Proya Group: The Blueprint of China’s Rising Beauty Empires

Introduction

A silent revolution is reshaping the global beauty landscape, and it’s coming from China. In just over a decade, a new breed of domestic champions has emerged, transforming China from the world’s largest consumer of Western beauty brands into one of the most dynamic creators of its own. Among them stand Proya, Chando, Winona, and Marubi, each defining a new standard of innovation, digital agility, and consumer intimacy.

At the forefront of this movement is Proya Group Co., Ltd., whose evolution offers perhaps the clearest blueprint for how China’s homegrown beauty houses are rewriting the industry playbook. Proya’s ascent, from a local skincare label in Hangzhou to a publicly listed, digitally dominant, multi-brand powerhouse, encapsulates the strategic sequencing, data fluency, and operational discipline now distinguishing China’s most successful beauty enterprises.

Unlike the first generation of Chinese brands, which relied heavily on retail distributors and price competition, this new cohort built itself on digital ecosystems, brand science, and real-time consumer insight. Proya, in particular, has demonstrated how a brand can scale rapidly while preserving profitability and brand equity, a balance that many Western peers continue to chase.

Today, as Proya explores acquisitions in Europe and other mature markets, it stands not just as a national success story, but as a template for China’s rising beauty empires: companies equally capable of influencing global markets as they once were of following them.

Proya’s trajectory has not been the result of a single disruptive moment, but of a carefully sequenced transformation, executed in distinct phases that progressively reshaped its brand portfolio, commercial model, and global outlook.

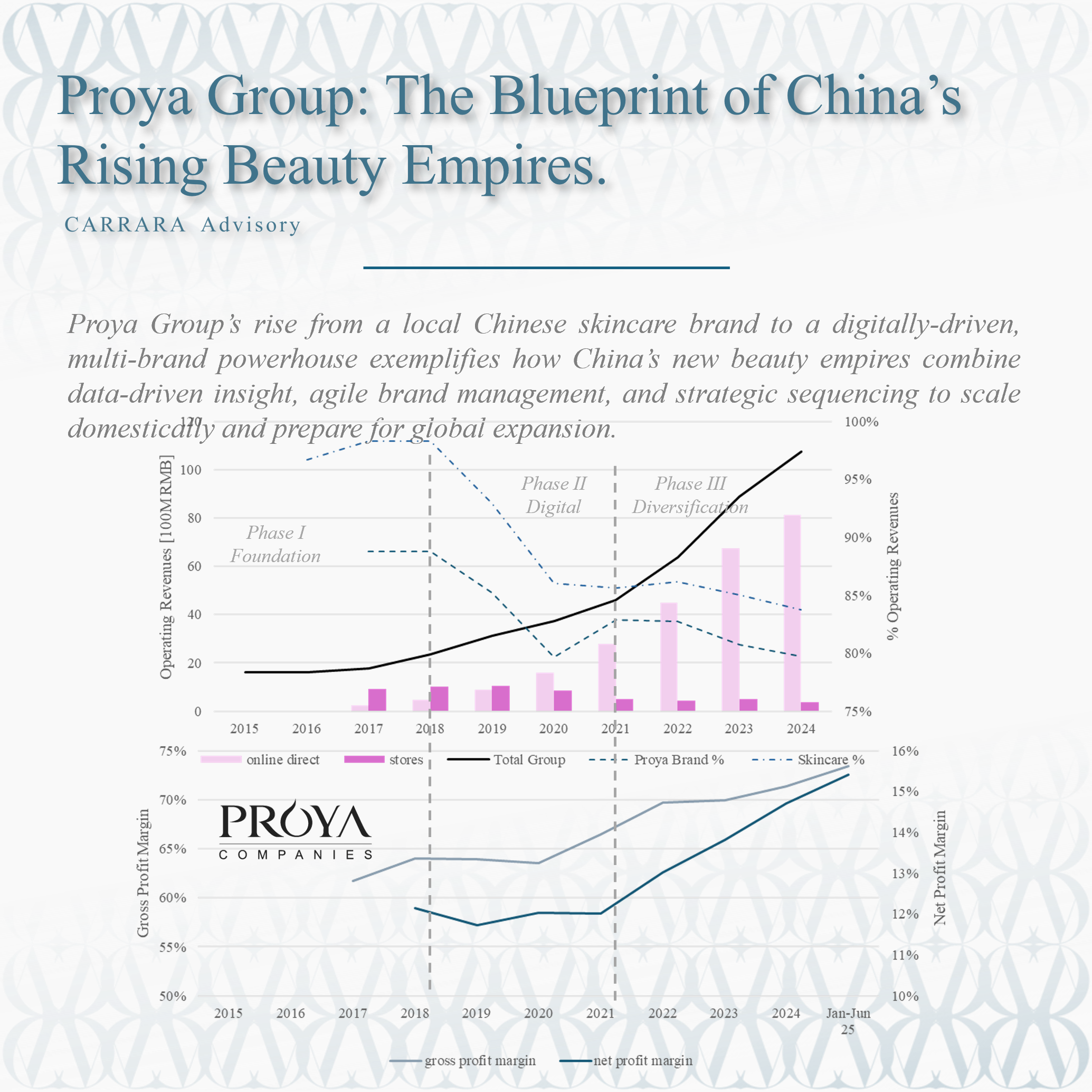

Phase I (2015–2018): Building the Foundations in an Offline World

In its early years as a listed company, Proya operated much like a traditional beauty business. The focus was on distribution breadth, brand awareness, and stable offline growth.

Between 2015 and 2018, revenues rose from RMB 1.63 billion to RMB 2.36 billion, a modest but steady expansion that relied heavily on department stores, cosmetics counters, and specialty retailers. At that stage, nearly 60% of all sales came from offline points of sale, while the flagship Proya brand represented almost 90% of the total business.

This period was crucial for laying down the company’s organizational and reputational foundation: Proya invested heavily in R&D capabilities, built a robust logistics and production infrastructure, and expanded its reach across China’s second- and third-tier cities. The company’s product mix was almost entirely skincare, accounting for over 98% of total revenue, but its approach to the category was consistent and data-informed, even at a time when few Chinese players had access to advanced consumer insight tools.

Financially, the company achieved a gross margin increase from 61.7% in 2017 to 64.0% in 2018, an early sign of improving pricing discipline and a gradual shift toward premiumization. However, net margins hovered around 12%, suggesting a company still maturing, balancing expansion costs with operational discipline.

Phase II (2019–2021): The Digital Acceleration

Proya’s true transformation began when it embraced China’s digital economy. The years from 2019 to 2021 marked an inflection point, the moment when Proya stopped being a traditional beauty player and became a data-driven, e-commerce-native organization.

Revenues soared from RMB 3.12 billion in 2019 to RMB 4.62 billion in 2021, a 48% increase over two years. The change was not only quantitative but structural: online sales exploded from 53% of total revenues in 2019 to 85% by 2021. The company quickly adapted to the new retail paradigm, leveraging platforms such as Tmall, Douyin, JD, and Kwai, and building an exceptionally agile content-marketing operation.

Proya’s dual online model, a distinction still evident in its official communication, became one of its greatest strengths. The company operates through:

Direct sales, conducted on Tmall, Douyin, JD, Kwai, and Pinduoduo, where Proya controls the full consumer experience, pricing, and content and gathers proprietary data;

Distribution sales, carried out via resellers on platforms such as Taobao, JD, and Vipshop, where Proya benefits from scale and reach without direct inventory or operational risk.

This system allowed Proya to maintain control over its brand identity and pricing, while still capitalizing on the extended ecosystem of resellers. It balanced control and expansion, enabling the company to capture data, optimize margins, and test new product concepts with remarkable agility.

While most peers struggled to adapt to the pace of China’s e-commerce revolution, Proya built internal competence in digital operations, live-streaming sales, and KOL collaborations, converting social traffic into sustained brand equity.

The offline business, meanwhile, was intentionally reduced but not abandoned. It evolved into a network of strategic dealer-operated stores in department stores and modern malls, not as a volume channel, but as a brand-building tool reinforcing credibility and physical visibility.

The company also began its brand diversification journey. Timage, a color-cosmetics label, for modern, image-conscious consumers, began scaling rapidly and positioned Proya in the rapidly growing makeup segment, while Hapsode targeted younger consumers seeking gentler, dermatologist-tested skincare. Both launches signaled a strategic shift from a single-brand dependency to a portfolio model.

These moves signaled Proya’s understanding that consumer segmentation (not just digital fluency) was key to sustaining relevance in China’s fragmented beauty landscape.

Despite this rapid transformation, profitability remained healthy. Gross margins stabilized around 64–66%, while net profit margins held near 12%, demonstrating that the company’s pivot to digital did not come at the expense of efficiency.

Phase III (2022–2024): Scale, Diversification, and Global Readiness

If the previous phase was about transformation, the years since 2022 have been about consolidation and elevation. In three years, Proya’s revenues more than doubled, climbing from RMB 4.62 billion in 2021 to RMB 10.77 billion in 2024.

The online channel, now accounting for over 95% of total sales, became both the backbone of growth and the laboratory for innovation. Proya’s precision in digital execution allowed it to outperform not only Chinese peers but even many international players struggling to localize their online operations in China.

At the same time, the company refined its brand architecture, developing a portfolio that now includes:

Proya, the flagship science-based skincare brand;

Timage, a fast-growing makeup line;

Hapsode, for sensitive and younger skin;

Off&Relax, a body and lifestyle brand;

INSBAHA, with a focus on clean, minimalist beauty.

This structure mirrors that of leading global beauty groups, where the master brand anchors credibility and the satellite brands target specific consumer segments and price points.

The category mix also evolved: skincare still drives around 84% of revenues, but makeup has grown to 13%, compared to less than 1% in 2018. This diversification supports not only consumer acquisition but also margin improvement, given the typically higher profitability of color products when distributed directly online.

Indeed, margins tell the story of maturity: by mid-2025, Proya’s gross margin had risen to 73.4%, up nearly ten points in five years, and its net profit margin to 15.4%, reflecting superior cost management, pricing power, and operational scale.

The evolution of Proya’s sales model clarifies the engine behind these results:

“The Company primarily focuses on online channels, while also maintaining offline channels. Online sales are mainly operated through direct sales and distribution. Direct sales are mainly carried out through platforms such as Tmall, Douyin, JD, Kwai, and Pinduoduo, and distribution is based on platforms such as Taobao, JD, and Vipshop. Offline sales are mainly operated through dealers. The sales channels include specialty cosmetics stores, department stores, and multi-brand retail outlets in modern shopping malls.”

This statement encapsulates the hybrid logic of Proya’s model: near-total digital dominance tempered by a strategic offline presence. Physical stores now serve primarily as brand-building touchpoints. reinforcing trust, testing experience formats, and supporting omni-channel integration, rather than as volume drivers. The online business, with its dual track of direct and distributed sales, offers both control and flexibility, ensuring that scale does not erode margin or brand equity.

Phase IV: Toward International Expansion and Brand Acquisitions

Having mastered the domestic battlefield, Proya is now looking outward and particularly toward Europe. The logic is clear. As the Chinese market grows increasingly competitive, owning or partnering with established European brands offers both global prestige and product differentiation.

From a strategic perspective, European acquisitions would provide:

Access to heritage and craftsmanship, assets that continue to hold strong emotional appeal among Chinese consumers.

Advanced formulation and regulatory expertise, especially in dermocosmetics and clean beauty, areas aligned with Proya’s science-driven positioning.

Mutual distribution leverage, as European brands gain entry into China through Proya’s digital infrastructure, while Proya gains global credibility.

This outward orientation aligns with Proya’s long-term goal of becoming a globally competitive beauty group, not merely a domestic leader. Its financial stability, margin profile, and multi-brand experience make it a credible acquirer.

From a symbolic standpoint, the move marks a reversal of roles: a Chinese beauty group not just importing Western know-how, but exporting capital, operational excellence, and digital innovation back into Europe. It reflects the maturing confidence of China’s consumer sector and the emergence of domestic champions operating at international standards.

Conclusion: The Architecture of a Modern Beauty Empire

Proya’s journey from a mid-tier offline player to a data-powered, innovation-driven beauty conglomerate is emblematic of China’s new corporate sophistication. Proya’s trajectory offers a blueprint for understanding how China’s beauty empires are redefining scale and speed in the industry:

Data before instinct: Every move — from brand positioning to product drop timing — is driven by social media analytics and consumer feedback loops.

Omnichannel integration as default: Unlike Western brands that had to “digitally transform,” Proya was born digital and is now integrating offline, not the reverse.

Brand agility within corporate structure: Despite its size, Proya operates with the speed and creative elasticity of an indie label — a critical advantage in the trend-driven beauty sector.

The company’s model stands as a benchmark for the new generation of global beauty players. Its success carries lessons well beyond China: that agility and control are not mutually exclusive, that digital intimacy can coexist with premium positioning, and that growth anchored in strategic sequencing produces durable value.

As Proya turns its gaze toward Europe, it does so not as an emerging challenger, but as a mature contender, one whose command of digital consumer engagement may prove as valuable to Western brands as European craftsmanship is to Proya’s own future. In that balance lies the blueprint of the next era of global beauty: where East and West no longer compete but converge.

#BeautyIndustry #ChinaBeauty #DigitalTransformation #BrandStrategy #GlobalExpansion #Proya #Innovation #ConsumerInsights #LuxuryBeauty #Omnichannel