Brands vs Manufacturers: Decoding the Numbers

The beauty industry is vibrant, competitive, and ever-evolving. Behind every product lies a complex network of businesses: consumer-facing brands that build identities and foster loyalty, and manufacturers that produce the products without ever putting their name on the packaging. Sometimes they are the same but often they are different entities. For investors and industry professionals, understanding the differences between these business models is essential, because each presents unique financial dynamics, opportunities, and risks.

In this article, we focus on the makeup category, comparing brands and manufacturers from a financial perspective. We explore profitability, growth potential, working capital dynamics, and strategic opportunities, drawing on real-world examples to illustrate why some investors prefer one type over the other.

Understanding the Two Business Models

Makeup brands are the companies that consumers know and engage with directly. They develop product lines, create marketing campaigns, and sell through retail and/or e-commerce channels. Brands have the advantage of pricing power, their products can command higher margins because consumers are paying for perceived value, innovation, and brand identity. High gross margins, often in the range of 60 to 70 percent, give these companies flexibility to invest in advertising, influencer partnerships, research, and global expansion.

However, this model also comes with significant responsibilities. Brands must constantly innovate to stay relevant, manage inventory to avoid unsold products, and maintain strong marketing campaigns to retain consumer attention. Operational costs are high, and missteps can quickly impact profitability. Still, for brands that scale effectively, the combination of high margins and growing sales can generate impressive returns.

Manufacturers, on the other hand, operate mostly in the background. These contract or private-label manufacturers produce makeup for brands, handling formulation, production, packaging, and regulatory compliance. Their revenue comes from volume and long-term client relationships, rather than brand recognition or consumer loyalty. Margins are lower, typically 15 to 30 percent for gross profit, because manufacturers compete on efficiency, pricing, and capacity. But the upside lies in stability: manufacturers often serve dozens or hundreds of clients, reducing reliance on any single partner, and can generate significant absolute profits if they scale operations successfully.

Profitability: Brands vs. Manufacturers

Financially, the contrast between brands and manufacturers is stark. Brands often enjoy high gross margins and healthy net income percentages. For example, leading makeup brands may see gross margins of 65–70 percent, with net income margins ranging from 10 to 18 percent. This high-margin profile allows brands to absorb operational expenses while still generating strong profits. Marketing, R&D, and distribution costs are significant, but once a brand reaches scale, these expenses can be leveraged, meaning that additional revenue contributes proportionally more to the bottom line.

Manufacturers, in contrast, operate on lower margins. Gross profits of 15–30 percent are common, with net income often in the single digits. This reflects the operational intensity of the business: manufacturing facilities, quality assurance labs, regulatory compliance, and raw material sourcing all require substantial investment. Yet when volume is high, these companies can achieve meaningful absolute profits and generate stable cash flow. In addition, manufacturers that provide research and development services alongside production can earn higher-margin revenue streams, further diversifying their income.

Case Studies: Real-World Examples

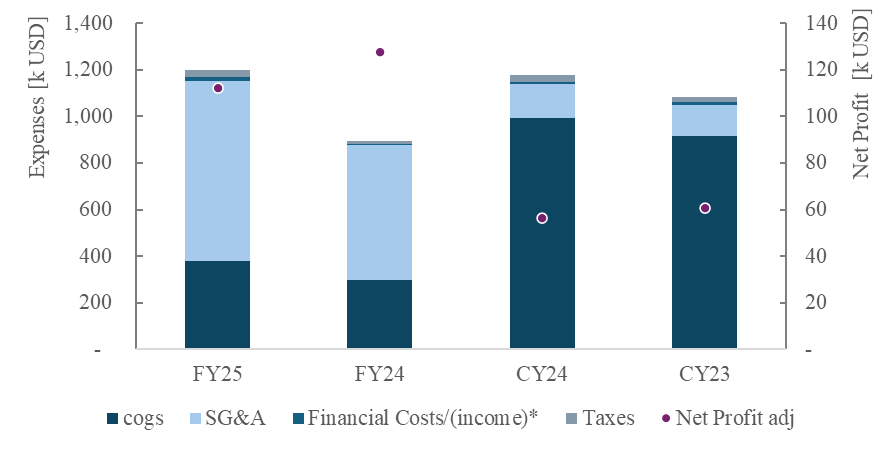

To illustrate the financial and operational differences between makeup brands and manufacturers, consider E.L.F. Beauty, a leading consumer-facing brand(s), and Intercos, a prominent contract manufacturer serving hundreds of brands globally. Interestingly, both companies generate comparable top-line revenue, around 1.2 to 1.3 billion USD, yet the way they deploy these resources is fundamentally different.

E.L.F. Beauty consistently achieves high gross margins of approximately 70 percent. Its revenue growth is strong, fueled by strategic marketing campaigns, influencer collaborations, and innovative product launches across both direct-to-consumer channels and traditional retail. The brand invests heavily in its operations, with roughly 60 percent of revenues allocated to SG&A, a figure dominated by marketing spend and personnel costs, while about 30 percent goes into the cost of goods sold. This investment strategy reflects the brand’s focus on consumer engagement, building loyalty, and differentiating its product portfolio. Efficient working capital management is another hallmark of the brand: inventory turnover has improved over time, and receivable collection has become faster, contributing to overall liquidity and financial flexibility. Conservative leverage allows E.L.F. to reinvest in growth opportunities, whether expanding its geographic footprint, acquiring complementary brands, or funding research and development for new product lines.

In contrast, Intercos operates with a very different financial and operational structure. Its gross margins are considerably lower, around 19 percent, and net income represents only a modest portion of revenues. Yet its revenue scale is substantial, reflecting the sheer volume of production it handles for multiple brand clients worldwide. The company invests heavily in cost of goods sold, approximately 80 percent of revenue, while SG&A represents just 12 percent, including about 4 percent for research and development. This allocation illustrates a clear operational focus: Intercos prioritizes production efficiency, technical expertise, and the ability to meet high-quality standards across large volumes.

Beyond profitability and cost structure, the management of working capital and leverage highlights another fundamental difference between makeup brands and manufacturers. Using E.L.F. Beauty and Intercos as examples, we can see how these financial mechanics reflect the operational realities of each business model.

E.L.F. Beauty demonstrates efficient working capital management despite its consumer-facing orientation and heavy investment in marketing and personnel. Trade receivables are moderate, reflecting strong control over customer payments and largely predictable cash inflows from retail and e-commerce channels. Inventory levels are carefully managed, balancing product availability against the risk of overstocking in a category where trends can shift rapidly. The result is a relatively high Days Inventory Outstanding (DIO) compared with manufacturers, which may seem counterintuitive given the lower proportion of revenue spent on cost of goods sold. In practice, this reflects the brand’s need to maintain a broad product assortment and anticipate consumer demand, which often requires holding more inventory relative to COGS. Trade payables are also smaller, reflecting limited reliance on extended payment terms from suppliers, likely because the brand prioritizes rapid market execution and agility over stretching supplier financing. Overall, E.L.F.’s trade working capital represents a moderate portion of revenue, and its conservative financial leverage enhances flexibility, enabling reinvestment into marketing campaigns, product innovation, or acquisitions.

By contrast, Intercos operates with fundamentally different working capital dynamics, shaped by its role as a contract manufacturer. Both receivables and payables are substantially larger than those of the brand, reflecting the volume and complexity of B2B operations. Receivables are larger because some clients operate on net terms, paying invoices after delivery or batch production, sometimes across multiple countries and currencies. Payables are also larger because the company leverages supplier terms to finance raw material purchases and production costs. Despite a much higher proportion of revenue being allocated to COGS Intercos maintains a smaller DIO than the brand. This reflects faster inventory turnover and highly efficient production scheduling, which minimizes the time raw materials and work-in-progress remain on hand. Inventory is deployed primarily to meet client demand rather than to support marketing or trend-driven product experimentation, allowing the company to convert raw materials into cash more rapidly.

These contrasts illustrate the operational and financial levers unique to each model. For brands like E.L.F., working capital is a tool to balance consumer demand, product variety, and marketing-driven growth. For manufacturers like Intercos, working capital management is central to sustaining high-volume operations, financing production efficiently, and maintaining liquidity across a complex supply chain. Both approaches can be highly effective within their respective contexts, but they reflect fundamentally different business imperatives: the brand prioritizes agility, marketing, and consumer engagement, while the manufacturer emphasizes operational efficiency, scale, and predictable cash flow.

Leverage further differentiates the two models. E.L.F. Beauty maintains conservative debt levels relative to EBITDA, reinforcing financial flexibility and reducing risk. This allows the brand to fund aggressive marketing campaigns, expand distribution, and pursue strategic acquisitions without compromising liquidity. Intercos, while also maintaining reasonable leverage, operates in a capital-intensive environment where production facilities, equipment, and R&D investments are substantial. The company must balance borrowing with operational cash flow to finance these fixed assets while sustaining service levels for multiple clients. This operational leverage amplifies the importance of consistent revenue streams and efficient cost control, as even small inefficiencies can impact margins more significantly than in a brand-driven model.

In summary, the financial structures and operational choices of makeup brands and manufacturers reflect their distinct business strategies. Brands like E.L.F. Beauty allocate significant resources to marketing, consumer engagement, and growth initiatives, managing working capital to balance inventory and receivable timing with market responsiveness. This approach enables higher margins and strong growth potential, albeit with greater exposure to market trends and operational execution risks. Manufacturers like Intercos, in contrast, focus on operational efficiency, large-scale production, and leveraging client relationships and supplier terms to generate stable cash flow. Their lower margins are offset by consistent revenue and resilience built through scale and diversified clients. Understanding these differences is essential for investors, as each model presents unique opportunities, risks, and financial imperatives: brands offer growth and profitability upside, while manufacturers provide stability and operational leverage, together representing the full spectrum of strategic investment options within the makeup sector.

Strategic Implications for Investors

Investors must carefully weigh the trade-offs between makeup brands and manufacturers, as each presents distinct financial dynamics and strategic opportunities. Brands, such as E.L.F. Beauty, offer the potential for high-margin growth, strong consumer loyalty, and scalability, but they also carry higher exposure to market trends, marketing costs, and inventory risks. Manufacturers, like Intercos, provide stable, diversified revenue streams, operational leverage, and resilience through scale, though they operate on lower margins and face competitive pressures that can limit upside.

For equity investors, a balanced approach may be particularly effective. Exposure to both brands and manufacturers captures the high-growth, high-margin potential of brands while benefiting from the predictable, volume-driven stability of manufacturers. Private equity and strategic investors may find opportunity in manufacturers with strong R&D capabilities, a global footprint, and long-term client relationships, while brand founders should focus on selecting manufacturing partners who are not only operationally reliable but also innovative collaborators. For manufacturers, continued investment in technology, operational efficiency, and sustainability is essential to differentiate in a competitive landscape and support evolving brand needs.

Key Takeaways

The industry presents two complementary but distinct pathways for value creation. Brands leverage marketing, innovation, and consumer engagement to achieve high margins and scale, converting investment in growth initiatives into profitability. Manufacturers focus on operational efficiency, volume, and diversified client relationships to generate stable revenue and consistent cash flow, even with lower margins.

A deep understanding of financial mechanics, cost allocation, and working capital management is critical for investors. Brands allocate more to SG&A and marketing, maintaining flexibility to drive growth, while manufacturers invest heavily in production and optimize inventory, receivables, and payables to sustain operations at scale. Both models come with unique risks and opportunities, and each offers a different risk-reward profile depending on investor objectives.

WORKSHOP: Introduction to the Beauty Industry for Financial Institutions

CHF 10,000.00