The Strategic Reinvention of Private Label in Beauty and Wellness

Beauty and Wellness Private Labels List

CHF 0.00

This is a list of retailers and their beauty private labels

Walk into a modern beauty retailer today and the shift is difficult to miss. Alongside the established multinational brands sits an increasingly sophisticated portfolio of retailer owned products. At Boots it is No7. At dm-drogerie markt it is Balea and alverde. At Sephora it is Sephora Collection. At Rossmann it is Isana. At Shoppers Drug Mart it is Quo Beauty.

None of this is entirely new. Retailers have operated beauty private labels for decades. No7 itself dates back to 1935, while European pharmacy and drugstore chains have long sold retailer owned skincare, personal care, and wellness products. What has changed is not the existence of retailer brands, but their strategic importance, sophistication, and commercial ambition. Retailers are no longer treating private label as a secondary activity primarily designed to improve margins. Increasingly, they are building full beauty brands with dedicated positioning, innovation strategies, sustainability commitments, clinical claims, and marketing investments that compete directly with multinational suppliers occupying the same shelves.

As part of this research, CARRARA Advisory mapped nearly 100 beauty and wellness retailers across Europe, North America, Asia Pacific, Latin America, the Middle East, and Africa operating private label programs across skincare, makeup, haircare, wellness, fragrance, and personal care. The findings point toward a broader structural shift within the industry. Retailers are progressively repositioning themselves from distributors into brand owners.

A Market Growing Faster Than National Brands

The numbers help explain why retailers continue to expand private label investment.

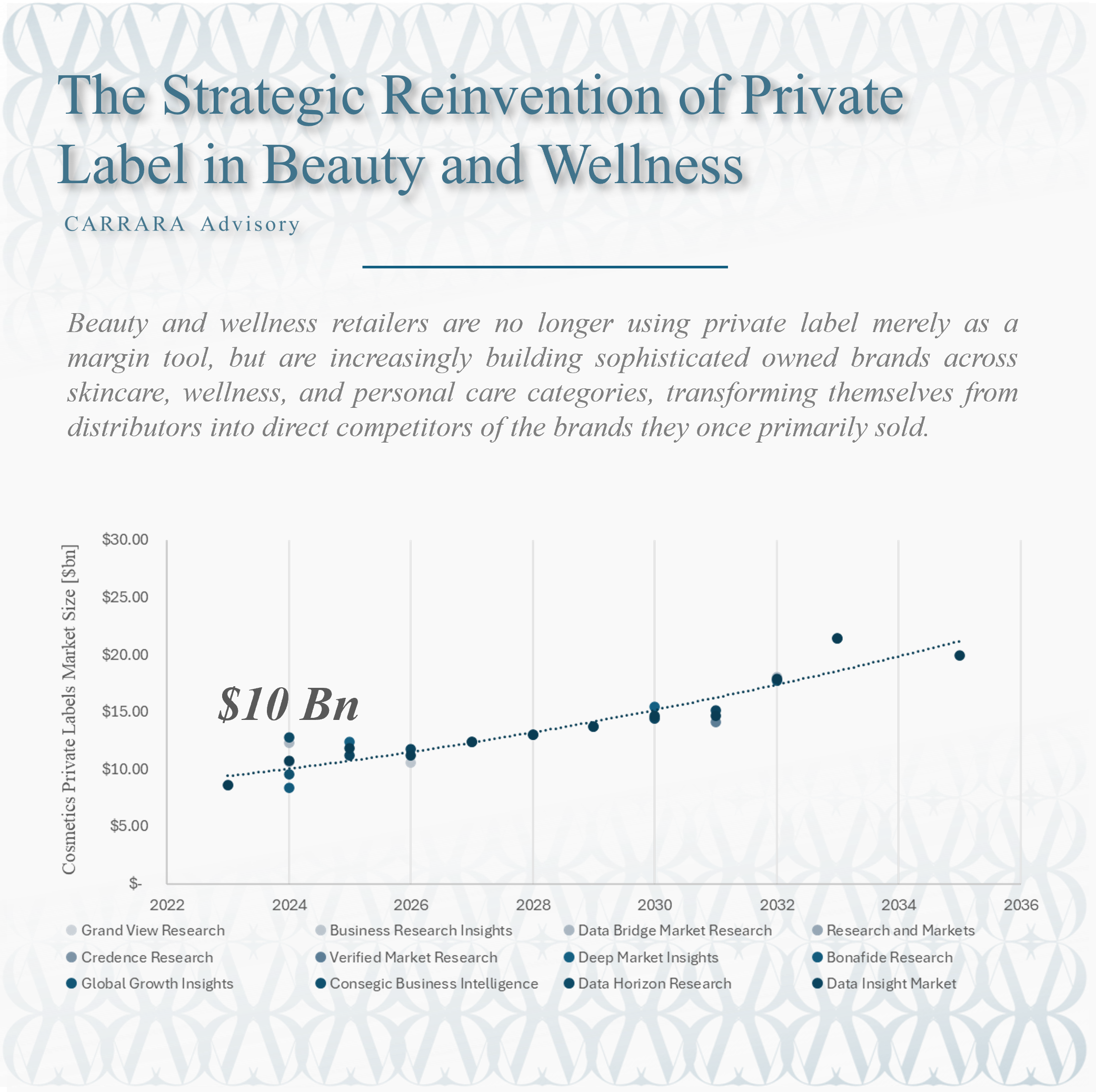

The global private label cosmetics market was valued at approximately $10.7 billion in 2024 and is projected to reach roughly $14.7 billion by 2030, growing at a compound annual growth rate of 5.4 percent. Across all consumer categories, private label sales in the United States reached a record $271 billion in 2024 according to PLMA and Circana data, growing 3.9 percent year over year compared with approximately 1 percent growth for national brands. Beauty and personal care ranked among the strongest performing private label categories during the same period.

Consumer perception has also shifted materially. Historically, retailer owned products were often associated with compromise. Consumers purchased them primarily to save money while accepting that performance, packaging, or formulation quality might be inferior to branded alternatives. That perception has weakened substantially over the past decade. NielsenIQ consumer data indicates that only a very small minority of consumers now perceive private label products as inherently inferior.

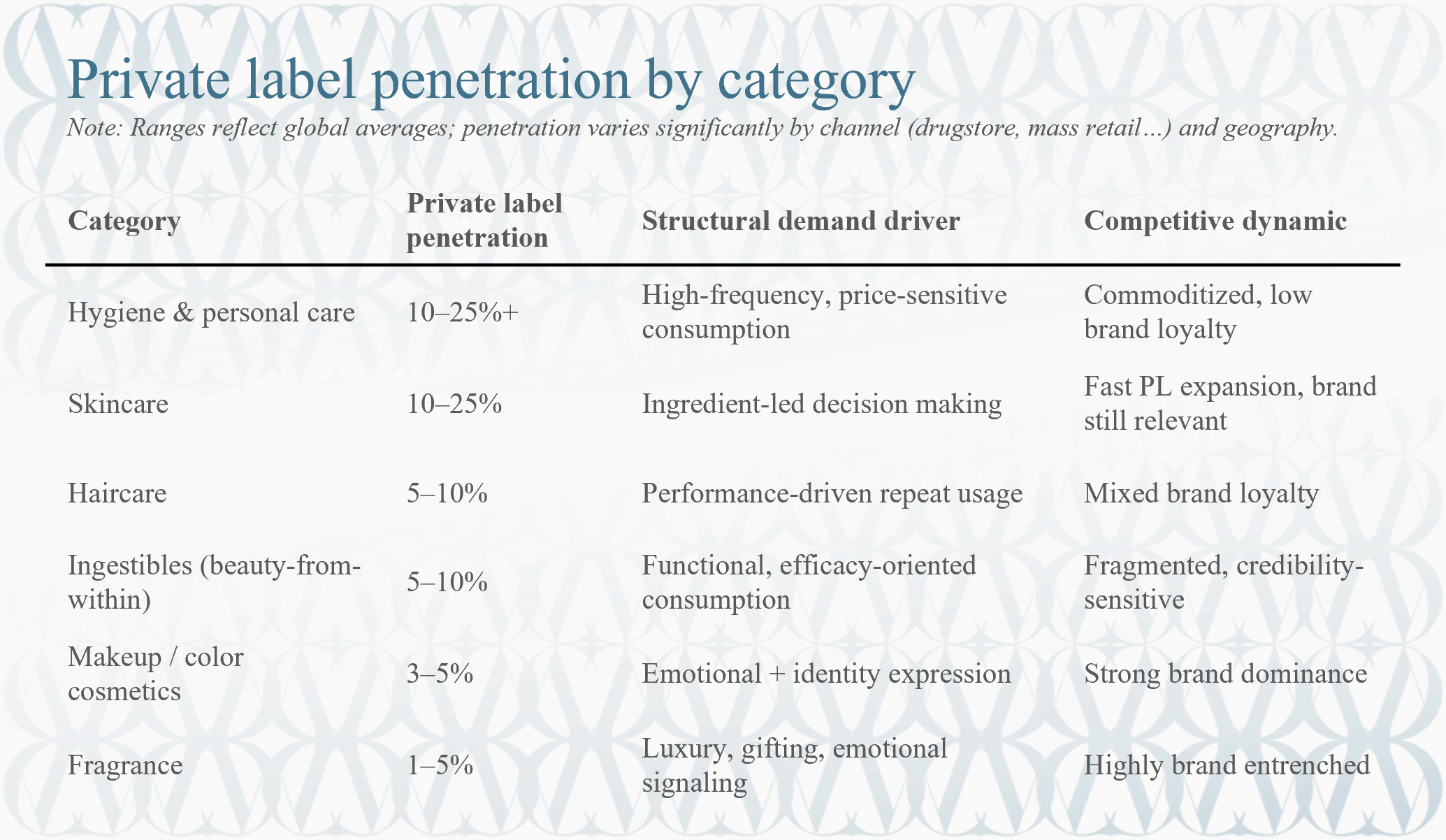

Private label penetration is structurally uneven, not uniformly weak

Private label remains a relatively small share of the global beauty and wellness product market at an aggregate level, estimated at approximately 2-5 percent overall. However, this headline figure masks a highly asymmetric structure across categories.

Penetration is materially higher in commoditized, high-frequency, and low-differentiation segments such as hygiene and basic personal care, where private label can reach 20–40 percent or more. In contrast, emotionally driven and identity-linked categories such as fragrance and prestige makeup remain heavily dominated by established brands, with private label penetration often in the low single digits.

Skincare occupies a structurally intermediate but strategically critical position. It accounts for approximately 41.7 percent of the global private label cosmetics market and is the fastest expanding zone for retailer owned brands. This is driven by a shift in consumer behavior toward ingredient-led purchasing, where decisions are increasingly based on functional components such as niacinamide, peptides, ceramides, and retinoid alternatives rather than brand heritage alone.

Ingestibles and beauty-from-within products show a similar but more fragmented pattern, where efficacy perception and ingredient transparency matter more than emotional branding, but trust barriers remain higher than in topical skincare.

Category dynamics explain why the global average remains low

The relatively low global penetration of private label is not the result of weak performance within categories, but rather a consequence of structural weighting effects across the beauty and wellness market.

High private label penetration is concentrated in lower-value or highly commoditized categories, while large, high-value segments such as fragrance, makeup, and premium haircare remain strongly brand-led. These categories also represent a disproportionate share of total market value, which mechanically lowers the global average despite strong performance in specific segments.

As a result, private label strength is best understood as category-specific dominance rather than system-wide penetration.

Private label growth is not incremental, but reallocation-driven

The structural takeaway is that private label expansion in beauty and wellness is not a uniform substitution effect across all categories. Instead, it represents a progressive reallocation of share within specific segments where functional differentiation is low and consumer decision-making is increasingly rational and ingredient-based.

This has three strategic implications:

Growth will continue to concentrate in skincare, hygiene, and selected ingestibles rather than evenly across the portfolio.

Categories with strong emotional or symbolic value (notably fragrance and prestige cosmetics) will remain structurally resistant.

The overall market share of private label will remain relatively low in aggregate terms even as it becomes dominant in selected high-volume segments.

In other words, private label is not becoming “the default” in beauty. It is becoming the dominant model in specific, structurally favorable categories while remaining marginal in others.

Why Retailers Are Making This Move

The strategic logic behind retailer owned beauty brands extends well beyond simple margin improvement.

Margin arithmetic, properly understood. Margin economics remain attractive, particularly at scale. Retailer owned products frequently generate materially stronger gross margins than third party brands, especially when retailers successfully optimize sourcing and manufacturing. Across millions of annual transactions, even relatively modest improvements in category economics can produce meaningful profitability gains. Yet the economics themselves have evolved. Retailers are no longer simply sourcing low cost alternatives. Increasingly, they are investing in packaging design, sustainability initiatives, digital marketing, influencer partnerships, clinical validation, and product innovation. Modern private label programs increasingly resemble full brand building exercises rather than procurement projects.

Differentiation as a survival imperative. Differentiation has also become structurally more difficult in beauty retail. Assortments increasingly overlap across channels, while ecommerce has further reduced exclusivity and increased price transparency. Many retailers stock the same multinational portfolios, often at similar price points. In that context, retailer owned products become one of the few genuinely exclusive assets available to the retailer. Consumers may purchase multinational products through many channels, but Balea remains exclusive to dm and Sephora Collection remains exclusive to Sephora. Private label therefore functions not only as a profit driver but also as a mechanism for customer retention, traffic generation, and differentiation.

Data as a formulation weapon. The evolution of retailer data capabilities has strengthened this position further. Modern beauty retailers operate increasingly sophisticated loyalty ecosystems and transactional analytics platforms that provide broad visibility into consumer behavior across competing brands and categories. Retailers can observe which ingredients drive repurchase, which price points convert trial into repeat purchase most effectively, which pack sizes perform best geographically, and which emerging trends accelerate within specific demographic groups. This creates a form of market visibility that is uniquely valuable because retailers can compare consumer behavior across multiple competing brands simultaneously.

Customer lock-in and loyalty reinforcement. A shopper who becomes loyal to No7 moisturizer is, by definition, loyal to Boots. The private label creates a product-level dependency that reinforces channel preference in a way that stocking national brands cannot. This is especially valuable as digital commerce fragments traditional retail loyalty: owning a formulation that cannot be purchased elsewhere is one of the few remaining structural tools for driving physical store visits.

Negotiating leverage with brand manufacturers. A retailer that demonstrably competes with its own products holds a different bargaining position with national brand suppliers. The implicit threat — that shelf space can be reallocated to own brand if trade terms are unsatisfactory — is more credible when the own brand program is strong and growing. This dynamic has been well-documented in academic literature on retailer-manufacturer relationships and remains a live consideration in category management decisions across every major retail group.

Retailers are also increasingly using private label to occupy market spaces that multinational brands have underserved or addressed too slowly. Affordable clean beauty, ingredient focused skincare, vegan formulations, trend responsive launches, and entry level prestige products are all areas where retailer owned brands have gained traction. In some cases, retailers can move faster than established multinational competitors precisely because they face fewer internal constraints around legacy positioning, portfolio cannibalization, or global brand architecture.

Why Private Label Is Easier Than It Was Fifteen Years Ago

One of the most overlooked drivers behind the expansion of retailer owned beauty brands is the transformation of the manufacturing ecosystem itself.

Fifteen years ago, launching a credible beauty line required capabilities that many retailers simply did not possess internally. Product development cycles were longer, packaging supply chains were less flexible, formulation expertise was concentrated among large multinational groups, and trend cycles evolved more slowly. Today, the ecosystem supporting retailer owned beauty has become dramatically more sophisticated.

Modern contract development and manufacturing organizations increasingly provide turnkey capabilities extending far beyond production alone. Many manufacturers now support formulation development, packaging sourcing, regulatory affairs, claims substantiation, sustainability certification, trend analysis, and even positioning support. Ingredient innovation has also become substantially more democratized. Active ingredients that once differentiated prestige skincare brands are now broadly available through global ingredient suppliers, while social media has accelerated ingredient awareness among consumers themselves. Consumers increasingly search for niacinamide, peptides, ceramides, collagen, or microbiome related benefits before they search for specific brands.

The result is that barriers to entry have fallen while the importance of speed, agility, and execution quality has increased.

Two Distinct Retailer Models Are Emerging

Not all retailer private label strategies are built the same way. Broadly speaking, two operating models increasingly dominate the market.

The Integrated Brand Builder

A smaller group of retailers have evolved beyond traditional private label into something closer to vertically integrated consumer goods companies.

Boots represents one of the clearest examples. No7 has developed into one of the United Kingdom’s most recognized skincare brands, supported by dedicated product development teams, scientific partnerships, clinical testing programs, and standalone marketing investment. Walgreens Boots Alliance eventually consolidated several owned beauty brands under No7 Beauty Company, effectively creating an internal beauty portfolio organization. Similarly, dm-drogerie markt built Balea and alverde into highly recognizable brands with distinct positioning strategies and sustainability commitments. Shoppers Drug Mart repositioned Quo Beauty as a standalone beauty brand with its own visual identity and product philosophy rather than merely a store substitute.

These retailers increasingly resemble vertically integrated beauty groups rather than traditional retailers operating secondary private label ranges.

The Hybrid and Contract Driven Model

The larger portion of the market operates through hybrid development and outsourced manufacturing structures.

In this model, retailers retain ownership of positioning, pricing, packaging direction, trend strategy, and brand management while relying heavily on external manufacturing ecosystems for execution. Sephora operates through a hybrid structure combining internal brand management, external manufacturing partners, and selected support capabilities from the broader LVMH and Kendo ecosystem. Sephora Collection spans multiple categories including makeup, skincare, accessories, and body care, while manufacturing is distributed across specialist suppliers depending on category expertise.

Douglas similarly operates several retailer owned concepts through external development and manufacturing partnerships, while Rossmann manages a broad portfolio of private brands through an extensive supplier network.

Mass retail and grocery groups such as Target, Walmart, Carrefour, and Lidl generally prioritize scale, sourcing efficiency, and pricing architecture over internally built beauty innovation capabilities. Yet even within these models, expectations toward manufacturing partners have evolved substantially.

What Retailers Look For in a Contract Manufacturing Partner

Historically, cost and production capacity dominated supplier selection. Today, retailers increasingly evaluate manufacturers on a much broader range of strategic capabilities.

Formulation agility and trend responsiveness. Speed to market has become one of the most critical variables because beauty trend cycles have compressed dramatically. Viral ingredients, packaging formats, and aesthetic trends can emerge and mature within months. Retailers therefore increasingly expect manufacturing partners capable of reducing development timelines through ready to customize formulations, modular packaging systems, accelerated validation protocols, and flexible sourcing models. Manufacturers unable to operate within compressed launch windows risk becoming structurally uncompetitive.

Regulatory fluency across markets. Regulatory sophistication has also become significantly more important. Retailers operating across multiple geographies face increasingly complex compliance environments involving EU cosmetics regulation, FDA requirements, sustainability claims scrutiny, ingredient restrictions, and country specific registration obligations. As a result, regulatory support is increasingly becoming part of the commercial value proposition rather than merely a technical back office function. Manufacturers capable of supporting dossier preparation, claims substantiation, ingredient documentation, and multi market launch coordination hold a meaningful competitive advantage.

Sustainability credentials that hold up to scrutiny. Sustainability has become another critical dimension of supplier selection. Retail sustainability commitments increasingly flow upstream into manufacturing requirements, forcing suppliers to demonstrate capabilities around recycled packaging, ingredient traceability, cruelty free compliance, certification standards, and carbon reduction initiatives. Retailers face growing pressure to combine sustainability with accessible price positioning, a balance that remains difficult across much of the industry. Manufacturers capable of delivering commercially viable sustainable solutions are therefore increasingly positioned as preferred strategic partners rather than interchangeable suppliers.

Capacity and reliability at scale. A missed production window for a retailer's own brand is categorically different from a missed production window for a third-party brand. If No7 is out of stock at Boots, there is no alternative supplier to fall back on — the loss is both a sale and a trust event with the retailer's most loyal customers. CDMOs that can demonstrate consistent on-time delivery, adequate safety stock management, and contingency production capacity are disproportionately valued in retailer private label programs.

Minimum order quantity flexibility. Particularly for specialty and mid-size retailers exploring private label for the first time — or for retailers launching new sub-brands or experimental categories — the ability to manufacture at low initial volumes before scaling is a meaningful barrier-reducer. Manufacturers who can offer tiered MOQs, white-label starting points, and progressive customization paths tend to win entry-level contracts that evolve into strategic relationships.

Innovation support has become increasingly important as well. Retailers no longer expect manufacturers simply to execute technical briefs. Increasingly, they expect proactive contribution around trend forecasting, ingredient scouting, packaging innovation, texture development, and benchmark analysis. This is particularly true within specialty beauty retail, where differentiation matters more than pure price positioning.

Who To Call: The Right Entry Points By Retailer Type

The organizational complexity behind retailer private label programs is often underestimated by manufacturers entering the sector. Different retailer categories tend to structure private label responsibility differently.

In drugstore and pharmacy chains (Boots, dm, Rossmann, Shoppers Drug Mart, CVS, Watsons), private label product decisions sit predominantly with a Category Management or Own Brand Director, often supported by a dedicated product development team that manages formulation briefs and supplier relationships. Regulatory and quality functions are typically separate but have significant influence over supplier approval. The commercial entry point is through category, but approval requires a parallel conversation with quality and regulatory teams.

In specialty beauty retailers (Sephora, Ulta, Douglas, Marionnaud), the function is often titled Brand Development, Own Brand, or Private Label Merchandising. These teams operate with significant brand-building ambition and frequently have their own in-house product developers or trend researchers. CDMOs approaching specialty retailers need to demonstrate genuine innovation capability — the ability to bring a formulation or concept to the table proactively, not merely respond to a brief. Ulta Beauty's VP of Private Label Merchandising has been explicit that the brand seeks partners who help it "anticipate" trends, not merely execute them.

In mass retailers and grocery (Walmart, Target, Carrefour, Tesco, Lidl, Aldi), private label is managed through a centralized Buying or Procurement function, often with a dedicated Own Brand team embedded within. Price competitiveness is weighted more heavily in these relationships, and the commercial conversation begins with the buying team. However, long-term contract security requires alignment with quality assurance functions that conduct facility audits and formulation testing independently.

In fashion-adjacent and lifestyle retailers (H&M Beauty, Zara Beauty, Primark, & Other Stories), the private label function is typically housed within a broader Product team that straddles apparel and beauty. These teams move fast, value aesthetic alignment heavily, and are often less experienced in the technical nuances of cosmetic manufacturing compliance. CDMOs that can serve as turnkey education and quality assurance partners — not merely suppliers — tend to build stickier relationships in this segment.

In practice, supplier approval usually requires alignment not only with procurement teams but also with quality assurance, sustainability, regulatory affairs, and product development functions simultaneously. Manufacturers approaching retailers exclusively through procurement channels often underestimate the broader organizational dynamics involved.

The Pain Points Contract Manufacturers Must Address

Despite the growth of retailer owned beauty brands, retailers themselves continue to face significant operational and strategic challenges.

Speed to market is the most frequently cited frustration. Traditional development timelines often remain poorly aligned with modern beauty trend cycles, particularly in categories heavily influenced by social media. Retailers increasingly need manufacturers capable of compressing development cycles without compromising formulation stability or regulatory compliance.

Formulation consistency across geographies. Maintaining consistency across multiple manufacturing partners also creates complexity, especially for retailers operating internationally. Variations in texture, fragrance, ingredient sourcing, or packaging quality can quickly erode consumer trust in retailer brands. Consumers increasingly expect retailer owned products to deliver consistency levels comparable to multinational beauty groups.

Clean and transparent ingredient sourcing. Clean beauty expectations have further increased documentation burdens. Retailers increasingly require detailed transparency around ingredient sourcing, extraction methods, allergen status, toxicological safety, sustainability claims, and cruelty free compliance. Many smaller manufacturers struggle to maintain documentation systems at the level now expected by large retailers.

Packaging innovation at accessible price points. Consumers increasingly evaluate beauty products partly on the basis of packaging sustainability: refillable formats, PCR content, mono-material construction, and reduced plastic use. Retailers want to offer these features in their private label ranges to meet their own ESG commitments and respond to consumer preference. The challenge is that sustainable packaging almost always carries a cost premium that compresses the price differential that makes private label attractive to consumers. CDMOs that have invested in sustainable packaging partnerships and can offer credible eco-alternatives without punitive cost premiums are solving a real problem.

Regulatory support for multi-market launches. A retailer launching a new private label skincare range across Europe, the UK, and the Middle East simultaneously faces a documentation and registration burden that its internal teams are often not resourced to manage. CDMOs that offer regulatory affairs support as part of their service proposition — dossier preparation, safety assessment coordination, claims substantiation — are providing genuine value beyond the product itself, and this support is becoming a more explicit part of the supplier evaluation conversation.

Brand coherence support. As retailer private label programs mature from functional ranges into genuine brands, the demand on suppliers shifts. Retailers need CDMOs who can maintain a coherent sensory signature — fragrance, texture, color, packaging aesthetic — across a growing SKU count and multiple production batches. This requires more than quality control; it requires a manufacturing partner who understands brand positioning well enough to serve as a guardian of brand consistency, not merely a producer to specification.

Retailers Also Face Strategic Risks

The expansion of retailer owned beauty brands is not risk free.

By operating increasingly as brand owners, retailers assume responsibilities historically carried by multinational beauty groups, including inventory exposure, regulatory liability, recall risk, sustainability scrutiny, and direct reputational accountability. A failed retailer brand affects not only product sales but potentially the retailer’s broader credibility with consumers.

At the same time, relationships between retailers and multinational suppliers are becoming simultaneously more collaborative and more competitive. The same retailer that depends on multinational brands to drive traffic and category credibility may also increasingly prioritize shelf placement, marketing visibility, and loyalty program support for its own products.

The result is not the disappearance of national brands but rather a more complex and interconnected competitive landscape in which retailers themselves increasingly participate as brand owners.

Looking Ahead

The expansion of retailer owned beauty and wellness products should not be viewed as a temporary inflation driven phenomenon. The underlying drivers are structural and likely long lasting.

Retailers increasingly recognize that owned brands provide stronger margins, deeper customer retention, greater exclusivity, and more control over pricing architecture. Consumers, meanwhile, have become materially more willing to trust retailer owned products, particularly in categories where efficacy, ingredients, and value increasingly outweigh heritage positioning alone.

For contract manufacturers and CDMOs, this creates a substantial long term opportunity, although one that increasingly favors organizations capable of acting as strategic partners rather than commodity suppliers. Retailers are no longer looking solely for manufacturing capacity. Increasingly, they are seeking partners capable of supporting innovation, regulatory complexity, sustainability objectives, packaging development, trend responsiveness, and long term brand consistency.

The beauty retailer of the future will likely continue to operate simultaneously as distributor, curator, data platform, and brand owner. That convergence is already reshaping the structure of the global beauty industry and redefining the relationships between retailers, manufacturers, and the brands that once viewed retailers primarily as channels rather than competitors.

Beauty and Wellness Private Labels List

CHF 0.00

This is a list of retailers and their beauty private labels