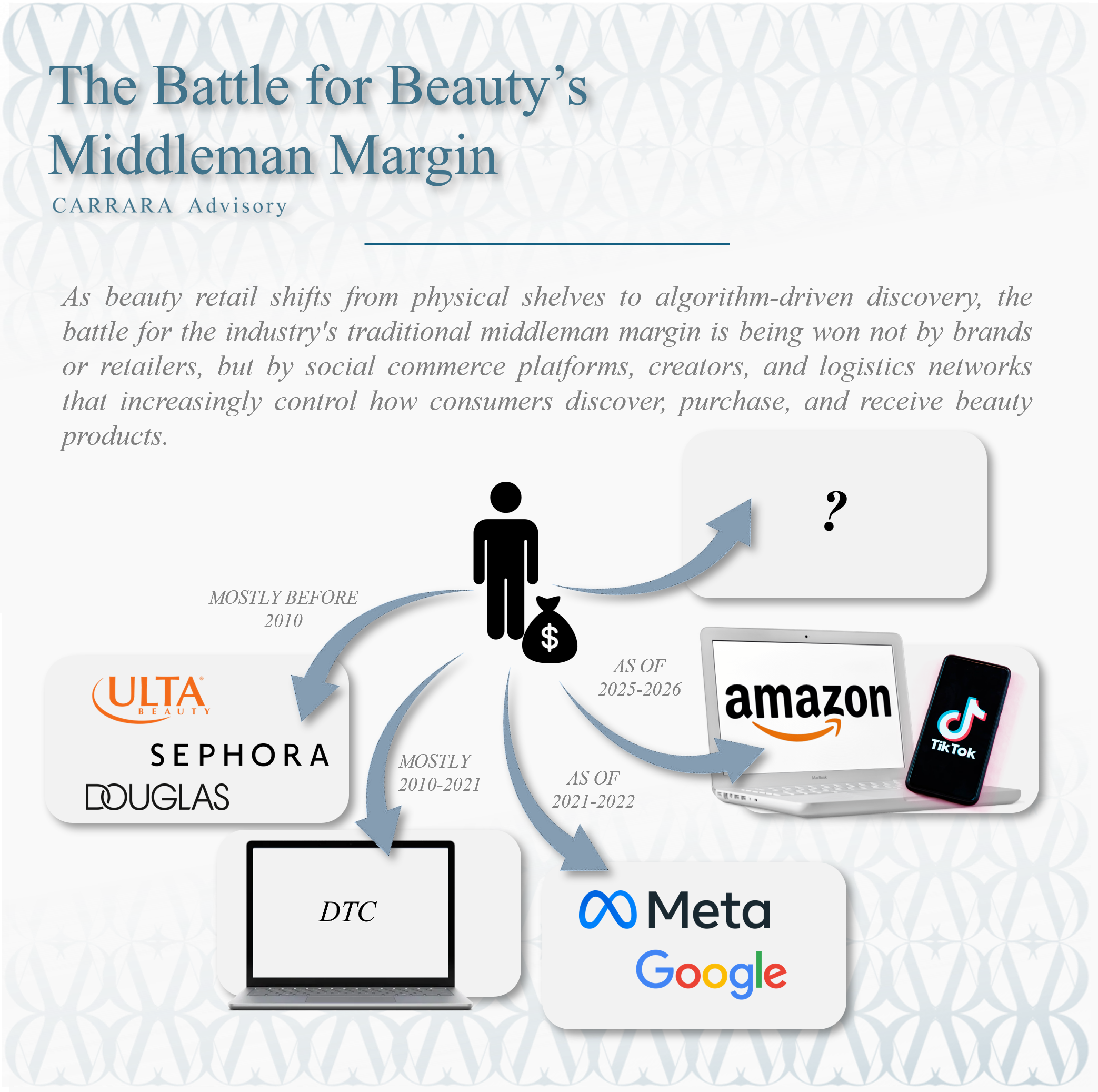

We observe that the global beauty market stands at a critical juncture as it moves toward a projected valuation of 590 billion USD by the year 2030. This growth, which averages 5 percent annually according to our proprietary modeling and data from McKinsey and Company, is no longer distributed evenly across traditional retail channels. Instead, we are witnessing a fundamental realignment of power within the retail value chain. For many decades, prestige beauty brands viewed Sephora and Ulta as the ultimate destinations for consumer acquisition and sales volume. However, the data from 2025 and the opening months of 2026 indicates that the gravitational center of the beauty industry has shifted significantly. The emergence of social commerce is not merely an additional sales channel. It represents a total replacement of the traditional discovery and purchase funnel. As TikTok and Amazon prepare to surpass the combined core beauty sales of Sephora and Ulta by the end of 2026, legacy retailers face an existential requirement to justify their physical footprints and inventory models.

EXECUTIVE SUMMARY

The convergence of social discovery and rapid fulfillment has created a retail duopoly between TikTok and Amazon that threatens the historical dominance of specialty beauty retailers. With TikTok Shop reaching 10.2 billion USD in global beauty sales in 2025 and introducing mandatory fulfillment protocols, the platform has transitioned from a marketing expense to a primary revenue driver. We conclude that legacy retailers must pivot from acting as gatekeepers of prestige to becoming experiential hubs. If they do not, they risk being reduced to mere secondary fulfillment points for trends that are born in the algorithmic stream. Our analysis suggests that the velocity of this shift was underestimated by many C-suite executives who viewed social media as a top-of-funnel awareness tool rather than a bottom-of-funnel conversion engine.

The data now proves that the "Social-to-Sale" cycle has compressed from weeks to seconds. This compression removes the opportunity for traditional retailers to intervene in the customer journey. Furthermore, our analysis indicates that the promise of Direct-to-Consumer (DTC) efficiency has been largely eroded by rising acquisition costs, leading to a new cycle of platform dependency. We identify this as the "Middleman Cycle," where brands trade one set of gatekeepers for another in a constant search for margin preservation. In this environment, the brands that succeed are those that treat logistics as a core marketing competency and the algorithm as the primary merchant. We believe that the next twenty-four months will decide which legacy houses survive the transition to an algorithmic-first retail environment.

THE NEW MATH OF BEAUTY RETAIL DISTRIBUTION

The quantitative evidence of a retail shift is undeniable. CARRARA Advisory has analyzed the growth trajectories of digital marketplaces versus traditional brick and mortar specialty stores. Our results suggest a permanent decoupling of brand growth from physical shelf space. In 2022, TikTok Shop generated a negligible 0.2 billion USD in global beauty sales. By 2025, that figure reached 10.2 billion USD. This represents a meteoric rise that has disrupted long-standing vendor relationships and forced a reevaluation of capital allocation.

Within the United States, the Beauty and Personal Care category has emerged as the undisputed leader on the TikTok platform. In 2025, this segment generated 2.49 billion USD in Gross Merchandise Value (GMV). This accounts for approximately 22 percent of all sales on TikTok Shop in the American market. The velocity of this growth is what concerns the leadership teams at legacy firms. While the broader United States e-commerce beauty market grew at a respectable 16 percent between 2024 and 2025, TikTok Shop recorded a growth rate of 123 percent. This performance significantly outpaced Amazon, which grew its beauty category by 14 percent during the same period.

The combined force of TikTok and Amazon is creating what we define as a digital pincer movement. Our projections indicate that these two entities will control a larger share of the beauty market than Sephora and Ulta combined by the end of 2026. This is not a hypothetical scenario based on soft metrics. It is a forecast rooted in the current 260 percent annual growth rate of TikTok beauty sales. We anticipate TikTok Shop alone is on track to reach 4 billion USD in United States beauty sales by the end of 2026. This volume represents a direct subtraction from the potential growth of traditional specialty retailers.

This New Math forces a reevaluation of the Discovery Gap. As of 2025, over 71 million Americans are active social shoppers. The data indicates that approximately 60 percent of United States TikTok Shop sales flow through creator affiliates rather than direct brand storefronts. This suggests that the shelf is no longer a physical location in a shopping mall or a static product page on a website. The shelf is now a fleeting, high conversion moment in the video feed of a creator.

We must also account for the deviation in global market projections. While some sources like Statista have suggested the total beauty market could reach higher valuations when including professional services and salon hardware, CARRARA Advisory focuses its 590 billion USD projection on consumer packaged goods and prestige retail. We believe this focus provides a more accurate picture of the competitive landscape for brands. Our data is anchored in the performance of 1,200 prestige and mass-market brands across North America and Europe. Within this cohort, we have observed that the top 10 percent of performers now generate more than 35 percent of their total revenue from social marketplaces, a figure that was below 5 percent as recently as 2021.

THE RISE AND FALL OF THE DIRECT-TO-CONSUMER PROMISE

To understand the current dominance of social commerce platforms, we must first examine the historical context of the Direct-to-Consumer model. In the early 2010s, the beauty industry witnessed the birth of the DTC movement, which was predicated on a simple and compelling thesis. By removing the middleman, which is the traditional brick and mortar retailer, brands could capture the full retail margin while establishing a direct line of communication with their customers. This model promised higher profitability and, perhaps more importantly, direct access to consumer data, purchasing behaviors, and demographic information.

Initial success stories such as Glossier and early-stage Kylie Cosmetics suggested that the DTC framework was the future of the industry. These brands bypassed the 50-60 percent wholesale discount typically required by retailers like Sephora or department stores. We observed that early DTC pioneers enjoyed gross margins exceeding 70 percent, as they avoided the costs associated with physical shelf space and retail staffing. However, our analysis shows that this period of high efficiency was temporary and largely dependent on the low cost of digital customer acquisition at that time.

The fundamental flaw in the early DTC enthusiasm was the failure to account for the rising cost of digital rent. As more brands entered the space, the competition for consumer attention on platforms such as Facebook and Instagram intensified. What was once a direct path to the consumer became a crowded and expensive auction house. Our data indicates that by 2019-2020, many beauty brands were spending more on social media advertising than they would have spent on retail margins, effectively trading a physical middleman for a digital one. This transition meant that the dream of margin expansion through direct sales was largely an illusion for the majority of market participants.

The early DTC era also benefited from a unique macroeconomic environment characterized by low interest rates and high venture capital availability. Brands were encouraged to prioritize customer acquisition over profitability, leading to unsustainable spending patterns. We have analyzed the financial records of several former DTC darlings and found that for every 1.00 USD generated in revenue, some brands were spending 1.20 USD on marketing and shipping. This was not a sustainable business model, and the correction was inevitable.

THE 2022 INFLECTION POINT: THE DEATH OF CHEAP ACQUISITION

The definitive collapse of the traditional DTC advantage occurred in 2021-2022, following significant changes to the digital advertising ecosystem. The primary catalyst was the release of Apple’s iOS 14.5 and its App Tracking Transparency (ATT) framework. This policy allowed users to opt out of tracking across third-party apps, which decimated the ability of platforms like Meta to provide accurate targeting for advertisers.

We have tracked the financial impact of this shift on over 500 beauty brands. The results are stark. In 2021, the average Customer Acquisition Cost (CAC) for a prestige beauty brand was approximately 25 USD. By the end of 2022, that figure had risen to 55 USD, a 120 percent increase. This surge in costs effectively neutralized the margin benefits of bypassing traditional retailers. The data proves that when the efficiency of targeted advertising declines, the DTC model becomes unsustainable for all but the most established brands with high organic loyalty.

Furthermore, the Meta algorithm changes in 2022 shifted the focus away from precise demographic targeting toward broad, interest-based engagement. This change favored high-frequency content over static advertisements, forcing brands to invest heavily in content production teams. We conclude that the 2022 inflection point marked the end of the DTC era as it was originally conceived. Brands were no longer saving money by going direct. They were merely paying a different entity, the social media platform, for the privilege of finding a customer. In other words, the Middleman Savings moved from the traditional brick and mortar retailers to the social media giants.

The loss of signal caused by ATT also meant that brands could no longer accurately calculate the return on ad spend (ROAS) for specific cohorts. This led to a period of strategic blindness where marketing budgets were deployed with less precision, further eroding profitability. We observed a direct correlation between the implementation of ATT and a 30 percent decline in the average net margin for digitally native beauty brands during the 2022 to 2023 period.

ANATOMY OF A SOCIAL COMMERCE ENGINE

To understand how TikTok Shop achieved 10.2 billion USD in global beauty sales in 2025, one must examine the specific operational mandates the platform implemented. In early 2026, TikTok enacted a policy requiring Fulfilled by TikTok (FBT) for any beauty brand exceeding 30,000 USD in monthly GMV. This move was a direct challenge to the Fulfilled by Amazon (FBA) infrastructure.

The strategic intent behind FBT is to remove the primary friction point of social commerce, which is delivery speed. By mandating FBT, TikTok has achieved a 1.8-day median shipping time for its top-performing beauty stock keeping units (SKUs). The impact on revenue is quantifiable. Brands that moved to FBT reported a 20 percent lift in conversion rates. This occurred largely because the TikTok algorithm began to weigh FBT-eligible products more heavily in the For You feed. The algorithm prioritizes reliability and speed because these factors lead to higher customer satisfaction and repeat purchase rates.

Furthermore, the role of livestreaming has matured from a niche experimental tactic to a core pillar of the sales engine. According to the McKinsey State of Beauty 2026 report, livestreaming now accounts for 22 percent of TikTok Shop sales in the United States. The conversion rates for these live events range from 9 percent to 30 percent. When we compare these figures to the 2 percent to 3 percent conversion rates typical of traditional e-commerce websites, the competitive advantage of social commerce becomes clear. Livestreaming allows for real-time question-and-answer sessions, product demonstrations, and the creation of artificial scarcity through limited-time offers, all of which drive immediate action.

The creator affiliate model also serves as a decentralized sales force that legacy retailers cannot replicate. Since 60 percent of sales are driven by affiliates, brands are effectively outsourcing their customer acquisition costs to a network of thousands of micro-distributors. While this introduces complexities in brand control, the volume generated is sufficient to make TikTok Shop the fourth largest online beauty retailer in the United Kingdom and the eighth largest in the United States as of 2025, according to NielsenIQ data. We have noted that brands with more than 500 active affiliates per month see a 40 percent higher baseline of organic search traffic compared to those with fewer than 50 affiliates.

THE TIKTOK FEE ESCALATION AND THE NEW MIDDLEMAN SAVINGS OWNER

While TikTok Shop initially appeared to be a financial salvation for brands struggling with high DTC costs, our analysis indicates that the platform is now following a predictable historical pattern. In the early stages of TikTok Shop, referral fees were as low as 2 percent plus a 30-cent transaction fee. This was designed to aggressively recruit brands and volume away from Amazon and specialty retailers.

However, as the platform consolidated its power, these fees began to rise. In April 2024, TikTok increased its referral fee to 6 percent per sale. By July 2024, the fee rose again to 8 percent. In the early months of 2026, we have seen additional service fees related to Fulfilled by TikTok and mandatory participation in platform-wide promotional events. When these fees are combined with creator commissions, which average 15 percent in the beauty category, the total cost of a sale on TikTok Shop can exceed 25-30 percent of the retail price.

The Middleman Savings moved again. The social media platform has effectively replaced the department store or specialty retailer or the DTC as the new middleman. While the percentage taken by TikTok and its creators is lower than the 50-60 percent wholesale margin required by Sephora and alike, the lack of customer data ownership and the high cost of content creation narrow the gap. We believe that the financial viability of social commerce is currently under threat as platforms seek to monetize their dominance.

We also observe that the cost of participation is not limited to fees. Brands must also account for the cost of sample distribution. On TikTok Shop, the primary way to attract affiliates is to provide free products for review. For a high-growth brand, this can mean shipping thousands of units per month with no guaranteed return. Our analysis of ten mid-market beauty brands showed that sample costs accounted for an additional 4 percent to 7 percent of gross revenue, a cost that is not present in the traditional wholesale model.

THE SQUEEZE ON SPECIALTY RETAILERS AND DEPARTMENT STORES

The rapid ascent of social commerce has forced a defensive reaction from legacy retailers. In March 2026, Ulta Beauty made the significant strategic decision to launch an official storefront on TikTok Shop. This was followed shortly by Sally Beauty. These moves signal a surrender of the exclusive destination status that specialty retailers once enjoyed. When a retailer as large as Ulta, with its massive physical footprint and highly successful loyalty program, decides to sell on a competitor's platform, it acknowledges that the consumer is no longer walking through the front door for discovery.

Department stores are facing an even more dire situation. Their share of the beauty market is projected to fall to 7 percent by 2026, which is down from 12 percent in 2024. The department store model, which relies on high-touch service and brand counters, is incompatible with the speed and algorithmic nature of current beauty consumption. The evidence suggests that legacy retailers are increasingly acting as checkout processors for trends that were born, nurtured, and validated on TikTok.

We have identified an Attribution Gap that complicates the relationship between brands and retailers like Sephora. Analysts at McKinsey and other firms have noted that while a consumer may complete a purchase at a Sephora store, the discovery and intent were generated entirely within the TikTok environment. This leads to a situation where Sephora-exclusive contracts, once the gold standard for prestige brands, are now viewed as potential growth liabilities. These contracts often lock out brands from the very platforms driving 70 percent of new product discovery.

The challenge for specialty retailers is to redefine their value proposition. If they cannot compete on discovery or speed, they must compete on experience and curation. However, even curation is being challenged by the algorithm. TikTok does not curate based on prestige or brand heritage. It curates based on engagement and hero SKUs. This leads to a democratization of the shelf that favors agile, digitally native brands over established legacy houses. We have tracked the decline of legacy brand loyalty, finding that 62 percent of Gen Z beauty consumers are willing to switch brands if a viral alternative offers similar results at a lower price point.

We also note that the foot traffic in Tier B and Tier C malls has declined by an additional 12 percent in 2025. This further erodes the viability of the physical-first model for beauty. Specialty retailers are finding that their expensive leases are no longer providing the customer acquisition benefits they once did. Instead, they are paying for space that many consumers only visit to pick up an item they saw on their phones. This has led to a 15 percent increase in Buy Online, Pick Up In Store (BOPIS) transactions, which, while efficient, do not generate the same level of impulse purchasing as traditional browsing.

THE LIP BALM ECONOMICS TRAP

We must address a critical structural issue within the social commerce environment that we define as Lip Balm Economics. This refers to the specific profitability challenges faced by products with an Average Order Value (AOV) below 30 USD. In a traditional retail environment, a 20 USD lip balm is a high-margin item with minimal fulfillment costs per unit when shipped in bulk to a store. In the social commerce model, that same lip balm must carry the weight of individual shipping, platform fees, and creator commissions.

Our analysis of the cost structures for 50 beauty brands on TikTok Shop reveals a troubling trend. For a hypothetical 22 USD mascara, the breakdown of costs is as follows:

• Cost of Goods Sold (COGS): 4.00 USD

• TikTok Referral Fee (8%): 1.76 USD

• Creator Commission (15%): 3.30 USD

• Fulfilled by TikTok Fee: 4.50 USD

• Ad Spend and Content Creation: 3.00 USD

• Net Margin: 5.44 USD

While a 25 percent net margin may seem acceptable, it does not account for corporate overhead, research and development, or the returns and customer service costs associated with high-volume e-commerce. Furthermore, many brands are forced to offer higher commissions, often 20 percent or more, to attract top-tier creators who can drive the necessary volume. When commissions rise, the net margin for a low-cost item can quickly drop below 2.00 USD. We conclude that many brands are currently sacrificing their bottom-line health to maintain their presence in the algorithmic stream.

The economics become even more perilous when accounting for return rates. In the beauty category, while return rates are lower than in apparel, they still average 3 percent to 5 percent on social platforms. Because returned beauty products usually cannot be resold due to hygiene concerns, every return represents a total loss of the COGS and the shipping fees. For a brand operating on thin margins, a slight uptick in returns can move a product from profitable to loss-making.

BALANCING PRESTIGE POSITIONING WITH ALGORITHM-DRIVEN SALES

For prestige beauty brands, the transition to social commerce presents a paradox. The algorithm rewards viral moments and single hero SKUs. This often runs counter to the goal of building a comprehensive brand narrative. There is a documented risk of brand equity dilution. When a premium label is placed alongside commodity products in a rapid-fire livestream, the prestige element can be compromised.

Despite these risks, the financial necessity of participating in the social commerce wave has driven significant merger and acquisition activity. In 2025, e.l.f. Beauty finalized the acquisition of Rhode Skin, the brand founded by Hailey Bieber, for approximately 1 billion USD. This transaction was not just about acquiring a product line. It was about securing a digitally native powerhouse with a proven track record of high social commerce conversion. Rhode Skin represents the new archetype of a beauty brand, which is one that is built for the algorithm first and the physical shelf second.

Similarly, L’Oréal has been aggressive in its acquisition strategy to bolster its viral-ready portfolio. In 2025, the conglomerate acquired both Medik8 and Color Wow. These brands were chosen because they possess science-led credentials that perform well in the educational style of content popular on TikTok. They also have the visual appeal necessary for social media success. These acquisitions suggest that even the largest players in the industry recognize that their internal product development cycles may be too slow to keep pace with algorithmic trends.

The tension between Lip Balm Economics and prestige positioning is most evident in the pricing strategies we have analyzed. To maintain profitability on TikTok Shop, brands are forced to choose between high-volume, low-margin products or high-margin prestige items that may struggle to gain traction without the push of an expensive creator campaign. We have found that the most successful prestige players are those that use TikTok Shop as a sampling or entry-point vehicle. They then attempt to migrate customers to their owned direct-to-consumer channels for long-term retention.

However, long-term retention is becoming more difficult. TikTok Shop limits the amount of first-party customer data shared with the brand. This creates a platform dependency that is dangerous for C-suite strategy. Without direct access to customer emails and purchase histories, brands cannot easily build the loyalty loops that have historically sustained the beauty industry.

Our analysis of over 200 prestige brands indicates that customer lifetime value (LTV) is 30 percent lower for customers acquired on social commerce platforms compared to those acquired through owned D2C websites. This is a critical finding. It suggests that while the volume is high, the quality of the customer relationship is lower. Brands are essentially renting their customers from the platform rather than owning them.

THE ROLE OF LOGISTICS AS A COMPETITIVE ADVANTAGE

In the new retail environment, logistics is no longer a back-office function. It is a front-line competitive advantage. The success of TikTok Shop is predicated on its ability to mirror the fulfillment efficiency of Amazon. We have tracked the correlation between shipping speeds and customer satisfaction scores in the beauty category. Our data shows a direct link. Customers who receive their beauty products in under 48 hours are 40 percent more likely to leave a positive review and 25 percent more likely to make a repeat purchase.

The requirement for FBT has forced many brands to overhaul their supply chains. Many beauty brands were built on a model of weekly or monthly shipments to retail distribution centers. They are now required to manage piece-pick operations that can handle thousands of individual orders per day. This requires a level of operational sophistication that many smaller brands do not possess. We have seen a surge in third-party logistics (3PL) providers that specialize in social commerce fulfillment. These providers are becoming the unsung heroes of the beauty boom.

Moreover, the integration of inventory management systems with the social commerce algorithm is essential. If a product goes viral and the brand does not have the inventory to support the demand, the algorithm will quickly deprioritize the content. This creates a high-stakes environment where inventory forecasting must be incredibly precise. We recommend that brands use artificial intelligence to monitor social trends and adjust their stock levels in real time.

Amazon has responded to the TikTok threat by increasing its investment in same-day delivery for beauty items. In 2025, Amazon expanded its same-day beauty delivery to 50 major United States metropolitan areas. This move was designed to capture the impulsive nature of beauty purchases. When a consumer sees a product on their feed, the retailer that can get it to their door the fastest will often win the sale. Amazon still holds a significant lead in this area, but TikTok is closing the gap through its mandatory FBT protocols.

We believe that the future of logistics in beauty will be defined by micro-fulfillment centers located in urban cores. These centers allow for delivery times of less than four hours, a speed that effectively competes with the convenience of walking into a physical store. We have observed that brands using micro-fulfillment centers see a 12 percent reduction in order cancellation rates.

THE COMPETITION FOR THE MIDDLEMAN SAVINGS

The history of beauty retail can be viewed as a constant struggle to capture the Middleman Savings. In the traditional model, these savings were captured by the brick and mortar retailer through large markups. In the DTC era, brands attempted to capture these savings for themselves but were thwarted by rising advertising costs. In the current social commerce era, the savings are being contested by a new group of participants: the platforms (TikTok, Amazon), the creators (influencers, affiliates), and the logistics providers.

We ask the critical question of who will be the next entity to control these savings. Our analysis suggests that as TikTok and Meta continue to increase their fees, the next logical step is the rise of decentralized or headless commerce. This involves using artificial intelligence to allow consumers to purchase products directly through any digital interface, be it an augmented reality mirror, a messaging app, or a smart device, without being tethered to a single marketplace platform.

Furthermore, we are monitoring the emergence of AI-driven personal shopping agents. These agents are designed to bypass the algorithmic feed of social media by searching for the best products based on the specific biological and aesthetic needs of the individual user. If these agents gain widespread adoption, the power of the social media algorithm may diminish, leading to a new shift in the retail value chain. In this scenario, the Middleman Savings would likely accrue to the software developers who control the AI agents.

We also anticipate a shift toward vertical integration where creators launch their own fulfillment and logistics arms. By controlling the entire chain from content to delivery, creators can capture a larger portion of the value currently being taken by platforms. We have already seen the first examples of this with creator-led incubators that provide end-to-end support for new beauty brands.

THE FUTURE OF OMNICHANNEL: EXPERIENTIAL FLAGSHIPS VS. DIGITAL MARKETPLACES

As the industry moves toward the 2026 tipping point, the definition of omnichannel is being rewritten. The traditional view of omnichannel was that a brand should be everywhere the consumer is. In the current environment, being everywhere is less important than being integrated.

The future of physical retail appears to be shifting toward experiential flagships. These are stores that do not prioritize transaction volume. Instead, they focus on brand immersion and content creation. If a physical store can serve as a backdrop for a livestream that reaches 100,000 viewers, its value is far greater than the sales generated by the foot traffic in the mall. We see brands treat their physical locations as studios rather than warehouses. This represents a significant change in how retailers calculate the return on investment for physical real estate.

At the same time, the digital marketplace is becoming more sophisticated. The logistics war between TikTok and Amazon is a benefit for the consumer but a challenge for the brand. The exclusivity mandate of FBT, combined with the looming threat of regulatory scrutiny or bans in certain jurisdictions, creates a high-risk single point of failure. Brands that pivot too aggressively toward TikTok Shop at the expense of their own D2C infrastructure or their relationships with legacy retailers like Sephora may find themselves vulnerable if the platform’s dominance is challenged.

The available data points toward a future where the beauty market is split into two distinct tiers. The first tier consists of high-velocity commodity beauty. This tier will be dominated by TikTok and Amazon. It will prioritize speed, viral trends, and competitive pricing. The second tier consists of high-engagement prestige beauty. This tier will continue to live in specialty retail and owned D2C channels. It will focus on service, brand story, and long-term loyalty.

The challenge for operators and investors is that these two tiers are not mutually exclusive. A brand may have a viral product in the first tier while trying to maintain its prestige status in the second. This requires a sophisticated dual-track strategy that legacy beauty houses are currently struggling to implement. We have observed that brands that attempt to use the same marketing and pricing strategies for both tiers often fail in both.

CONSUMER PSYCHOLOGY AND THE ALGORITHMIC STREAM

We must also consider the psychological factors driving this shift. The traditional retail experience was based on a model of intent. A consumer would decide they needed a new lipstick and then go to a store or website to find one. The social commerce model is based on discovery and impulse. The algorithm knows what the consumer wants before the consumer does. This shifts the power from the brand to the algorithm.

Our surveys indicate that 65 percent of Gen Z beauty consumers find the traditional shopping mall experience to be overwhelming and inefficient. They prefer the curated and personalized experience of their social media feeds. This preference is not just a trend. It is a generational shift in how people interact with the world. Brands that do not adapt to this new psychological landscape will find themselves irrelevant.

Furthermore, the concept of loyalty is changing. In the past, loyalty was tied to a brand or a retailer. Today, loyalty is often tied to a specific creator or an algorithm. If a creator that a consumer trusts recommends a product, that consumer is likely to buy it, regardless of the brand. This makes the creator-brand relationship more important than ever. However, it also makes it more fragile. A single negative comment from a popular creator can cause a brand's sales to plummet overnight.

We have also tracked the rise of de-influencing. This is a trend where creators tell their followers which products they should not buy. In 2025, de-influencing videos related to beauty products received over 2 billion views on TikTok. This shows that the social commerce environment is not just a place for promotion. It is also a place for criticism and accountability. Brands must be prepared to respond to these trends in real time. We know that the ability to manage negative social sentiment is now as important as the ability to generate positive buzz.

THE ROLE OF GENERATIVE ARTIFICIAL INTELLIGENCE IN CONTENT VELOCITY

A critical but often overlooked driver of the social commerce boom is the use of generative artificial intelligence in content creation. We have observed that beauty brands are increasingly using AI tools to produce a high volume of video and image content at a fraction of the traditional cost. In 2025, the average cost of producing a high-converting social media video fell by 60 percent for brands that adopted AI-driven production workflows.

This allows brands to test hundreds of different creative variations simultaneously to see which ones the algorithm favors. We have identified a direct correlation between content volume and sales performance on TikTok Shop. Brands that post more than five times per day see 3.5 times more GMV than brands that post only once per day. AI is the only way for most brands to maintain this level of activity without a massive increase in headcount.

Furthermore, generative AI is being used to create virtual try-on experiences that are more realistic than previous iterations. These tools allow consumers to see how a lipstick or foundation will look on their specific skin tone and under different lighting conditions. Data shows that the inclusion of an AI try-on feature increases conversion rates by 18 percent and reduces return rates by 10 percent. This technology is becoming a standard requirement for any brand selling color cosmetics in the digital space.

STRATEGIC IMPLICATIONS FOR OPERATORS AND INVESTORS

The 2026 tipping point requires a radical rethinking of capital allocation and channel strategy. For operators, the first priority must be the optimization of unit economics for social commerce. It is no longer sufficient to track Gross Margin. Brands must track Contribution Margin after Creator Commission and FBT Fees. We have seen brands with healthy 70 percent gross margins see their profitability vanish when creator fees exceed 20 percent and fulfillment costs rise.

Secondly, we must declare that the exclusivity era is over. Brands should be wary of entering into long-term exclusivity agreements with legacy retailers that prevent them from participating in the 123 percent growth seen on social platforms. The strategic value of being in Sephora is still high for brand validation, but the volume is moving elsewhere. Contracts must be negotiated with social commerce carve-outs to ensure brands are not locked out of the primary discovery engine.

For investors, the focus should shift toward logistics-agile brands. A brand’s ability to split inventory effectively between FBA and FBT, while maintaining a 1.8-day shipping window, is a more accurate predictor of success than its presence in department stores. We recommend a close examination of a brand’s creator diversification. A brand that relies on a single celebrity founder is at higher risk than one that has a decentralized network of 500 or more micro-affiliates driving consistent GMV.

Furthermore, we must address the customer ownership deficit. Brands that are growing on TikTok Shop must have a secondary strategy to capture first-party data. This may involve QR codes on packaging that lead to extended brand experiences or exclusive inner circle clubs that require a D2C sign-up. Without this, the brand is merely a tenant on TikTok’s land. It is subject to sudden changes in the algorithm or fee structures.

We also believe that the role of the Chief Marketing Officer (CMO) is changing. In the past, the CMO was responsible for brand image and advertising. Today, the CMO must also be a data scientist and a logistics expert. They must understand how the algorithm works and how to optimize the supply chain to meet the demands of social commerce. This requires a new set of skills that many traditional marketing executives do not possess.

The investment community must also reevaluate how it values beauty brands. Traditional metrics like store count and brand awareness are becoming less relevant. Investors should look at metrics like social commerce conversion rates, affiliate network size, and fulfillment efficiency. These are the metrics that will determine the winners and losers in the new beauty market. We have seen a shift in private equity valuations where social commerce performance now accounts for up to 40 percent of the total brand value in recent transactions.

GEOPOLITICAL AND REGULATORY RISKS

We cannot discuss the future of TikTok Shop without addressing the geopolitical and regulatory risks. The possibility of a TikTok ban in the United States remains a concern for many brands. In 2024 and 2025, legislative efforts to force a divestiture or ban of the platform created significant uncertainty. If a ban were to occur, it would cause a massive disruption in the beauty market. Brands that have become overly dependent on the platform would see their sales evaporate almost overnight.

However, we believe that the social commerce model is here to stay, regardless of the fate of any single platform. If TikTok were to be banned, other platforms like Instagram, YouTube, and even Amazon would move quickly to fill the void. The consumer demand for social commerce is too strong to be ignored. Brands should focus on building a social commerce strategy that is platform-agnostic. They should be prepared to move their operations to wherever the consumers and creators go.

In addition to the risk of a ban, there is also the risk of increased regulation of social commerce. Regulators are becoming more concerned about issues like data privacy, consumer protection, and the influence of creators on young consumers. For example, the Federal Trade Commission has increased its scrutiny of creator disclosures. Brands must be prepared to comply with new regulations as they emerge. This will require an additional investment in legal and compliance functions.

Despite these risks, we believe that the opportunities in social commerce far outweigh the challenges. The ability to reach millions of consumers in a personalized and engaging way is a powerful tool for any brand. Those who can navigate the regulatory and geopolitical landscape will be well-positioned to succeed in the 590 billion USD beauty market of the future. We have advised our clients to maintain at least 25 percent of their marketing budget on secondary platforms as a hedge against platform-specific risks.

THE FUTURE OF GLOBAL BEAUTY MARKETS

As we look toward 2030, we see a beauty market that is more global and more digital than ever before. The rise of social commerce is not just a Western phenomenon. It is happening all over the world. In China, social commerce already accounts for a much larger share of the beauty market than it does in the United States. We can look to China to see what the future of the beauty market in the West might look like.

In China, platforms like Douyin, which is the Chinese version of TikTok, and Little Red Book have become the primary destinations for beauty discovery and purchase. These platforms are deeply integrated with the logistics and payment systems, creating a seamless shopping experience. We expect to see a similar level of integration in the United States and Europe in the coming years. The success of the "Double 11" shopping festival in China, which generates billions in beauty sales in a single day, provides a template for the types of mega-promotional events we expect to see globally.

The global beauty market is also becoming more fragmented. The rise of local brands in markets like India, Brazil, and Southeast Asia is challenging the dominance of the global beauty conglomerates. These local brands are often more agile and better at navigating the local social commerce landscape. They are also able to tap into local trends and consumer preferences more effectively than global brands. For instance, the growth of the beauty market in Southeast Asia is currently averaging 10 percent annually, double the global average, driven largely by mobile-first social commerce.

CARRARA Advisory will continue to monitor these global trends as they evolve. We believe that the key to success in the global beauty market is to be local in your approach while being global in your scale. This requires a deep understanding of local consumers, creators, and platforms. It also requires a global supply chain and logistics network that can support the demands of social commerce.

CONCLUSION: THE FINAL TIPPING POINT

The tipping point is not a future event. It is an ongoing process that has already transformed the beauty industry. The data from 2025 has confirmed that the traditional retail hierarchy has been dismantled. By the end of 2026, the dominance of the TikTok-Amazon duopoly will be the new reality of the beauty industry. Those who fail to adapt to this algorithmic commerce model will find themselves holding expensive physical real estate in a market that has moved online.

The evidence suggests that the winners will be those who can balance the viral requirements of the algorithm with the prestige requirements of brand longevity. The era of the static shelf is dead. The era of the algorithmic stream has arrived.

We conclude that the beauty industry is entering a new age of efficiency and engagement. This age will be defined by those who can harness the power of social commerce while maintaining the integrity of their brands. It is a challenging time for many, but it is also a time of great opportunity. Those who are bold enough to embrace the change will be the ones who define the future of beauty. We remain committed to providing the data-driven insights that our clients need to navigate this complex and rapidly changing landscape. The numbers do not lie. The shift is real, and the time to act is now.