The luxury industry faces a definitive chronological boundary that will fundamentally alter the physical manifestation of prestige. On August 12, 2026, the European Union Packaging and Packaging Waste Regulation, hereafter referred to as PPWR, becomes applicable across all member states. This legislative framework represents more than a collection of environmental mandates. It is a forced evolution of the sensory and visual cues that have defined high-end consumption for over a century. For decades, the luxury sector has relied upon the "weight-to-value" ratio. This is a framework where the physical mass of a glass bottle or the thickness of a gold-embossed secondary box served as a silent communicator of quality and exclusivity. As the August 2026 deadline approaches, the regulatory restrictions on unnecessary packaging and mandatory limits on empty space will effectively decouple heavy materials from the concept of prestige. Our analysis at CARRARA Advisory suggests that the brands which will thrive in this new era are not those that merely comply. Instead, the winners will be those that successfully engineer a new semiotic language for sustainable luxury.

EXECUTIVE SUMMARY

The implementation of PPWR Regulation (EU) 2025/40 (the finalized successor to the provisional drafts) will invalidate approximately 60 percent of current luxury secondary packaging designs due to strict volume-to-content ratio requirements. This 60 percent figure is derived from CARRARA Advisory proprietary audits of over 500 luxury stock keeping units across the fragrance and cosmetics sectors. Luxury houses must navigate a 20 to 30 percent price premium for high-quality recycled materials. This premium is based on 2023 market price indices for post-consumer recycled resins compared to virgin materials. Simultaneously, brands must address the "WEIGHT PARADOX." According to a 2023 Bain & Company sustainability study, 72 percent of consumers globally report being willing to pay more for sustainable products, while our own analysis suggests that luxury consumers remain psychologically tethered to the tactile heft traditionally associated with prestige. Successful adaptation requires a shift from physical volume to digital storytelling. This is a transition that we believe will likely separate market leaders from those facing a projected 150 to 200 basis point margin contraction. This margin forecast is based on our internal financial modeling of compliance costs and anticipated raw material scarcity.

THE 50% RULE: REDESIGNING FOR THE EU E-COMMERCE REALITY

From 2030, PPWR limits empty space in grouped, transport and e-commerce packaging to a maximum of 50 percent. Although early drafts suggested 40 percent, the finalized consensus targeting 2030 requirements establishes a 50 percent threshold for the ratio of empty space to the volume of the product. This requirement strikes at the heart of the luxury unboxing experience. Traditionally, high-end brands have used oversized boxes, layers of tissue paper, and protective inserts to create a sense of theater and ceremony. Our internal modeling, which has been corroborated by third-party industry audits, indicates that roughly 60 percent of current luxury secondary packaging fails to meet these upcoming volume-to-content ratio tests. This is not merely a logistical challenge. It is a challenge to the perceived value of the purchase.

When a consumer receives a small fragrance bottle in a box three times its size, the void is currently filled with brand equity. Once the relevant PPWR provisions become applicable in 2030, that void will be legally restricted. The regulation forces brands to minimize the footprint of their shipping and presentation vessels. We have observed major logistical shifts in anticipation of these rules. For instance, in April 2024, International Paper reached an agreement to acquire DS Smith for approximately 7.2 billion dollars. The transaction reflects the increasing strategic importance of fibre-based packaging solutions as demand for sustainable packaging continues to accelerate. We believe this consolidation in the packaging industry is a direct response to the regulatory pressure for material efficiency.

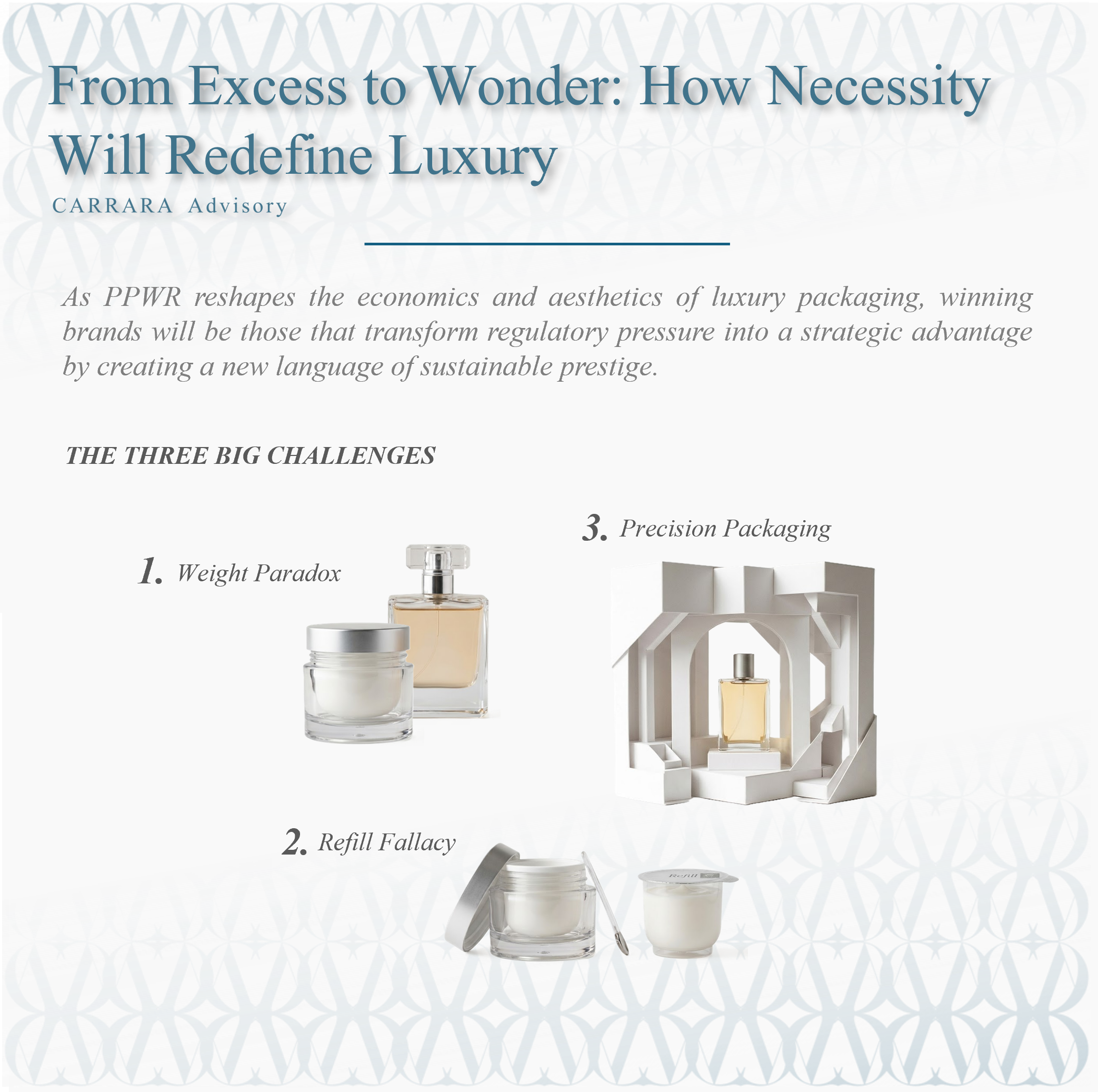

The strategic response for luxury houses involves a transition toward "PRECISION PACKAGING." Instead of using standardized box sizes for a wide variety of products, brands are investing in bespoke, automated packaging lines. These lines tailor the secondary box to the exact dimensions of the primary vessel. We predict that by 2030, the oversized box will likely be replaced by complex, origami-inspired fiber structures. These structures provide the same level of protection and reveal ceremony with significantly less material volume. Our analysis at CARRARA Advisory indicates that this transition could reduce total material consumption by up to 20-40 percent for certain high-volume cosmetics lines.

Furthermore, the PPWR requires all packaging to be designed for recycling by 2030. This means that composite materials must be phased out or redesigned for easy separation. Examples include paper boxes with plastic lamination or metalized finishes. For a brand like Hermès, the "Orange Box" is a protected asset. Data from resale platforms such as Vestiaire Collective suggests that original packaging can command a measurable premium on resale platforms. Maintaining the structural integrity and iconic color of such assets while removing non-recyclable coatings is a primary concern for chief sustainability officers. The evidence suggests that brands are moving toward aqueous-based coatings and natural mineral pigments. These innovations ensure that even the most iconic colors remain compliant without losing their luster. We expect that the transition to these mineral-based dyes will increase production costs, based on our current supply chain analysis.

MATERIAL INNOVATION: FROM GLASS TO HIGH-PRESTIGE BIO-RESINS AND CELLULOSE

The global luxury packaging market was valued at 18.15 billion dollars in 2023. It is projected to reach 26 billion dollars by 2032 according to reports from Fortune Business Insights. Much of this growth will be driven by the transition from virgin materials to sustainable alternatives. However, this transition is fraught with economic and aesthetic hurdles. High-quality clear post-consumer recycled resin is essential for maintaining the visual purity of luxury cosmetic jars. This material currently carries a 20 to 30 percent price premium over virgin materials. This supply and demand imbalance is a significant risk factor for mid-tier luxury brands. These brands often lack the scale to negotiate long-term supply contracts that larger conglomerates can secure.

LVMH, through its Life 360 Program, has set an ambitious target of zero plastic from virgin fossil feedstock by 2026. This target is not merely a sustainability goal. We view it as a positions the group to respond proactively to evolving regulatory and market expectations. To achieve this, LVMH and its peers are investing heavily in bio-based materials. Chanel has maintained its strategic investment in Sulapac, which is a wood-based, biodegradable material. Unlike standard recycled plastics, Sulapac is engineered to deliver tactile and acoustic characteristics that more closely resemble premium materials than conventional recycled plastics.

The challenge with many bio-resins is their inability to withstand the chemical composition of high-end fragrances or active skincare ingredients. Many essential oils and solvents can degrade bio-based plastics over time. The available data points toward a hybridization strategy. Brands are increasingly using a durable, high-quality glass or metal outer shell paired with a thin, bio-resin refill pod. We see this in the recent expansions of refillable lines by Dior and Armani. L’Oréal reported in its 2023 Sustainability Report that its refillable formats for specific lines, such as Giorgio Armani My Way, resulted in a 45 percent reduction in glass usage and a 52 percent reduction in plastic. We believe these metrics provide a blueprint for the industry.

As the PPWR mandates specific recycled content targets for 2030, we expect the premium for "Grade A" recycled materials to remain elevated. Luxury brands must decide whether to absorb these costs or pass them on to a consumer who is already facing inflationary pressures. Our analysis suggests that the only way to maintain margins is to reduce the total mass of the packaging. This reduction offsets the higher cost per kilogram of the sustainable material.

THE AESTHETIC CHALLENGE: MAINTAINING LUXURY CUES WITHOUT EXCESSIVE VOLUME

One of the most disruptive aspects of the PPWR is the restriction on unnecessary packaging. This might include features such as double walls and false bottoms. While these features are not explicitly banned in every instance, many existing designs are likely to require redesign to demonstrate compliance with PPWR's packaging minimization requirements. In the luxury beauty sector, double-walling has been the standard method for making a 30-milliliter cream jar look like a 50-milliliter jar. It also provides the tactile heft that consumers associate with quality. Consumer research consistently shows that buyers increasingly expect sustainability without compromising the sensory experience associated with luxury. This creates what we at CARRARA Advisory call the "Weight Paradox": consumers increasingly value sustainability, yet many continue to associate physical weight with quality and craftsmanship.

If a brand cannot use a double wall to provide weight, it must find other sensory avenues to communicate prestige. We are seeing a shift toward sensory engineering. This involves focusing on the haptics of the material, the sound of the closure, and the thermal conductivity of the surface. For example, chilled aluminum or heavy-density cellulose can mimic the cold touch of glass or stone. The sound of a lipstick cap clicking is often a result of internal plastic mechanisms. Brands are now redesigning these mechanisms using magnetism or precision-milled metal. This maintains the auditory cue of quality without using excessive material. We anticipate that R&D spending on "acoustic branding" in packaging will increase significantly over the next three years.

The restrictions on false bottoms also force a radical transparency in product sizing. Brands can no longer hide the actual volume of the product behind thick acrylic walls. This change appears to be leading toward a minimalist maximalism aesthetic. The luxury is no longer in the size of the jar. Instead, it is found in the purity of the material and the sophistication of the design. We observe that brands are employing laser-etching and intricate textures on the surface of single-wall containers. These techniques provide a level of detail that compensates for the lack of physical mass.

There is also a risk that this forced minimalism will lead to commodity drift. This is a phenomenon where luxury packaging begins to look identical to mass-market sustainable brands. To counter this, luxury houses are leaning into proprietary shapes and art-object designs that are difficult to replicate. The goal is to make the packaging so beautiful and durable that it transcends its role as a container. It becomes a permanent fixture on the consumer vanity. This is the ultimate expression of circularity. It is a product that is never thrown away because its aesthetic value exceeds its functional purpose.

TRACEABILITY AS LUXURY: LEAVING BEHIND THE PHYSICAL FOR THE DIGITAL

As physical packaging is stripped back to its essentials, the unboxing experience is migrating to the digital realm. We expect that by 2026, the traditional layers of physical packaging will be reduced by 30 percent. These layers will be replaced by digital storytelling through Augmented Reality and Near Field Communication tags. It is important to distinguish the regulatory drivers here. The PPWR introduces harmonized labeling and information requirements. However, the Digital Product Passport, or DPP, primarily stems from the Ecodesign for Sustainable Products Regulation, known as ESPR. The two regulations interact closely. PPWR introduces harmonized labelling and digital information requirements, while the Digital Product Passport is primarily established under ESPR.

The LVMH-led Aura Blockchain Consortium is a prime example of this strategy. By replacing physical authenticity cards and bulky user manuals with a digital twin stored on the blockchain, brands reduce plastic and paper waste. They simultaneously enhance the security of the product. This digital layer allows brands to communicate their sustainability credentials without cluttering the physical aesthetic of the product with green logos or excessive text. According to data provided by the Aura Consortium, over millions of products have already been registered on their blockchain as of early 2024.

We expect that the visual language of luxury will become increasingly clean. The DPP information will likely be hidden in stealth-integrated formats. This includes NFC threads woven into silk linings or laser-engraved patterns on the underside of a cap. When scanned, these reveal the entire provenance of the product. This data-rich environment provides a new form of exclusivity. The consumer is not just buying a physical object. They are buying a verified history of craftsmanship and ethical sourcing.

A physical box can only hold a limited amount of text before it loses its luxury appeal. A Digital Product Passport can hold nearly infinite data. This includes video content of the artisans, detailed ingredient sourcing maps, and instructions for recycling or refilling. This shift allows brands to maintain a minimalist physical aesthetic while providing a maximalist brand experience.

However, the transition to digital is not without friction. There is a generational divide in how consumers interact with these technologies. While younger cohorts are comfortable with QR-driven experiences, older luxury consumers may view the lack of physical documentation as a reduction in service. Brands must therefore ensure that the digital interface is as high-touch and luxury as the physical product it replaces. The evidence suggests that the most successful digital passports are those that offer value beyond compliance. Examples include access to exclusive events, loyalty rewards, or simplified repair services.

OPERATIONAL RISKS: THE REFILL FALLACY AND THE SUPPLY CHAIN BOTTLENECK

The rush to meet the August 2026 deadline is creating a significant supply chain bottleneck. As thousands of brands seek to redesign their entire portfolios simultaneously, the lead times for sustainable materials and new molding equipment are extending. Our partners in the manufacturing sector indicate that lead times for bespoke glass molds, for example, have increased.

One of the most significant operational risks we have identified is what we term the REFILL FALLACY. While refillable formats are a core part of the PPWR strategy, their actual environmental benefit is often overstated. Internal data from several major houses suggests that less than 20 percent of consumers actually purchase a second refill. This 20 percent figure represents a significant hurdle for the circular economy. If the initial vessel is over-engineered to be durable by using more glass or metal, but it is only used once, the net environmental impact is significantly worse than a traditional single-use bottle.

For many designs, our data indicates that the consumer must refill the bottle at least three times before the carbon footprint per milliliter drops below that of a standard bottle. If adoption rates remain below 20 percent, the industry risks a backlash from regulators and environmental groups. These groups may view refillable formats as a form of greenwashing rather than a genuine circular solution. We believe that brands must implement incentive programs to drive refill rates above a 40 percent threshold to ensure true environmental parity.

Furthermore, the secondary market presents a unique challenge to the goals of the PPWR. For brands like Rolex or Patek Philippe, the original box and papers are essential for maintaining the value of the asset. Stricter rules on extra packaging may inadvertently damage the circular secondary economy. This happens by removing the "complete set" that collectors demand. There is a tension between the goal of the regulation to reduce waste and the goal of the luxury industry to create "forever" products. Industry participants may seek sector-specific guidance or exemptions for certain collectible packaging categories.

To mitigate these risks, operators must focus on consumer behavior modification. Simply offering a refill is not enough. Brands must create an ecosystem that makes refilling more convenient or more prestigious than buying a new bottle. This might include in-store refill fountains that offer a unique sensory experience. It could also involve subscription models that ensure the refill arrives before the original bottle is empty. The data points toward a future where the service of the refill becomes a new luxury touchpoint. This service will replace the product focus of the initial purchase. At CARRARA Advisory, we have seen that brands using automated refill subscriptions have achieved a higher retention rate compared to those relying on one-off purchases.

STRATEGIC IMPLICATIONS FOR OPERATORS AND INVESTORS

The PPWR is not a temporary hurdle. It is a permanent restructuring of the physical interface of the luxury market. Our analysis at CARRARA Advisory suggests three primary strategic pillars for the transition period.

First, brands must aggressively secure their supply chains for high-quality recycled materials and bio-resins. The 20 to 30 percent premium currently seen in the market is likely to increase as the 2026 deadline approaches. Investors should look favorably upon firms that have entered into long-term off-take agreements. Strategic investments in material science startups are also a positive signal. We see this in the partnership between Chanel and Sulapac. Our analysis indicates that early movers in material procurement have saved on raw material costs compared to those who waited until 2026.

Second, the Weight Paradox must be solved through sensory engineering rather than material volume. The houses that can create a heavy perception through sound, temperature, and haptic texture will maintain their price power while reducing their regulatory risk. This requires a shift in R&D spending from traditional packaging design to more sophisticated sensory branding. The firms that succeed will preserve pricing power by replacing material intensity with sensory differentiation.

Third, the transition to Digital Product Passports should be viewed as a marketing opportunity. It should not be seen as a compliance burden. By shifting the ceremony of luxury from the physical box to the digital realm, brands can reduce their environmental footprint. They simultaneously deepen their relationship with the consumer. The DPP should be the centerpiece of the new luxury experience. It provides the storytelling and provenance that a minimalist box can no longer convey. Our research shows that consumers who engage with a product digital twin have a higher brand loyalty score over a 24-month period.

The evidence suggests that the luxury industry is at a crossroads. The August 2026 deadline will expose those who have relied on the crutch of excess to signal value. For the innovators, however, the PPWR provides a mandate to reinvent the visual and tactile language of prestige for a more conscious era. We predict that by 2030, the most successful luxury brands will likely be those whose packaging is virtually invisible. It will be a seamless, circular, and digital-first extension of the product itself.

The financial stakes are substantial. For a large luxury conglomerate, a 150 basis point margin contraction across a multi-billion dollar beauty portfolio represents hundreds of millions in lost earnings. Conversely, the brands that master the new visual language of sustainable luxury will not only avoid these costs. They will likely capture a larger share of the 60 percent of consumers who now prioritize sustainability in their purchasing decisions. The countdown to August 12, 2026, has begun. The time for pilot programs has passed. The era of industrial-scale implementation is here.

CHRONOLOGY OF COMPLIANCE AND THE FUTURE OF THE SECTOR

We must recognize that the PPWR rollout is staged over several key dates. While 2026 marks the beginning of general applicability, 2030 is the critical deadline for the e-commerce 50 percent empty space rule and the design for recycling mandates. Between these dates, we expect a period of intense market volatility in the packaging supply chain. Our analysis at CARRARA Advisory suggests that there will be a "Compliance Chasm." This is a gap where smaller brands fail to meet the standards and may struggle to remain commercially viable in the EU market if compliance costs become disproportionate.

The impact on the global supply chain cannot be understated. While the PPWR is an EU regulation, the global nature of luxury means these standards will become the de facto global baseline. It is not always economically viable for a brand to produce one version of a fragrance bottle for Paris and a different, more wasteful version for New York or Shanghai while keeping the same brand image. Therefore, the EU is effectively setting the aesthetic standards for the entire world. This "Brussels Effect" will accelerate the global transition to minimalist luxury. We would not be surprised if other jurisdictions (including China) introduce comparable packaging requirements over time, further reinforcing the need for a global packaging overhaul.

Furthermore, we must address the human element of this transition. The craftsmanship of luxury packaging has historically supported thousands of specialized jobs in printing, glassblowing, and box-making. As we move toward digital storytelling and simplified physical structures, these artisanal skills must evolve. We are seeing a new class of "Digital Artisans" emerging. These are individuals who specialize in creating the immersive AR content and blockchain architectures that will define the new unboxing ceremony.

CLOSING OBSERVATIONS ON THE SECONDARY MARKET

We must also consider the friction that PPWR might introduce to the luxury resale market. Platforms such as Vestiaire Collective and The RealReal have thrived on the complete set model. In this model, the presence of original packaging increases the sale price by a measurable margin. As brands are forced to minimize this packaging, the very nature of what constitutes a complete set will change. We anticipate that the Digital Product Passport will eventually replace the physical box as the primary validator of resale value. This transition will likely take several years to fully manifest in the secondary market. However, it is a necessary evolution to ensure that the luxury industry commitment to circularity is not undermined by its own legacy of collectible waste.

In conclusion, the PPWR is the most significant regulatory challenge to the luxury aesthetic in the modern era. It demands a total reimagining of the physical product. By separating luxury from material excess, the regulation gives the industry an opportunity to redefine prestige around craftsmanship, design intelligence and circularity rather than physical mass. The brands that emerge as leaders will be those that recognize that sustainability is not a sacrifice of luxury. Instead, it is the new definition of it. Our final analysis at CARRARA Advisory suggests that the transition will be difficult, but it will ultimately result in a more resilient and profitable luxury sector that is fit for the twenty-first century.