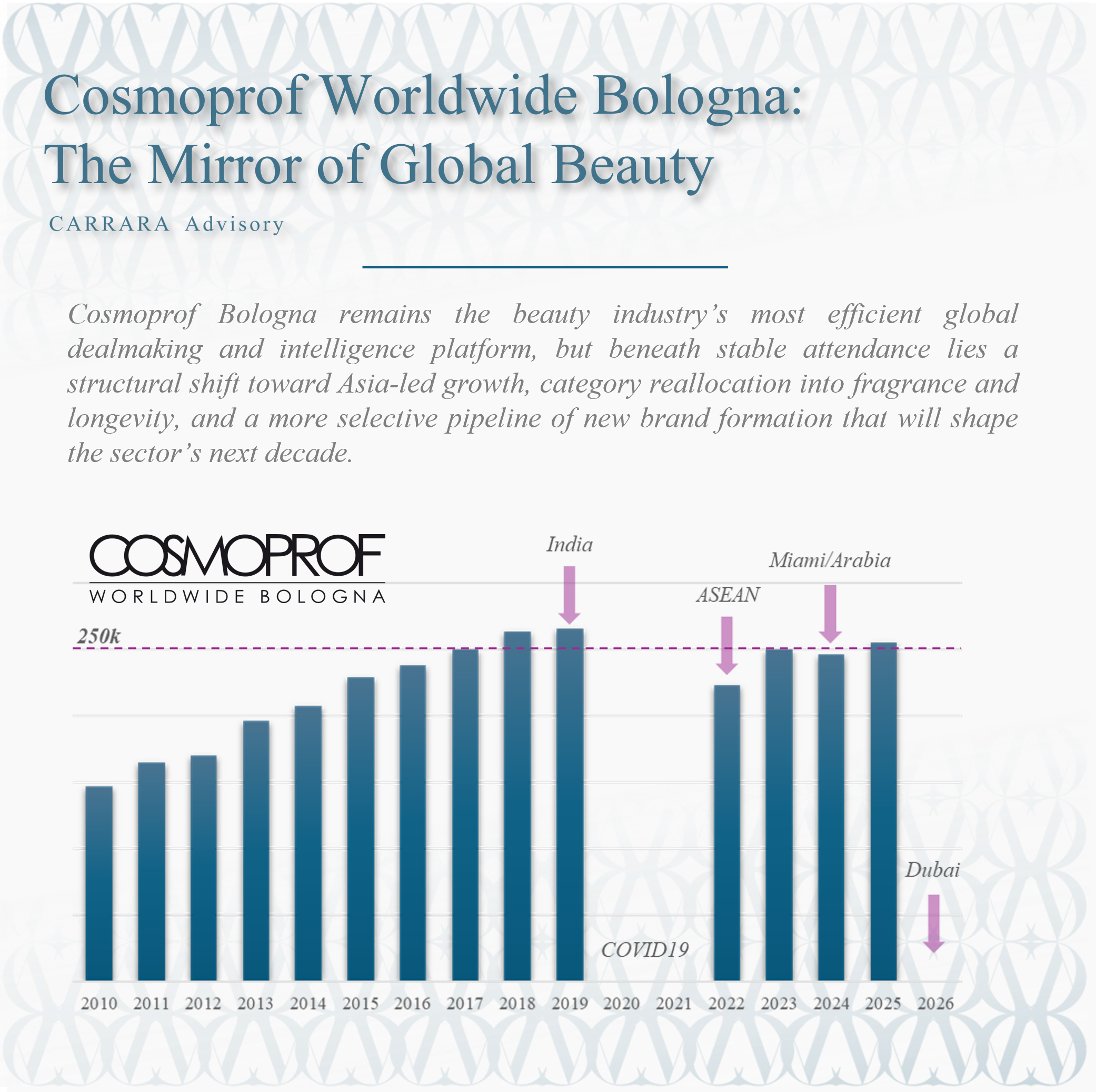

Cosmoprof Worldwide Bologna: The Mirror of Global Beauty

Cosmoprof Bologna remains the beauty industry’s most efficient global dealmaking and intelligence platform, but beneath stable attendance lies a structural shift toward Asia-led growth, category reallocation into fragrance and longevity, and a more selective pipeline of new brand formation that will shape the sector’s next decade.

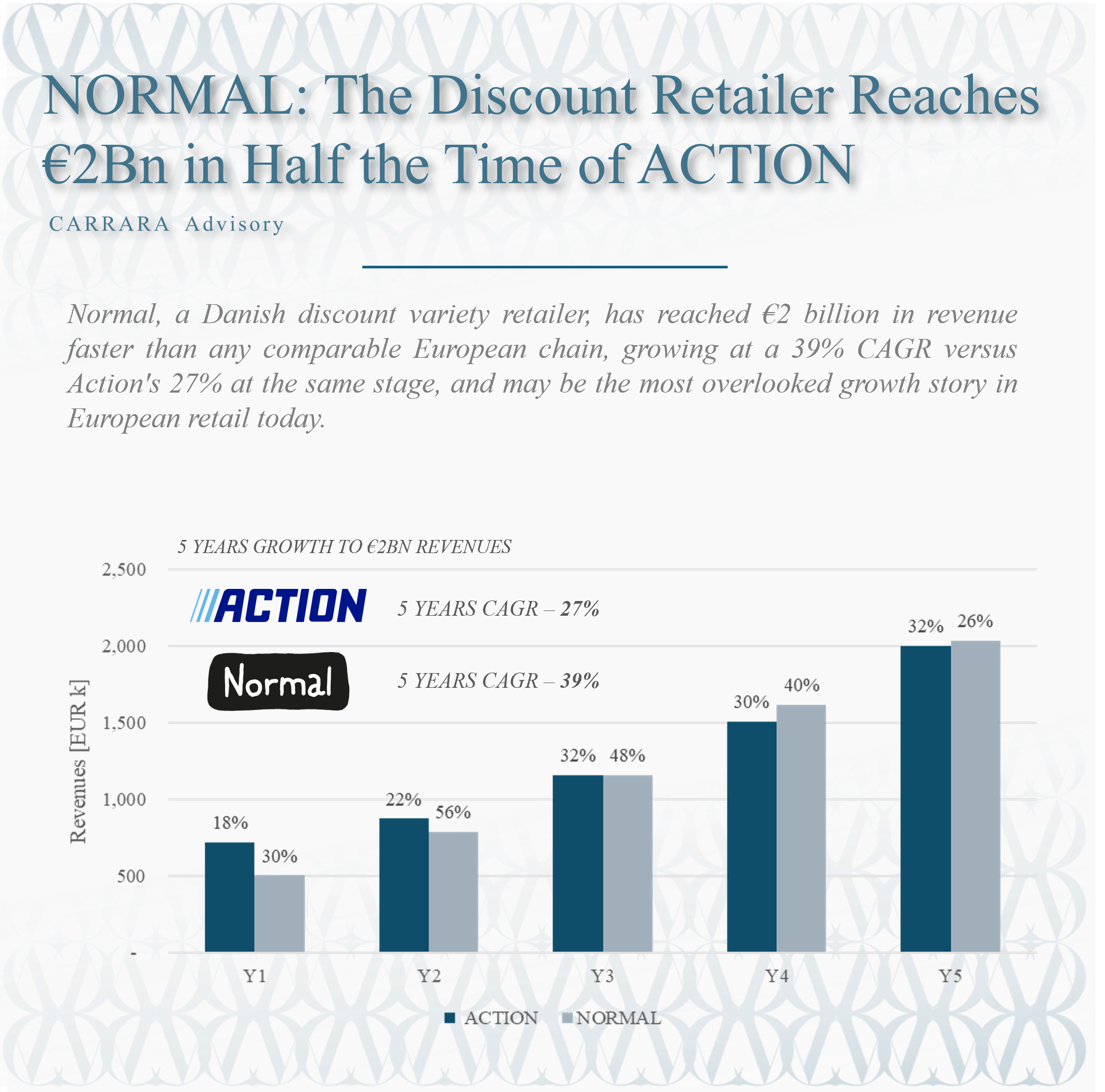

NORMAL: The Discount Retailer Reaches €2Bn in Half the Time of ACTION

Normal, a Danish discount variety retailer, has reached €2 billion in revenue faster than any comparable European chain, growing at a 39% CAGR versus Action's 27% at the same stage, and may be the most overlooked growth story in European retail today.

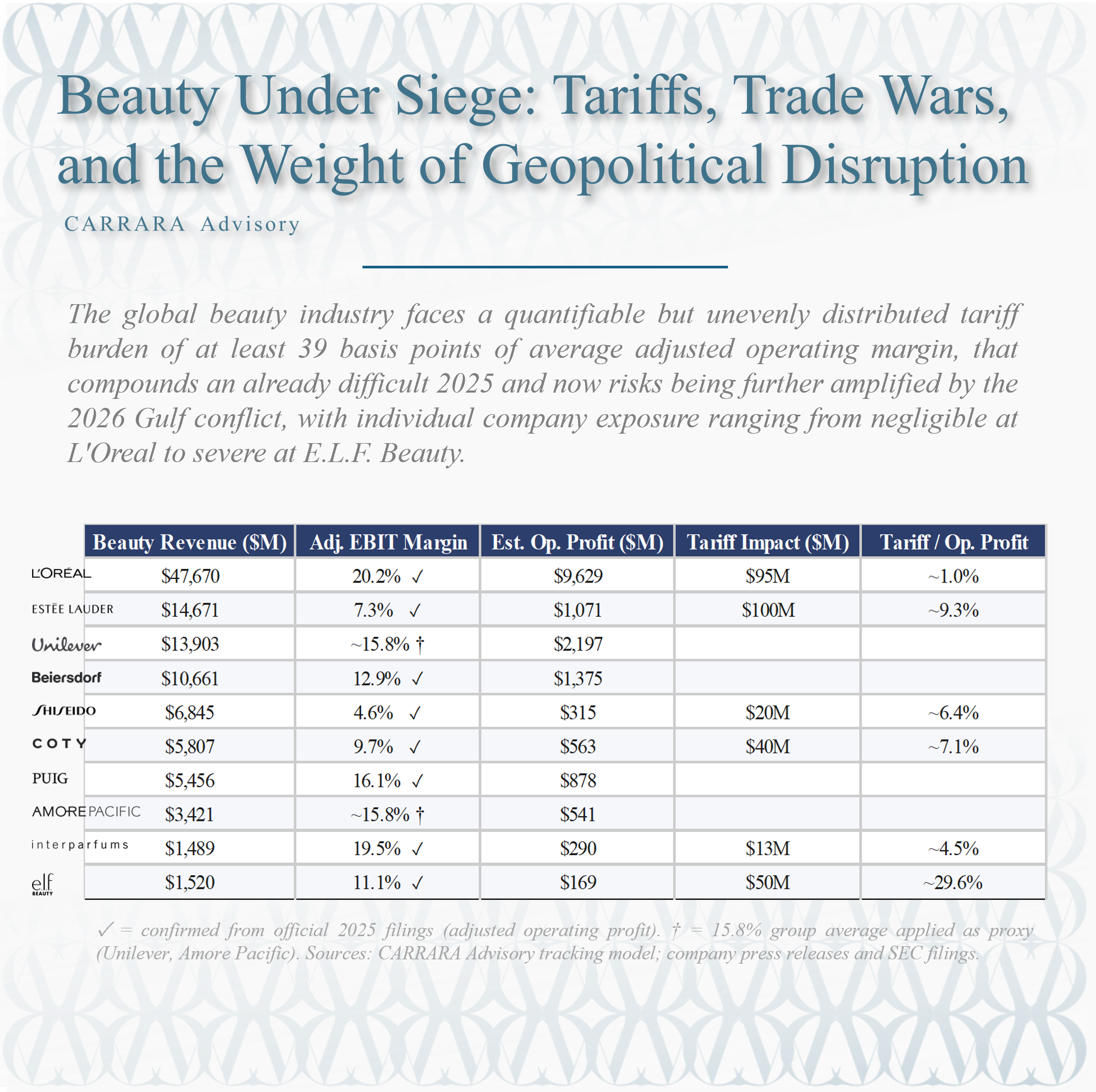

Beauty Under Siege: Tariffs, Trade Wars, and the Weight of Geopolitical Disruption

The global beauty industry faces a quantifiable but unevenly distributed tariff burden of at least 39 basis points of average adjusted operating margin, that compounds an already difficult 2025 and now risks being further amplified by the 2026 Gulf conflict, with individual company exposure ranging from negligible at L'Oreal to severe at E.L.F. Beauty.

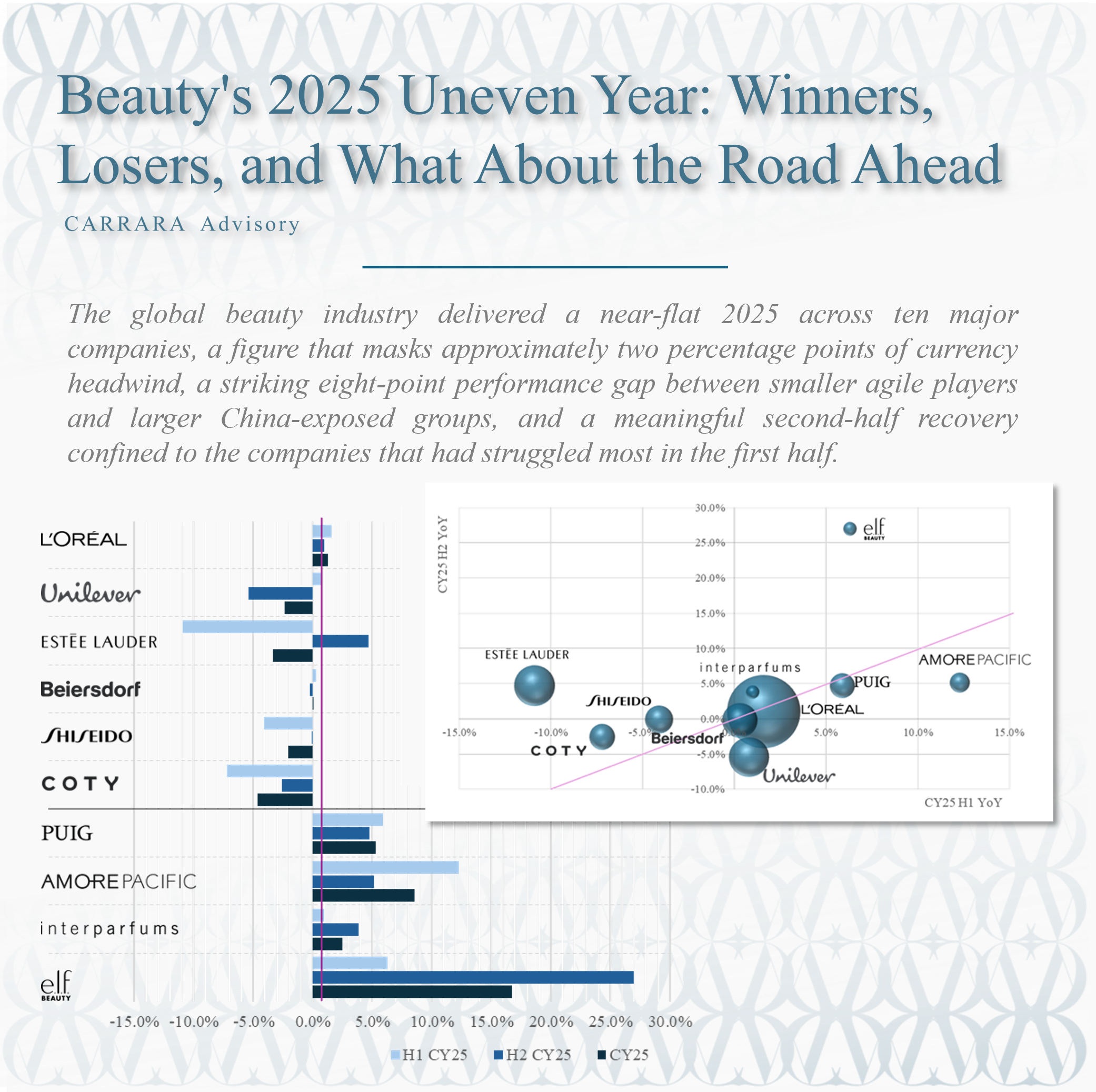

Beauty's 2025 Uneven Year: Winners, Losers, and What About the Road Ahead

The global beauty industry delivered a near-flat 2025 across ten major companies, a figure that masks approximately two percentage points of currency headwind, a striking eight-point performance gap between smaller agile players and larger China-exposed groups, and a meaningful second-half recovery confined to the companies that had struggled most in the first half.

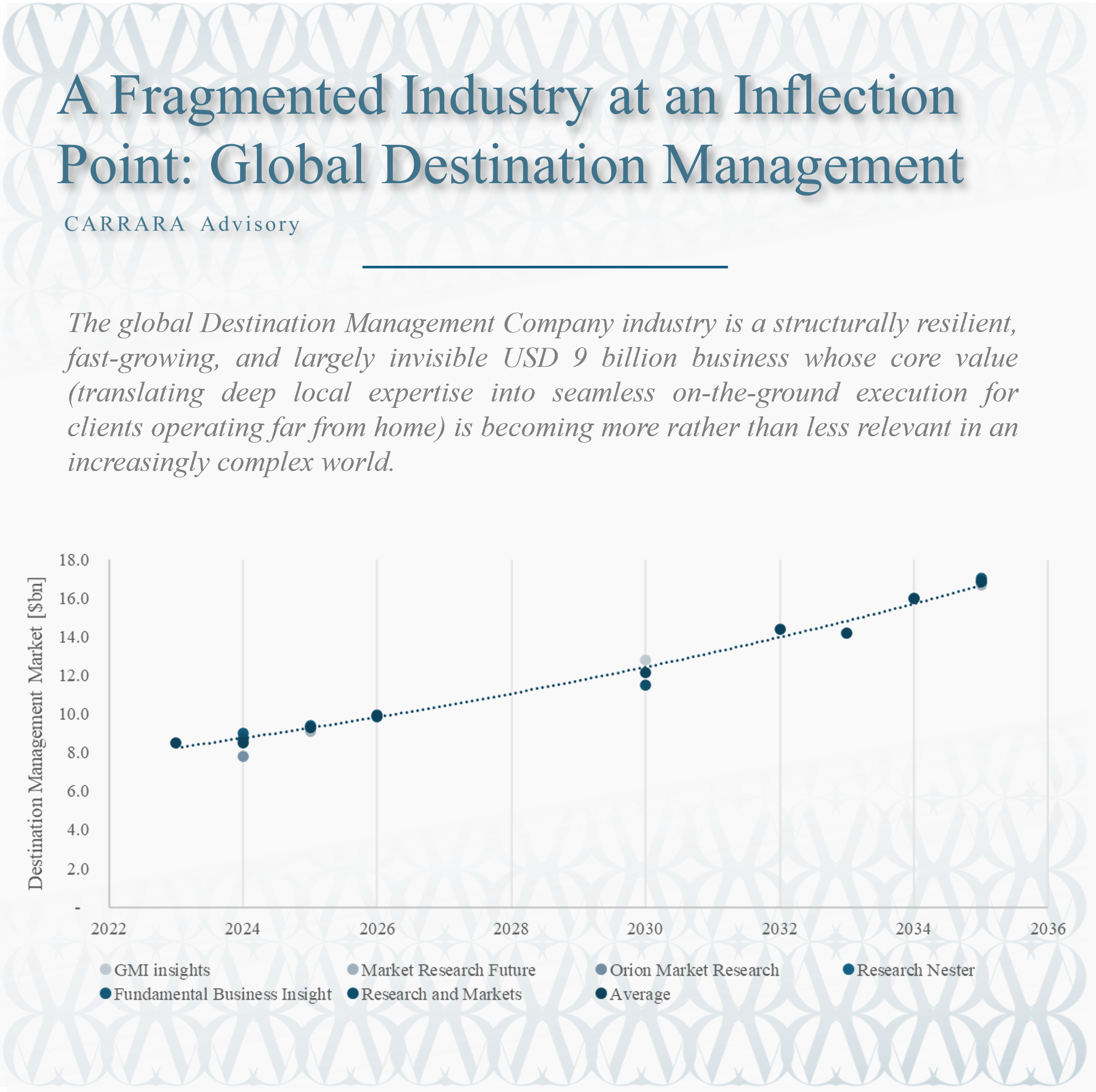

A Fragmented Industry at an Inflection Point: Global Destination Management

The global Destination Management Company industry is a structurally resilient, fast-growing, and largely invisible USD 9 billion business whose core value (translating deep local expertise into seamless on-the-ground execution for clients operating far from home) is becoming more rather than less relevant in an increasingly complex world.

Switzerland's Contract Beauty Manufacturing Ecosystem: Who's Building the World's Premium Skincare

Switzerland's "Swiss made" label unites a surprisingly diverse contract beauty manufacturing ecosystem of fifteen-plus operators, and for brands, choosing between them is less a procurement decision than a strategic one, where the wrong partner can cost as much as the right one can build.

The Great Beauty Portfolio Reset - When Divestiture Becomes the Growth Strategy

The beauty industry is undergoing a structural reset in which large groups like Estée Lauder and Coty are divesting mid-tier, makeup-heavy, marketing-dependent brands that no longer fit their economic and strategic models, signalling a broader shift toward smaller, more focused portfolios built around brands with clear positioning, defensibility, and sustainable growth.

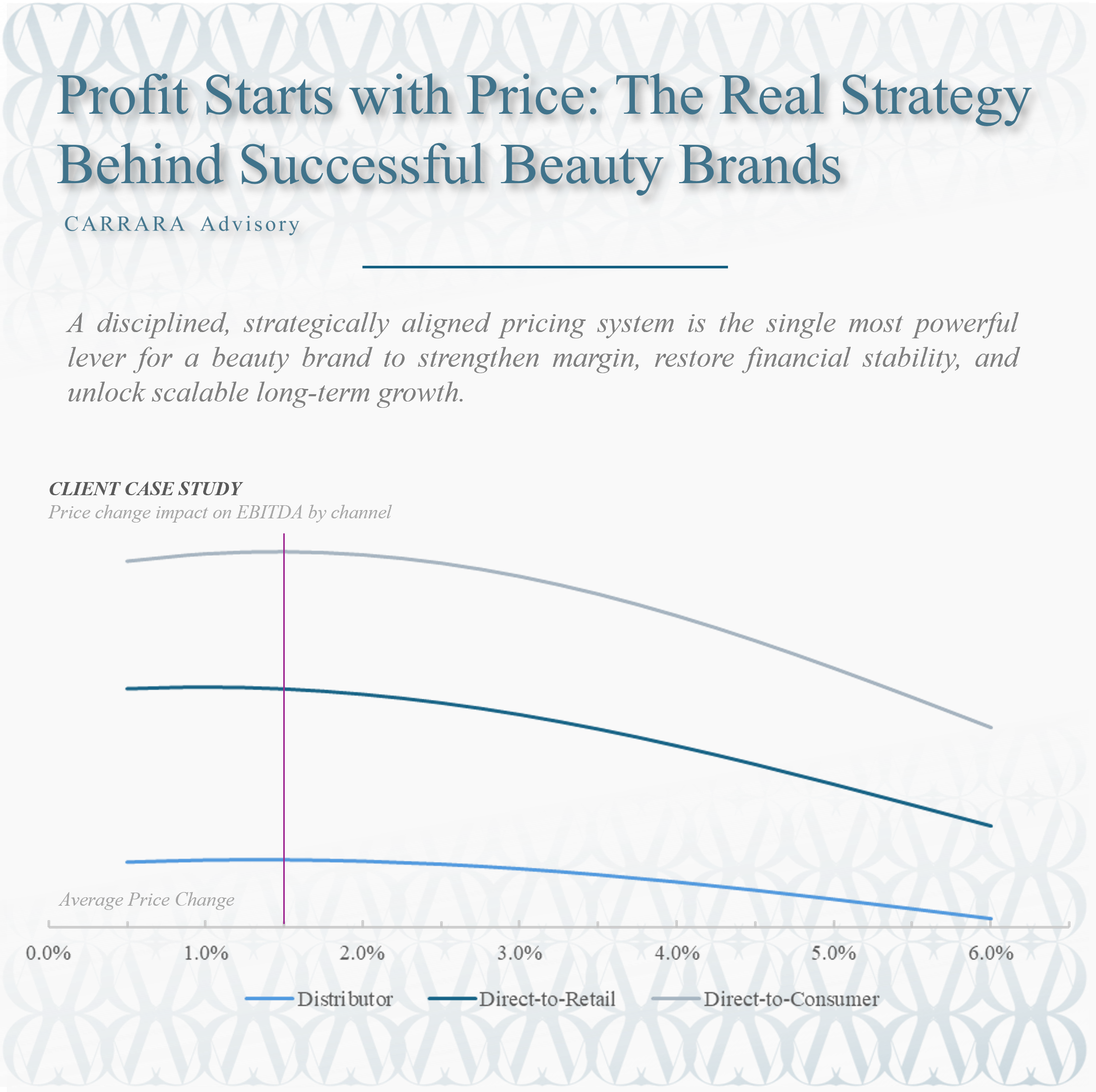

Profit Starts with Price: The Real Strategy Behind Successful Beauty Brands

A disciplined, strategically aligned pricing system is the single most powerful lever for a beauty brand to strengthen margin, restore financial stability, and unlock scalable long-term growth.

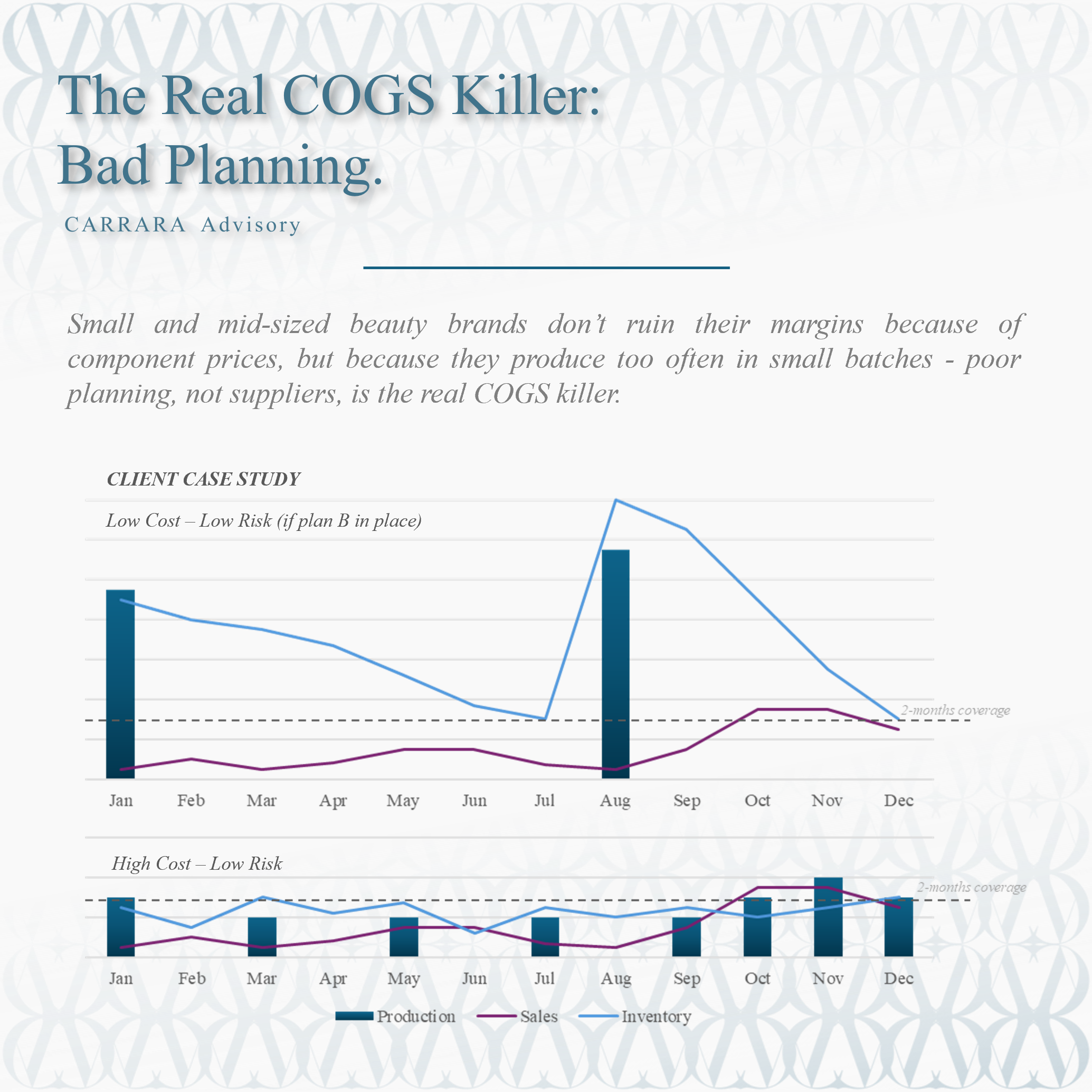

The Real COGS Killer: Bad Planning.

Small and mid-sized beauty brands don’t ruin their margins because of component prices, but because they produce too often in small batches - poor planning, not suppliers, is the real COGS killer.

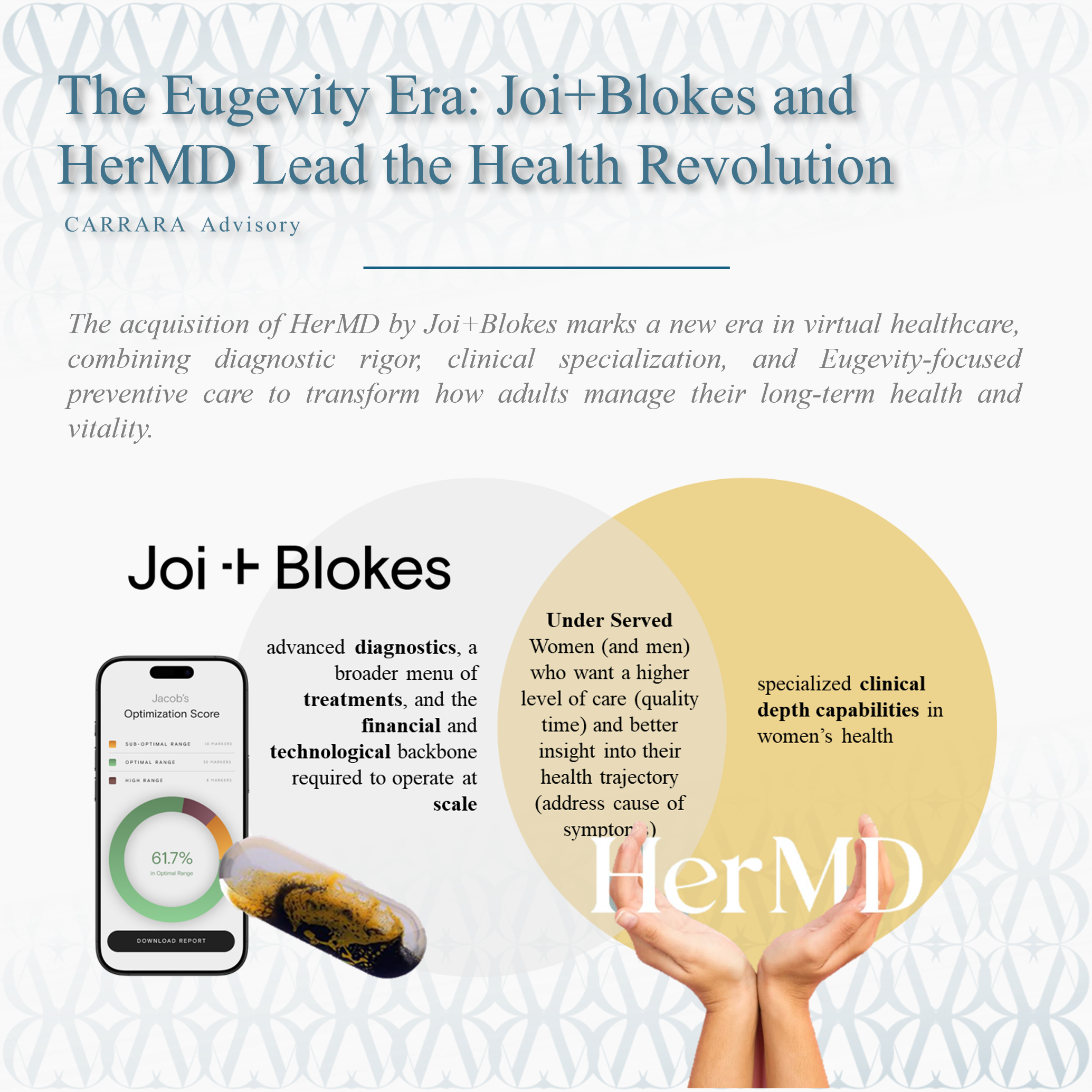

The Eugevity Era: Joi+Blokes and HerMD Lead the Health Revolution

The acquisition of HerMD by Joi+Blokes marks a new era in virtual healthcare, combining diagnostic rigor, clinical specialization, and Eugevity‑focused preventive care to transform how adults manage their long-term health and vitality.

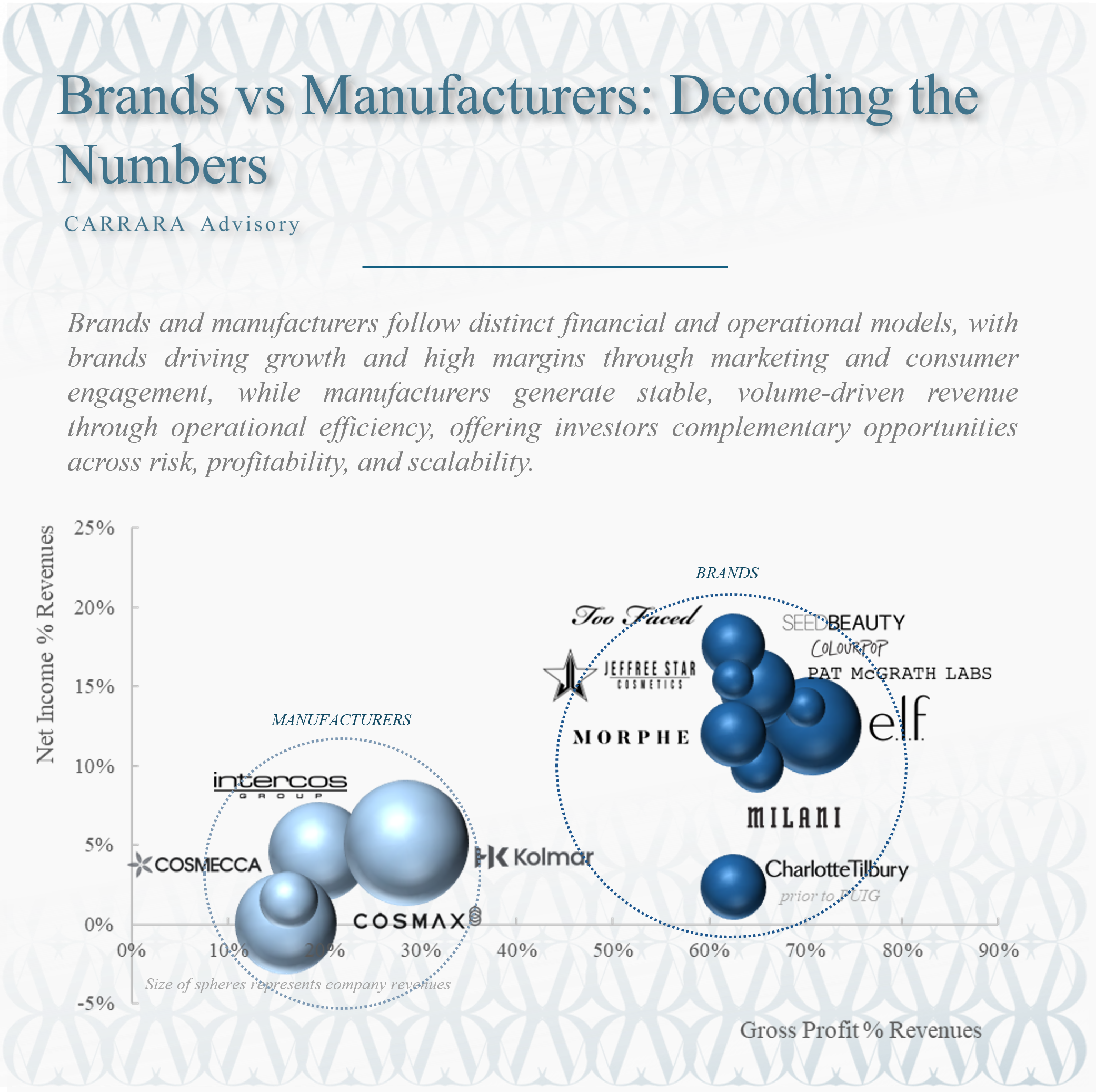

Brands vs Manufacturers: Decoding the Numbers

Brands and manufacturers follow distinct financial and operational models, with brands driving growth and high margins through marketing and consumer engagement, while manufacturers generate stable, volume-driven revenue through operational efficiency, offering investors complementary opportunities across risk, profitability, and scalability.

Crossroads: Kering’s Current Challenges and the Road Ahead

Kering stands at a critical crossroads where restoring Gucci, streamlining operations, clarifying group identity and exploring bold strategic moves such as mergers, Eyewear monetization or deep digital transformation will determine whether it emerges as a more diversified, resilient and operationally disciplined luxury leader or remains overly dependent on a single brand.

Inflation Resilience. Two Decades of Industry Winners and Losers

Over twenty years, industries differ sharply in their ability to outpace inflation, with brand-driven, emotionally valued, and innovation-led sectors like beauty, jewelry, apparel, and IT showing consistent real growth, while cyclical, regulated, or discretionary categories such as automotive, alcohol, and parts of pharma often underperform.

From H1 Struggles to Q3 Growth: Key Trends Shaping the Beauty Industry

A clear recovery, with growth driven by agile, innovation-focused brands, strategic turnarounds, and strong execution across channels and regions, while legacy mass-market segments continue to face pressure.