NORMAL: The Discount Retailer Reaches €2Bn in Half the Time of ACTION

A Pattern Worth Recognizing

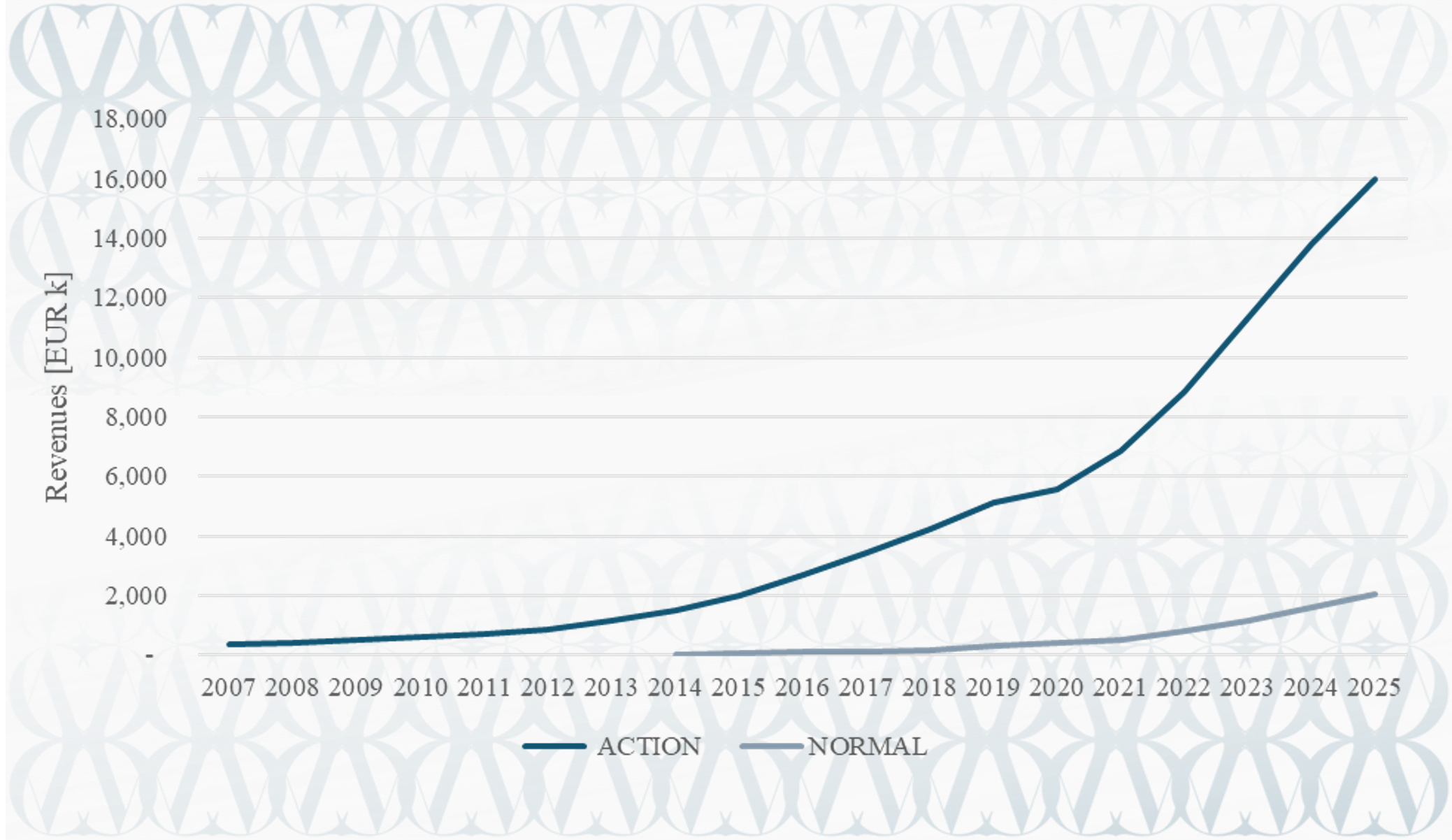

In a previous article on this website, we profiled ACTION, the Dutch discount variety retailer that has grown from a small regional chain into one of Europe's most formidable retail machines. At the time, we argued that ACTION's expansion trajectory, its resilience across economic cycles, and its almost counterintuitive ability to scale quality while holding price, made it one of the most instructive case studies in modern European retail. That argument has only grown stronger since. By 2025, ACTION had reached €16 billion in annual net sales, its EBITDA margins had expanded to approximately 15%, and it continued to add roughly €2 billion in revenue per year, with over 3,000 stores across more than 12 countries.

But the more interesting story right now may not be ACTION itself. It may be what ACTION has spawned: a template that another retailer is now executing at an even more aggressive pace. That retailer is NORMAL.

NORMAL is a Danish discount variety chain founded in 2013 by Torben Mouritsen and Bo Kristensen in Silkeborg, Denmark. Most European retail executives have not yet heard of it. Most will need to. By FY 2024/25, NORMAL had crossed the €2 billion revenue threshold, with approximately €2.0 to 2.2 billion in net sales estimated for the year, and it had done so faster than any comparable European retailer on record, including ACTION itself.

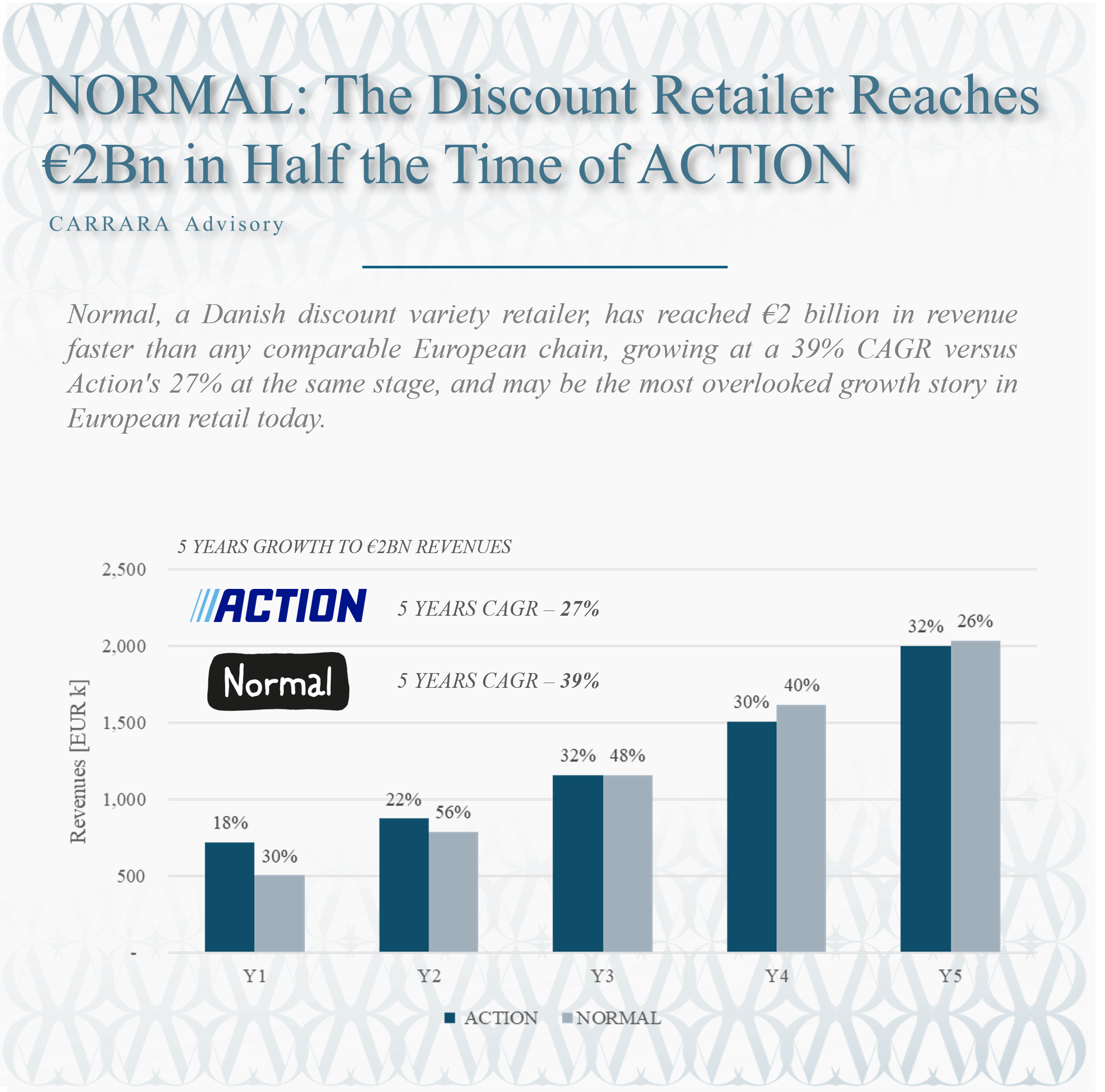

NORMAL just crossed €2 billion in revenue. In the five years leading up to that milestone, it grew at a CAGR of 39%. ACTION, in the equivalent period before reaching the same threshold, grew at 27%.

This article makes the case that NORMAL is not simply a Scandinavian curiosity. It is a scalable retail model at the earliest and most dynamic stage of its European expansion, and that the window to understand it, partner with it, and position around it is, as of this writing, wide open.

The Business Model: Familiar, But Faster

NORMAL's concept is straightforward, which is precisely what makes it so powerful. The company operates discount variety stores selling branded everyday products, with a strong emphasis on personal care, beauty, household cleaning, and food-adjacent categories. The product assortment is broad but curated, with prices positioned meaningfully below those of traditional pharmacy chains and grocery retailers. The stores use a forced-path layout, channeling customers through the entire product range before they reach the checkout, maximizing exposure and driving unplanned purchases. Mouritsen has publicly called Normal 'a hybrid between a grocery store and a personal care store,' a description that captures the model's dual appeal to routine replenishment shoppers and personal care buyers.

The parallels with ACTION are hard to miss. Both chains sell a constantly rotating assortment at low prices. Both create a treasure-hunt dynamic that drives repeat visits and basket size. Both run lean store formats that are cheap to open and quick to reach profitability. Both source opportunistically, combining standard supply relationships with grey-market procurement that allows them to offer branded products at prices that appear almost irrational to competitors operating under conventional margin structures.

Where NORMAL differentiates is in its category focus. While ACTION has a broader general merchandise mix spanning hardware, clothing accessories, toys, and garden products, NORMAL concentrates more heavily on personal care and beauty alongside branded food-adjacent goods. This is a higher-frequency purchase category. Shampoo, deodorant, toothpaste, and skincare products are replenishment items, not impulse buys, and that drives a meaningfully different customer return rate. It is also a category where the perception of value is particularly acute, since consumers are highly familiar with the prices of these products at pharmacies and supermarkets, and the discount at NORMAL is immediately legible.

The gross margin structure reflects this focus. NORMAL's gross margins have been estimated at around 20%, which is lower than many specialty retailers but characteristic of a model that deliberately sacrifices margin for volume and frequency. ACTION, at a comparable stage of development, was operating in a similar margin band. ACTION's operating EBITDA margins ranged between roughly 9% and 14% throughout its growth years, only reaching the 15% range as scale benefits fully materialized. NORMAL's EBITDA margin, currently estimated at 6 to 7%, is therefore not a sign of model weakness. It is a sign of a model at an earlier point on a well-understood curve.

The Numbers: A Growth Curve Unlike Any Other

The most compelling evidence for NORMAL's potential is also the simplest: the revenue trajectory.

NORMAL was founded in 2013 and generated an estimated €12 million in its first year. By FY 2023/24, it had reached approximately €1.618 billion, and by FY 2024/25, it had crossed the €2 billion mark. The table below places NORMAL and ACTION side by side across their respective growth histories.

The critical comparison is not the absolute size of the numbers. It is the growth rate at equivalent stages of maturity. In the five years prior to crossing the €2 billion revenue threshold, ACTION grew at a compound annual rate of approximately 27%. This was already an exceptional result, well above anything its European retail peers were achieving in the same period. NORMAL, in the equivalent five-year window leading to that same €2 billion milestone, grew at a CAGR of approximately 39%.

The FY 2023/24 results underscore just how much momentum is in the system. NORMAL reported net sales of approximately DKK 12.1 billion (roughly €1.618 billion at prevailing exchange rates), representing close to 40% growth year on year, driven by the opening of 222 new stores across 8 markets. As of November 2025, the chain was operating 981 stores, up from a handful a decade earlier.

NORMAL opened 222 stores in a single fiscal year. That is not incremental growth. That is a land-grab.

The Margin Story: Where NORMAL Is, and Where ACTION Was

One of the questions that arises most frequently when discussing NORMAL with investors and brand managers is profitability. A CAGR of 39% is impressive, but if it is being purchased at the cost of economic sustainability, the comparison with ACTION becomes less instructive.

The evidence here is more nuanced, and ultimately reassuring. NORMAL's current EBITDA margin, at approximately 6 to 7%, is modest in absolute terms but entirely consistent with the economics of a discount variety model at this stage of expansion. A retailer opening 200+ stores per year is necessarily running ahead of its fixed cost base. Ramp costs, new market entry expenses, and the time required for new stores to reach mature-state contribution margins all compress near-term profitability. This is not a hidden structural weakness. It is the predictable arithmetic of rapid geographic rollout.

ACTION's own margin history confirms this dynamic precisely. Action's operating EBITDA margin was approximately 11% in the year it crossed €1 billion in revenue, a figure that remained broadly stable through its most aggressive expansion phase before expanding toward 13%, 14%, and eventually 15% as scale benefits materialized. It fluctuated between 9% and 12% through its most aggressive expansion phase. Only as store density increased, logistics networks matured, and the fixed cost base was leveraged across a larger revenue base did margins begin to expand meaningfully toward 13%, 14%, and eventually 15%.

NORMAL appears to be on the same path. As new store openings moderate in maturing markets and the contribution of like-for-like sales growth increases as a proportion of total revenue growth, operating leverage will assert itself. The question is not whether margins will improve, but over what timeframe, and that depends heavily on how aggressively NORMAL continues to invest in geographic expansion.

A related data point worth noting is NORMAL's gross margin structure. At approximately 20%, NORMAL's gross margins are below those of most specialty retailers in adjacent categories, such as Matas in Denmark, which operates at roughly 50% gross margins. This is deliberate. NORMAL's model depends on passing value to the consumer through everyday pricing rather than capturing it on the income statement. The strategic bet is that volume, frequency, and market share will ultimately generate more economic value than a higher-margin, lower-volume model. The evidence from ACTION suggests that bet is well-placed.

Geography: How Much Room Is There?

NORMAL's current footprint spans eight countries, with its largest markets being Denmark, France, Norway, Finland, and Sweden. The chain has approximately 981 stores as of late 2025. For reference, ACTION operates in excess of 3,000 stores across more than 12 European countries. The implication is straightforward: even if NORMAL were only to replicate ACTION's current store footprint in the markets where it already operates, there is a potential doubling of the estate ahead. And NORMAL has not yet entered some of Europe's largest retail markets.

The Scandinavian home base gives NORMAL a natural advantage in terms of brand credibility and operational density, but it also reflects how early the international expansion story truly is. France appears to be the most significant international bet to date, and early indications suggest the concept is translating well. The discount variety format has proven to be culturally portable across Northern and Western Europe, and there is no structural reason why NORMAL's core proposition would not perform in Germany, the Benelux region, Spain, or the United Kingdom.

What makes the geographic opportunity particularly significant is the cost structure of expansion. NORMAL's stores are not expensive to open. The no-frills format, the relatively compact footprint, and the operational simplicity of the model mean that capex per new store is low relative to comparable formats. This is what allows a 200-plus store opening program to be economically viable while the overall margin structure is still maturing.

What This Means for Brands and Manufacturers

For the brand managers, category directors, and commercial leaders who read CARRARA Advisory's work, the strategic implications of NORMAL's rise are immediate and practical.

NORMAL sells branded products, not private label. This is a critical distinction from many other discount formats. The value proposition to the consumer is precisely that they are buying the brands they know and trust, at prices they would not expect. For a brand appearing in NORMAL's assortment, this creates a volume opportunity, but also a channel management question. At what price point is NORMAL selling? In which markets? And what does that communicate about the brand to consumers who encounter it in NORMAL's stores versus other channels?

These are questions that brands needed to work through with ACTION roughly a decade ago. Most arrived at a workable answer, and the brands that engaged constructively with ACTION early generally found a way to capture the volume upside while protecting their overall price architecture. The same process will need to happen with NORMAL, and the brands that engage now, when NORMAL is still below €2.5 billion in revenue and operating in fewer than ten markets, will be better positioned than those that wait until NORMAL is a €5 or €10 billion retailer.

There is also a more fundamental point about what NORMAL's growth tells us about the European consumer. The sustained success of ACTION, NORMAL, and the discount variety format more broadly is not merely a reflection of post-pandemic thrift or cost-of-living pressures, though these have clearly acted as tailwinds. It reflects a structural shift in how a broad cross-section of European consumers think about value. Middle-income households, who might have previously felt that discount stores were not for them, have discovered that buying branded personal care and household products at NORMAL prices is simply rational behavior. This is not a trade-down. It is a recalibration.

The brands that engage with NORMAL now, while it is below €2.5 billion, will be better positioned than those that wait until it is a €10 billion retailer.

The Investment Angle: A Privately Held Rocket

NORMAL is privately held, which limits the transparency available to external observers and means that a direct investment in the company is not possible through public markets. The founding shareholders, Mouritsen and Kristensen, retain control, and the company has not indicated any intention to list in the near term.

That said, the indirect investment logic is compelling. Suppliers and logistics partners with meaningful exposure to NORMAL's growth are a play on the trajectory described in this article. More broadly, NORMAL's rise underscores the continued attractiveness of the discount variety format as an asset class. The listed European analogues, most notably B&M European Value Retail in the United Kingdom, offer some proxy exposure to the dynamics that NORMAL is now demonstrating in unlisted form.

For private equity and growth investors, NORMAL represents exactly the kind of operator that would generate significant interest if it were ever to seek outside capital or pursue a listing. A business growing at 30 to 40% per year, with a proven unit economic model, a scalable store format, and an addressable market of several hundred additional store locations across Europe, commands a premium multiple in any market environment. 3i invested approximately £106 million at buyout and had, as of 2023, received cumulative distributions of around £1.7 billion.

Watch This Space

When we wrote about ACTION, the argument was that a retailer most of Europe's strategic community had not yet taken seriously enough deserved serious attention. That argument proved correct.

The argument today about NORMAL is structurally identical, but the window is earlier. NORMAL is where ACTION was when ACTION was still a story that required explaining. In five years, it will require no explanation at all.

The CAGR comparison is not just a statistic. It is a signal. A retailer growing at 39% on the way to €2 billion, in a format that has already been proven at €16 billion by its closest comparable, is either an anomaly or the beginning of a pattern. Everything in the data, the store economics, the consumer behavior, the category dynamics, and the European geographic white space, suggests it is the latter.

NORMAL may well be the most interesting growth story in European retail that most people in European retail have not yet made a priority. The time to change that is now.