Beauty Under Siege: Tariffs, Trade Wars, and the Weight of Geopolitical Disruption

Executive Summary

The global beauty industry entered 2025 expecting a return to the solid growth trajectory that characterized 2023 and 2024. What it encountered instead was one of the most complex operating environments in recent memory. A combination of China demand deceleration, persistent currency headwinds, and the initial wave of U.S. tariff escalation produced aggregate reported revenue growth of just +0.5% across ten major companies tracked by CARRARA Advisory, down sharply from +4.9% in 2024. Strip out foreign exchange effects, and underlying organic growth was approximately +2.3%, still a meaningful deceleration but more representative of the industry's operational reality.

Tariffs, which received sustained management attention throughout 2025 and into 2026, are the focus of this report. Our analysis of official company disclosures across fourteen beauty and personal care companies reveals a quantifiable tariff impact of at least $440 million in beauty-relevant profit. Against a collective adjusted operating profit pool of approximately $17 billion for the ten companies in our core coverage, this represents at least 39 basis points of average adjusted operating margin compression and approximately 2.6% of the collective profit pool. The qualifier 'at least' matters: five sizable companies acknowledged tariff exposure but did not quantify it, meaning the true industry-wide figure is higher. For the companies most directly exposed, particularly E.L.F. Beauty, Estee Lauder, and Coty, the proportional impact is far more severe.

The challenge for 2026 is that this tariff burden, already material, is now being compounded by a new and less predictable shock: the military conflict involving Iran and Gulf states that erupted in late February 2026. Its implications for beauty, particularly through Middle East travel retail, oil-linked input costs, and broader consumer confidence, add a further layer of uncertainty to an industry that has not yet completed its recovery from the prior cycle of disruption.

At the industry level, the $440M in quantifiable tariff costs represents at least 39 basis points of average adjusted operating margin compression and approximately 2.6% of the collective profit pool. For E.L.F. Beauty, operating on an 11.1% adjusted margin, the tariff burden consumes an estimated 30% of operating profit.

The Tariff Landscape: What Companies Actually Disclosed

Unlike broader macroeconomic headwinds, tariffs lend themselves to quantification. Companies know which products they import, from where, and at what declared value. As a result, a meaningful number of companies in our coverage universe have provided specific dollar estimates of their tariff exposure, making this one of the most data-rich dimensions of the current operating environment.

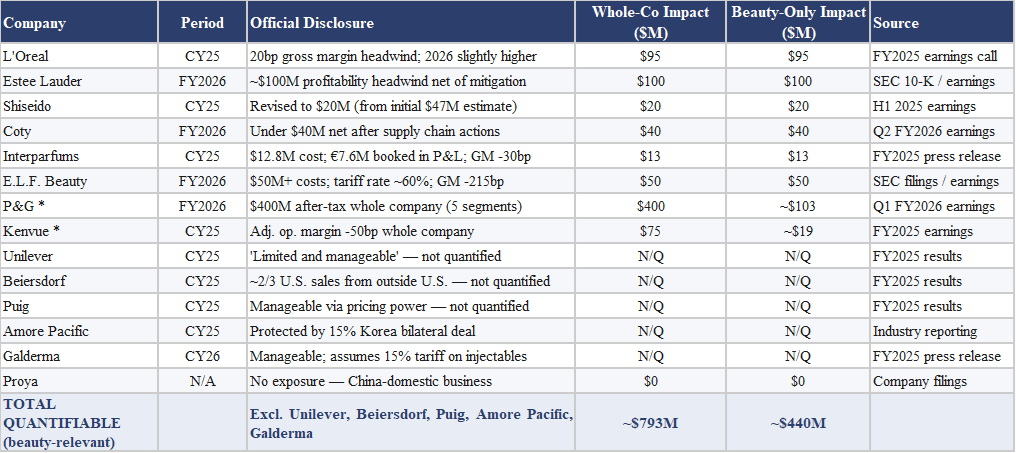

The table below aggregates official disclosures across fourteen companies, distinguishing between whole-company tariff impacts and beauty-relevant pro-rata allocations. For pure-play beauty companies the two figures are identical. For P&G, the $400 million after-tax whole-company figure has been allocated to beauty using actual segment revenues: P&G Beauty plus Grooming contributed $21.6 billion, or 25.7% of total group revenues, implying a beauty-attributable tariff cost of approximately $103 million. For Kenvue, the same methodology applied to the Skin Health and Beauty segment (approximately $3.9 billion, or 25.7% of group revenues) yields a pro-rata figure of approximately $19 million.

Exhibit 1: Declared Tariff Impact by Company

* P&G and Kenvue: whole-company figures allocated to beauty using actual segment revenues. P&G Beauty + Grooming = $21,626M = 25.7% of group. Kenvue Skin Health and Beauty = ~$3,900M = 25.7% of group. N/Q = not quantified in official communications. Sources: company press releases, SEC filings, and earnings call transcripts.

The aggregate of quantifiable beauty-relevant impacts reaches approximately $440 million. This is almost certainly a floor. Five sizable companies, Unilever, Beiersdorf, Puig, Amore Pacific, and Galderma, acknowledged tariff exposure in their official communications but declined to provide specific figures. Including reasonable estimates for those companies would push the industry-wide total meaningfully higher.

Among those that did quantify, the range of outcomes is wide and reflects fundamentally different supply chain architectures. L'Oreal, which manufactures approximately two thirds of what it sells in the U.S. domestically, reported a 20 basis point gross margin impact of approximately $95 million. At the other extreme, E.L.F. Beauty, which sources roughly 75% of its production from China, faces a tariff rate that has surged to approximately 60%, generating more than $50 million in additional annual costs and compressing gross margins by over 200 basis points.

Putting the Numbers in Perspective: Tariffs Against the Profit Base

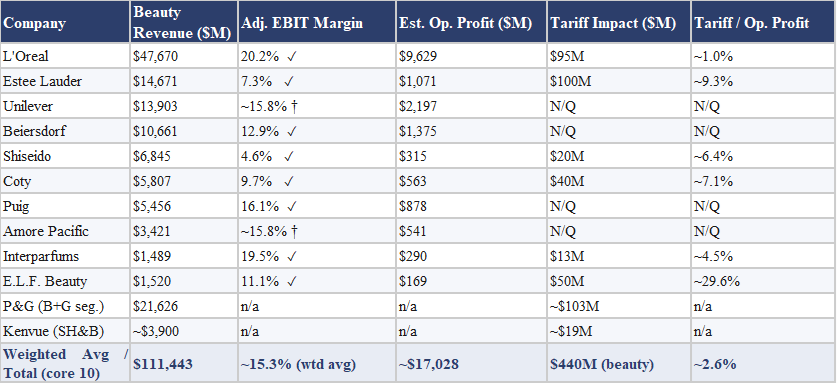

Absolute dollar figures tell only part of the story. To understand the true severity of tariff exposure, the impact must be measured against each company's profit base. The table below sets the tariff burden against adjusted EBIT margins and estimated operating profits. Where a company-specific beauty EBIT margin could not be confirmed from official disclosures, we apply the industry average of 15.8% as a proxy, flagged with a dagger symbol.

Exhibit 2: Tariff Impact as a Proportion of the Operating Profit Base

✓ = confirmed from official 2025 filings (adjusted operating profit): L'Oreal 20.2%, Estee Lauder 7.3%, Beiersdorf 12.9%, Shiseido 4.6%, Coty 9.7%, Puig 16.1%, Interparfums 19.5%, E.L.F. 11.1%. † = 15.8% group average applied as proxy (Unilever, Amore Pacific). P&G and Kenvue shown at segment revenue level; adjusted operating margins not disclosed at segment level. Sources: CARRARA Advisory tracking model; company press releases and SEC filings.

At the aggregate level, the $440 million in quantifiable beauty tariff costs represents at least 39 basis points of average adjusted operating margin compression and approximately 2.6% of the estimated $17 billion collective profit pool. Because five companies acknowledged exposure without quantifying it, both figures understate the true industry-wide burden. The story at the individual company level is more differentiated and in several cases more alarming.

E.L.F. Beauty is the most acutely affected company in the group on a proportional basis. With a confirmed adjusted operating margin of 11.1%, its profit base on $1.5 billion in revenues stands at approximately $169 million. Against that base, the $50 million tariff floor represents roughly 30% of operating profit, a burden that is almost entirely attributable to its concentrated China sourcing at a tariff rate that has surged to approximately 60%. Estee Lauder, whose confirmed adjusted operating margin of 7.3% reflects years of China-related headwinds and ongoing restructuring, absorbs a tariff drag equivalent to approximately 9% of its operating profit. Coty, with a confirmed adjusted operating margin of 9.7% generating approximately $563 million in operating profit, faces a 7% tariff-to-profit ratio, manageable in isolation but compounding an already stressed margin recovery trajectory. Shiseido, on a confirmed margin of just 4.6%, absorbs a drag equivalent to roughly 6% of its operating profit.

At the other end of the spectrum, L'Oreal's confirmed adjusted operating margin of 20.2% generates a profit base large enough to absorb its $95 million tariff cost as roughly 1% of earnings. Puig's confirmed 16.1% margin similarly provides meaningful buffer. The divergence confirms that tariff exposure is not a uniform industry tax but a structural discriminant that penalizes companies with thin margins and China-heavy supply chains while leaving well-capitalized, domestically anchored players comparatively unscathed.

E.L.F. Beauty's $50M tariff burden consumes approximately 30% of its operating profit on an 11.1% adjusted margin. For L'Oreal at 20.2%, the same tariff policy costs roughly 1% of earnings. Tariffs are a structural discriminant, not a uniform tax.

How Companies Are Responding: Three Mitigation Strategies

Faced with tariff headwinds ranging from modest to severe, the companies in our universe have pursued three broad categories of response, often in combination.

The first and most immediate is pricing. Almost every company with material U.S. import exposure has implemented selective price increases. Interparfums raised U.S. prices by 6 to 7% on the day tariffs took effect. E.L.F. implemented a one dollar increase on key products in August 2025. Puig and Coty have both signaled that their brand strength gives them room to pass through a portion of the cost increase, though both acknowledge a ceiling beyond which pricing becomes a volume risk rather than a margin solution.

The second is supply chain diversification. E.L.F. Beauty has been the most explicit and aggressive on this front, committing to a shift of production from China toward Vietnam, Indonesia, and Mexico. The structural challenge for most fragrance players, noted explicitly by Interparfums CEO Jean Madar, is that certain components, particularly glass bottles and precision pumps, simply cannot be sourced domestically. The U.S. glass manufacturing industry for prestige fragrance packaging no longer exists at any meaningful scale, which means full tariff avoidance through reshoring is structurally impossible for the category regardless of the ambition of the response.

The third strategy is geographic revenue diversification. Companies that have accelerated their international expansion are partially insulating their overall earnings from U.S. tariff costs. E.L.F.'s international revenues, now approximately 20% of total sales and growing significantly year on year, sit entirely outside the scope of U.S.-China tariff dynamics. L'Oreal's presence across more than 150 markets means U.S. margin compression from tariffs is diluted across a vast and diversified revenue base. The strategic implication is clear: in an era of persistent tariff risk, geographic revenue diversification is not just a growth strategy but a risk management imperative.

2025 in Context: A Year of Compounding Headwinds

To understand why tariffs matter as much as they do, it is important to situate them within the broader 2025 operating environment. Tariffs were not the industry's primary challenge in 2025. They were one layer in a multi-layer compression.

China was the dominant headwind. The world's second-largest beauty market continued its deceleration through most of 2025, with consumer confidence remaining subdued and the structural shift away from aspirational premium spending persisting longer than most company forecasts had anticipated. For Estee Lauder, Shiseido, and Coty, this translated directly into revenue declines of 3 to 5% on an underlying basis. The companies that had spent the prior decade building concentrated exposure to China prestige skin care and Asia travel retail found themselves carrying that exposure into a market that was structurally slower than the one they had built for.

Currency was the second major headwind. The U.S. dollar's sustained strength against the euro, yen, and Korean won subtracted approximately two percentage points from reported headline growth across the ten-company group, representing a translation loss with no underlying commercial cause. The companies most penalized, L'Oreal, Beiersdorf, Puig, and Coty, are the most euro-denominated businesses, and they would benefit mechanically from any dollar softening without any change in their commercial performance.

Against this backdrop, tariffs arrived as an incremental burden on an industry already navigating significant pressure. The second half of 2025 showed meaningful sequential improvement across several companies, with five of the ten delivering better H2 than H1 growth rates. Estee Lauder's swing from -10.9% in H1 to +4.7% in H2 was the most dramatic. But the trajectory into 2026 has been complicated by a new and entirely different category of risk.

The 2026 Gulf Conflict: A New and Uncertain Headwind

On February 28, 2026, U.S. and Israeli forces launched joint strikes on Iran, triggering a military conflict that has already produced significant disruption across the Gulf region. Airport closures and restrictions in Dubai, Abu Dhabi, and Doha; temporary store closures by major luxury and beauty retailers across the UAE, Kuwait, Bahrain, and Qatar; and sharp spikes in oil and energy prices have added a new dimension of uncertainty to an industry still absorbing the after-effects of 2025.

The Middle East has become a strategically important market for global beauty and luxury. Industry analysts at Altagamma estimate that the region accounts for approximately 5 to 6% of total luxury and beauty industry revenues globally, equivalent to roughly 23 billion euros, with more than half of that concentrated in the UAE. For travel retail specifically, a channel that beauty relies on disproportionately for premium fragrance and skin care sales, the region has been among the fastest-growing globally.

Oxford Economics estimates that inbound arrivals to the Middle East could fall between 11 and 27% year on year in 2026, depending on the duration and resolution of the conflict, potentially wiping out between $34 billion and $56 billion in visitor spending.

For beauty companies, there are three distinct channels of impact. The most direct is travel retail disruption. Premium fragrance sales in particular are heavily concentrated in airport duty-free environments, and the combination of flight cancellations, airport closures, and reduced tourist flows translates quickly into lost high-margin revenue. Companies like Puig, Interparfums, and Coty, which have built significant prestige fragrance businesses that rely on travel retail for both sales and brand building, are meaningfully exposed.

The second channel is oil-linked input costs. Beauty products are petrochemical-intensive. Synthetic fragrances, many packaging materials, and a significant portion of preservative and emulsifier inputs are derived from petrochemical chains linked to crude oil. The Strait of Hormuz disruption has already pushed Brent crude prices up by 10 to 13% since the conflict began. If oil prices sustains at or above the $100 per barrel level that analysts have cited as a plausible scenario, this will feed through into beauty company cost of goods over the course of 2026, adding a further margin headwind on top of the tariff impact already in the numbers.

The third channel is consumer confidence. The beauty industry's resilience through prior periods of economic uncertainty has rested partly on the argument that beauty is an accessible luxury where consumers continue to spend even when larger discretionary purchases are deferred. That dynamic remains broadly valid. But prolonged geopolitical instability, combined with tariff-driven price increases and oil-linked inflation, has the potential to soften that resilience at the margin, particularly in the aspirational mid-tier where brand loyalty is least entrenched.

The Gulf conflict adds a third simultaneous headwind to an industry still absorbing China deceleration and a 39bp tariff margin drag. The compounding effect is unlike anything the industry has navigated in the modern era.

Strategic Implications for 2026 and Beyond

The convergence of three independent but simultaneous headwinds creates a 2026 operating environment that is more challenging than most company guidance published in early 2026 had assumed. Several strategic implications follow from this analysis.

Supply chain geography has become a first-order strategic asset. Companies with diversified or domestically anchored U.S. production are structurally better positioned to absorb tariff risk than those with concentrated China or European sourcing. The capital allocation question for boards and management teams is no longer whether to invest in supply chain diversification but how quickly and at what cost. For fragrance companies constrained by the absence of domestic U.S. glass manufacturing infrastructure, this is a problem that cannot be solved at the company level and may ultimately require an industry-level response including regulatory engagement.

Pricing power is being tested simultaneously across multiple cost vectors. Companies face the challenge of passing through tariff-related cost increases, absorbing higher input costs from elevated oil prices, and maintaining volume in markets where consumer confidence is under pressure. The companies best positioned are those with genuine brand equity that earns consumer loyalty even at higher price points. The fragrance category has demonstrated this capacity repeatedly. The companies most at risk are those in the aspirational middle tier, where neither brand premium nor accessible price positioning offers clear protection.

Margin management has moved to the top of the strategic agenda in a way it has not been for most of the past decade. An industry accustomed to discussing growth rates and market share is now having a different kind of conversation: one about which cost lines can be held, which can be passed through, and which structural changes are needed to protect the profit base against a sustained multi-headwind environment. The 15-16% average EBIT margin that characterizes the industry today, already below the levels of the mid-2010s for many companies, leaves limited buffer against simultaneous tariff costs, input inflation, and potential volume softness.

Finally, the compounding nature of these challenges calls for caution in reading the second-half 2025 improvement as a signal of durable recovery. The improvement was real, particularly for Estee Lauder, Coty, and Shiseido, but it was achieved against relatively easy prior-year comparisons and before the full impact of 2026 tariff rates, Gulf tensions, and the persistence of Chinese demand softness had fully manifested.

Conclusion

The global beauty industry is navigating an environment defined by the simultaneous arrival of multiple structural headwinds, none of which has a clear near-term resolution. Tariffs represent the most quantifiable element: at least $440 million in beauty-relevant profit impact across the companies that disclosed specific figures, representing at least 39 basis points of average adjusted operating margin compression and approximately 2.6% of the collective profit pool. Given that five companies acknowledged exposure without quantifying it, the true industry-wide figures are higher. The individual company experience ranges from manageable at L'Oreal's approximately 1% of operating profit, to severe at E.L.F. Beauty's approximately 30% and Estee Lauder's approximately 9%.

But tariffs are only one dimension of the challenge. China demand deceleration, which drove most of the 2025 growth shortfall, has not fully resolved. Currency headwinds, which subtracted approximately two percentage points from reported aggregate growth in 2025, remain in place for European and Asian reporters. And the 2026 Gulf conflict has added a new and as yet unquantified layer of disruption through travel retail, input cost inflation, and consumer sentiment channels.

The companies best positioned for this environment share three characteristics: supply chain flexibility that reduces tariff exposure or enables rapid adaptation, genuine brand equity that supports pricing power across multiple cost headwinds, and geographic revenue diversification that prevents any single regional shock from dominating group performance. These structural advantages are not uniformly distributed, and the divergence between well-positioned and poorly-positioned companies is likely to widen before it narrows.

The beauty industry has a long track record of resilience. Its fundamental consumer proposition, that investment in personal care and appearance delivers disproportionate emotional and social value relative to its cost, remains intact. But resilience does not mean immunity. The industry's 2026 performance will be determined not by whether these headwinds are present but by the quality and speed of execution with which individual companies respond to them.