Beauty technology devices have moved from the edge of the industry to one of its most strategically important growth frontiers.

What was once a niche space dominated by cleansing brushes and salon adjacent hair removal systems has expanded into a broad ecosystem that now includes facial rejuvenation tools, scalp and hair growth platforms, connected diagnostics, body contouring devices, and increasingly sophisticated clinic to home continuation systems. Across syndicated market definitions, skincare devices remain the largest product category, accounting for more than one third of beauty tech revenue in some recent studies. This matters because the category is no longer simply about gadgets.

Beauty devices now sit at the intersection of efficacy, ritual, personalization, and measurable outcomes. They change not only what consumers buy, but how they engage with treatment consistency, visible proof, and repeat replenishment ecosystems.

For decades, beauty value creation was driven primarily by chemistry. Competitive advantages came from better formulas, stronger ingredient claims, superior sensoriality, and increasingly segmented routines. That model is now being structurally expanded.

A new layer of value creation is emerging at the intersection of hardware, skincare, software, and guided treatment protocols. LED masks, microcurrent sculpting devices, radiofrequency lifting systems, IPL hair removal tools, scalp stimulation helmets, and connected skin diagnostics are moving beauty from passive application toward active participation. Recent market reports consistently point to smart connectivity, AI enabled analysis, and multifunction design as the next major wave of category innovation.

This shift is not merely creating a new product category; it is redefining the architecture of the beauty routine itself.

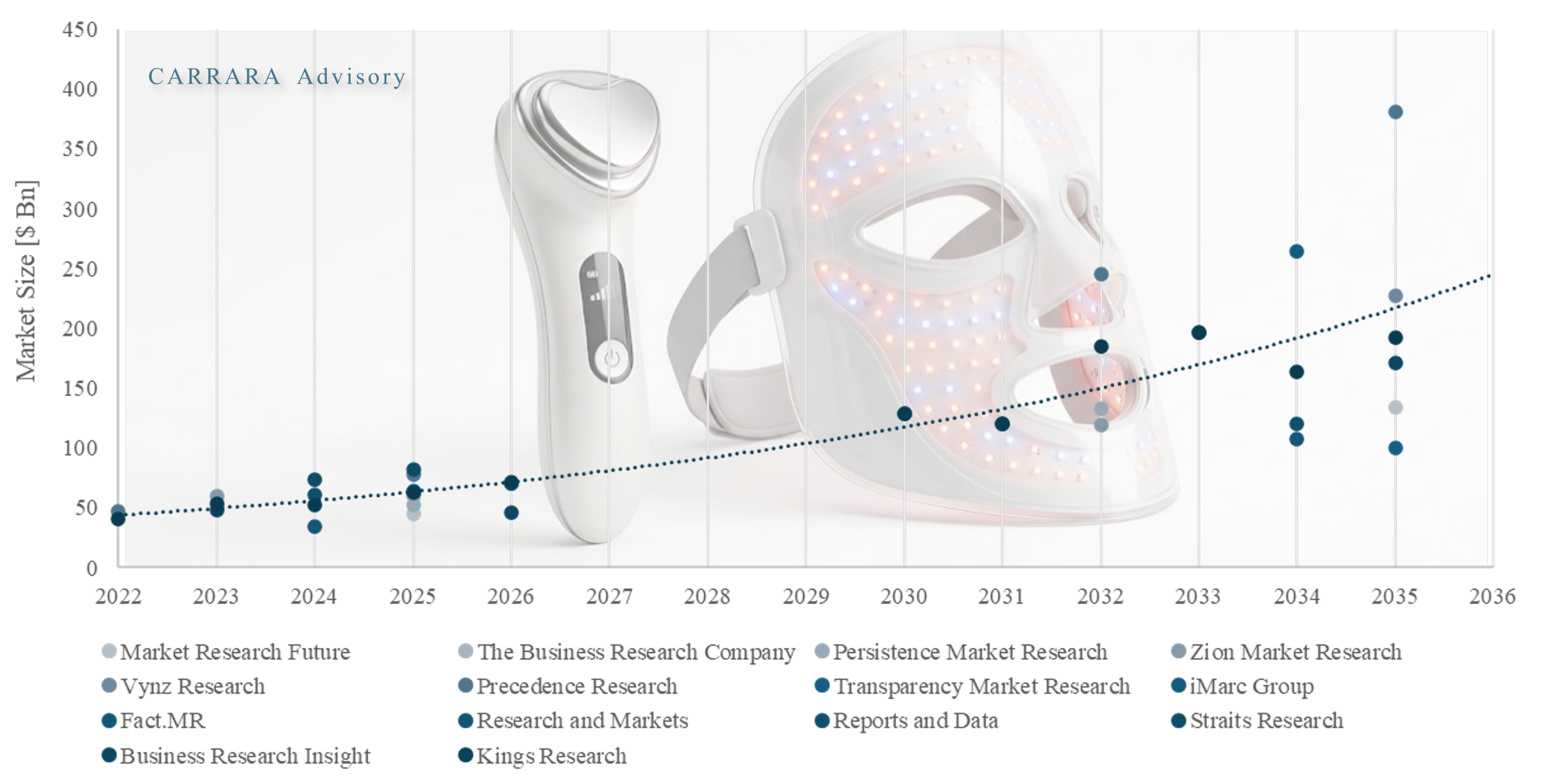

Based on the cross-source dataset, the 2025 global beauty tech devices market sits within a corridor of $45 billion to $82 billion, with a practical midpoint of $63.5 billion. The more important question, however, is whether beauty devices remain a premium hardware adjacency or evolve into the operating layer of modern beauty ecosystems. That distinction drives radically different market outcomes through 2035.

At Carrara Advisory, we believe this transition represents one of the most underappreciated value creation opportunities in the consumer sector today, and one that most incumbent beauty organizations are still significantly underwriting.

The Beauty Tech Devices Strategic Landscape

The beauty tech devices market is best understood through the interaction of three layers: segment economics, player archetypes, and future value creation paths.

At the segment level, today’s market is anchored by facial treatment devices, which remain the category’s largest and most strategically influential profit pool. LED therapy, microcurrent sculpting, radiofrequency tightening, ultrasonic infusion, and pore cleansing systems have become the leading expression of the clinic to home migration. These segments are particularly attractive because they combine premium pricing, visible before and after outcomes, and high compatibility with repeat ritual behaviors.

The second major segment is hair removal and IPL, which continues to benefit from one of the clearest consumer ROI equations in beauty. The long-term substitution of salon visits with home use systems creates durable demand and strong resilience even in more cautious spending environments.

The third major growth engine is hair growth and scalp technology, a segment with unusually strong emotional relevance and willingness to pay. Low level laser helmets, scalp microcurrent systems, and follicle stimulation devices are increasingly capturing value at the intersection of beauty, wellness, and aging optimization.

The fourth layer includes professional aesthetic and clinic grade systems, which remain essential because they shape efficacy expectations and often serve as the innovation pipeline for future consumer miniaturization.

The fifth segment, body contouring and beauty wellness crossover devices, reflects the category’s convergence with self-optimization and recovery culture.

The sixth and most strategically consequential layer is AI connected diagnostics and adaptive treatment systems, which may ultimately determine whether the category evolves into a platform economy.

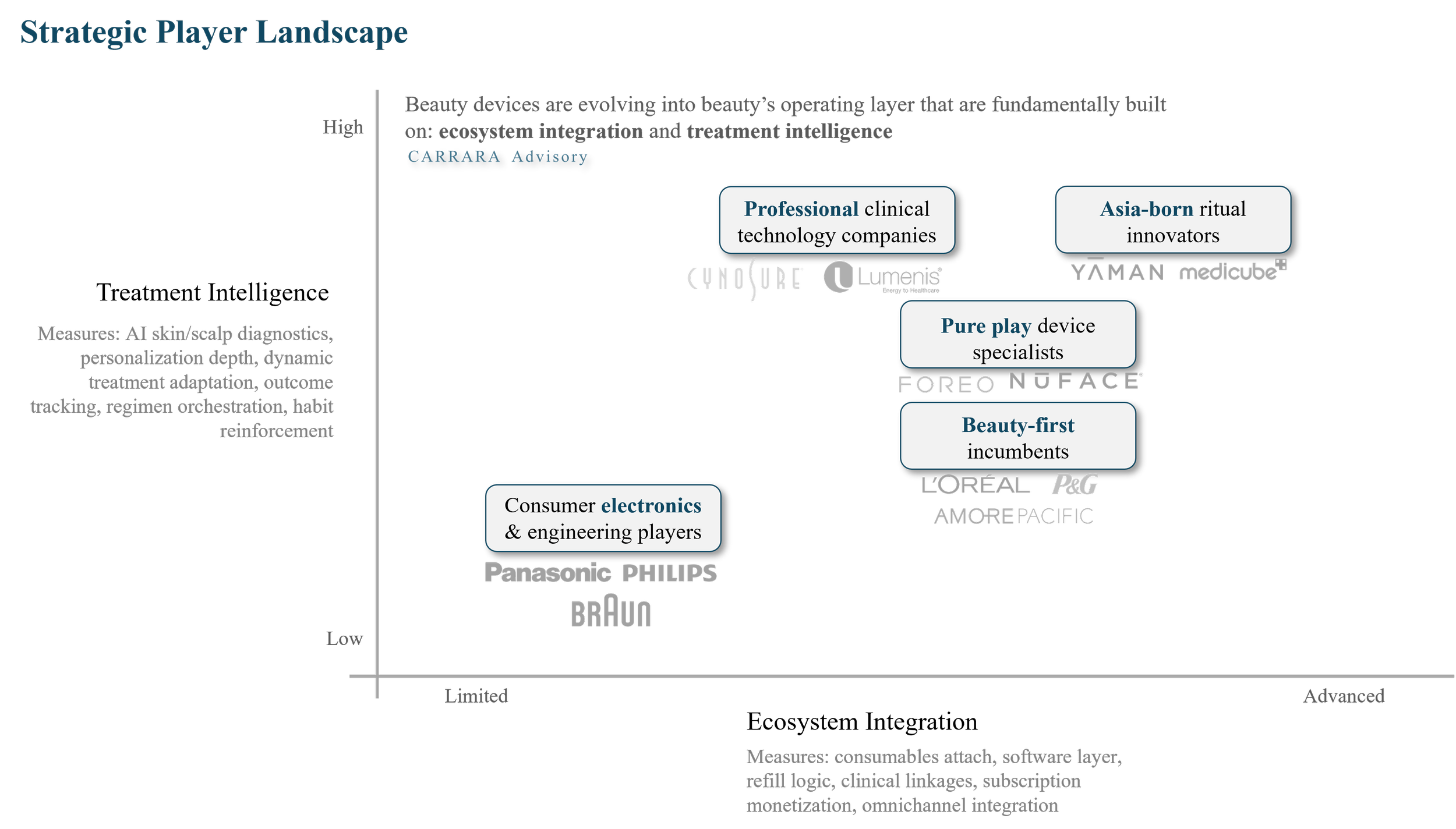

Across these six segments, five player archetypes currently shape competitive intensity. Beauty first incumbents compete through trust, skincare ecosystems, and omnichannel scale. Consumer electronics and engineering players compete through miniaturization, safety, manufacturing discipline, and battery performance. Pure play device specialists lead in creator education, ritual design, DTC conversion, and premium industrial design. Professional clinical technology companies influence efficacy standards and aspirational treatment benchmarks. Asia born ritual innovators increasingly set the pace in launch frequency, format elegance, and clinic inspired routine logic.

The interaction of these segments and player archetypes leads directly into three distinct future value creation paths. In the base case, value pools remain concentrated in premium hardware and adjacent consumables. In the acceleration case, value expands through mainstream ritual adoption, content loops, and increased routine frequency. In the platform case, the device becomes the control layer for a broader ecosystem including diagnostics, adaptive protocols, software subscriptions, replenishment logic, and professional escalation pathways.

This framework helps explain why the market appears relatively stable in the present yet diverges dramatically in long-term forecasts. The current 2025 market corridor of $45 billion to $82 billion reflects somewhat agreement on today’s hardware demand. The 2035 spread from roughly $110 billion in conservative scenarios to $380 billion in platform scenarios reflects disagreement on whether devices remain products or become systems. That is the central strategic question for the decade ahead.

CARRARA Framework: The Four Stages of Beauty Tech Value Migration

The long-term winners in beauty devices are not determined by hardware innovation alone. They are determined by how effectively brands move across four stages of value creation: Hardware, Ritual, Ecosystem, and Platform.

The market’s wide 2035 forecast corridor can be best understood through this lens. The lower end of the range reflects categories that remain primarily in the hardware stage. The midpoint acceleration case assumes successful migration into ritual and ecosystem economics. The upper end of the range reflects brands that successfully evolve into platform models, where diagnostics, software guidance, and replenishment systems materially expand lifetime value.

To help our clients navigate this complexity, we developed theCARRARA Beauty Tech Value Migration Frameworkwhich maps how beauty tech devices evolve from hardware products into ecosystem control layers.

Stage 1: Hardware

At the first level, value is concentrated in the physical device itself. The business model is driven by:

premium pricing, industrial design, engineering, channel distribution, and perceived efficacy. Examples include LED masks, IPL tools, cleansing brushes, and microcurrent devices sold as standalone hero products.

In this stage, growth is largely a function of: innovation cycles, influencer visibility, and retail conversion. This is where many brands start, but it is also where commoditization risk is highest.

The question at this stage is simple: Is the device differentiated enough to command premium pricing?

Stage 2: Ritual

The second stage begins when the device becomes part of a repeatable consumer behavior loop. The source of value shifts from product ownership to usage frequency and habit formation. At this level, the winning brands are not merely selling technology. They are designing daily routines, weekly protocols, guided treatment paths, before and after milestones, and creator education loops. This stage is strategically critical because frequency drives:

better outcomes, stronger retention, and lower churn. This is where brands such as Medicube, CurrentBody, and FOREO have created meaningful advantages.

The key advisory question becomes: How deeply is the device embedded in consumer ritual?

Stage 3: Ecosystem

The third stage is where the device starts to unlock adjacent revenue pools. At this level, value migrates from hardware margin into: conductive gels, proprietary serums, attachment heads, refills, software guidance, treatment plans, and replenishment subscriptions.

The device becomes the front door to higher lifetime value monetization. This is the point where the category begins to behave less like beauty accessories and more like connected consumer ecosystems. This is the stage where strategic value often compounds fastest.

The core question at this level is: How much recurring revenue sits behind the device sale?

Stage 4: Platform

The fourth and most advanced stage is where the device becomes the operating layer of beauty outcomes. At this point, the product is no longer the endpoint. It becomes the interface through which data, diagnostics, adaptive intensity, skin scanning, progress analytics, replenishment logic, and even professional escalation pathways are orchestrated.

This is where beauty begins to resemble: connected fitness, digital therapeutics, and precision wellness. In this stage, value creation shifts toward: software subscriptions, AI recommendations, personalization engines, and data enriched retention loops. This is the scenario embedded in the most aggressive 2035 market forecasts.

The defining question here is: Does the brand own the treatment intelligence layer?