From Appearance to Affect: The Neuro-Emotional Pivot in Prestige Beauty

Executive Summary

The most significant shift in global beauty and wellness right now is in the definition of product efficacy. Aesthetic correction is no longer the whole pitch. Neurological and emotional regulation now carries equal weight. CARRARA Advisory has tracked a clear move among high margin consumers who no longer treat skincare as a purely topical category, but as a lever in their broader biological stress management. The skin brain axis has moved out of academic journals and into commercial roadmaps across the prestige and ultra prestige tiers.

Success in this pivot depends on validated biometric data and proprietary neuro active formulation, not vague wellness language. As the FDA and EU regulators sharpen scrutiny of neurological claims, brands that can show clinical evidence of cortisol reduction or neurotransmitter modulation will separate from those running purely sensory marketing. We expect neuro scientific validation to become table stakes for prestige launches within five fiscal years. This report sets out the underlying biology, the market data, and the strategic calls for operators and investors, including two developments we consider under covered by the market to date: the consolidation of neuro beauty into a five modality product architecture, and a step change in consumer search behavior first visible in August 2025.

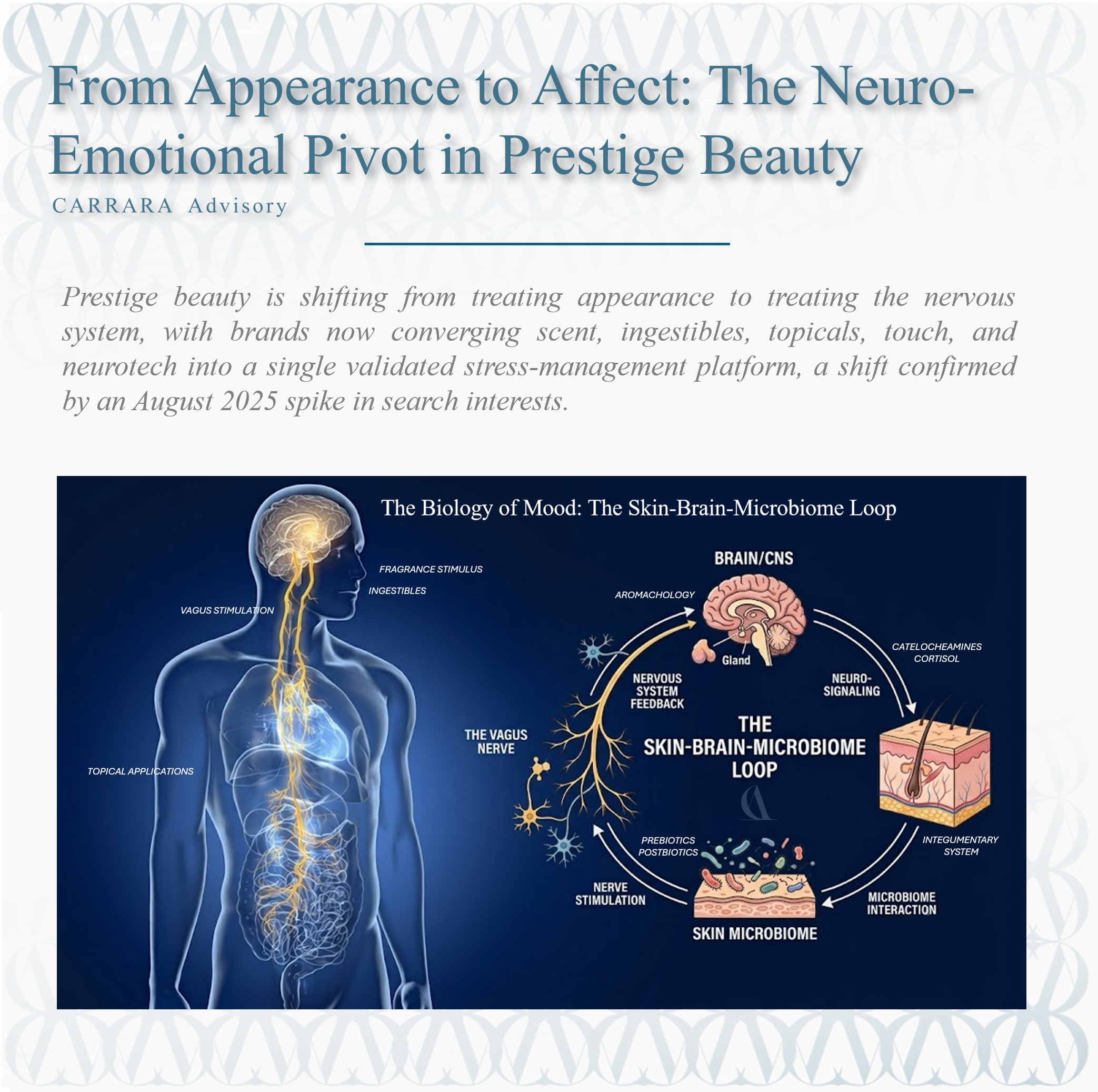

The Biology of Mood: The Skin Brain Microbiome Loop

The bidirectional communication between the central nervous system and the skin, including its associated glands, hair follicles, and other structures of the integumentary system, is the biological foundation of this pivot. This relationship, the skin brain axis, runs on neuropeptides and neurotransmitters produced by both the brain and skin cells themselves. Skin acts as an active neuroendocrine organ, producing cortisol and catecholamines in response to environmental and psychological stress, well beyond its role as a simple barrier.

Shiseido's aromachology research, the study of how scent influences emotion, has reported barrier recovery benefits from certain fragrances, and the broader mechanism is well established. HPA (Hypothalamic-Pituitary-Adrenal) axis activation under stress releases cortisol, which degrades the skin barrier and raises inflammation. Brands are increasingly building products to interrupt that pathway rather than just treat the redness or dryness that results from it.

The microbiome is the third leg of the loop. Skin surface microorganisms produce metabolites that communicate with the nervous system and appear to influence both mood and skin condition. That is why prebiotics and postbiotics are increasingly marketed as calming the skin's nervous response rather than simply supporting barrier function. McKinsey's 2024 UK wellness research found that 73% of surveyed consumers rank wellness as a top or important priority, directional evidence for a market that increasingly links appearance and mindfulness as a single consumer concern.

Early research also points to the vagus nerve as a fourth mechanism. Specific massage and application techniques appear to stimulate vagal tone and reduce systemic inflammation, which is why some brands are now patenting application rituals alongside the formulas themselves. The ritual of applying the product is becoming part of the claim, alongside the formula.

Neuro Actives and the Regulation of Inflammation Pathways

Neuro cosmetics use ingredients designed to interact with the cutaneous nervous system rather than target collagen synthesis or melanin production directly. Sisley Paris's Neurae, which launched in early April 2024, is the clearest commercial marker of this category to date. The brand is built entirely on NA3 Technology, combining neuro ingredients, targeted fragrance, and texture design to counter the physical signs of tiredness, sadness, and agitation.

Mechanistically, this category is working two levers: inhibiting Substance P, a neuropeptide tied to pain and inflammation, and stimulating beta endorphins. Ingredients such as red algae and specific botanical extracts are marketed on their ability to modulate the TRPV1 receptor, the same receptor involved in heat and pain perception, to lower the skin's sensitivity threshold and reduce the inflammatory load associated with chronic stress.

Innova Market Insights has tracked a sharp rise in neuro related claims in personal care launches since 2020, and we treat cortisol skincare as a distinct, investable sub segment addressing inflammaging, the chronic low grade inflammation that accelerates visible aging. The commercial target is the urban consumer under sustained environmental and psychological load, and pricing power in this segment is already meaningfully above standard prestige skincare.

Emotional Segmentation: Stress State as the New Skin Type

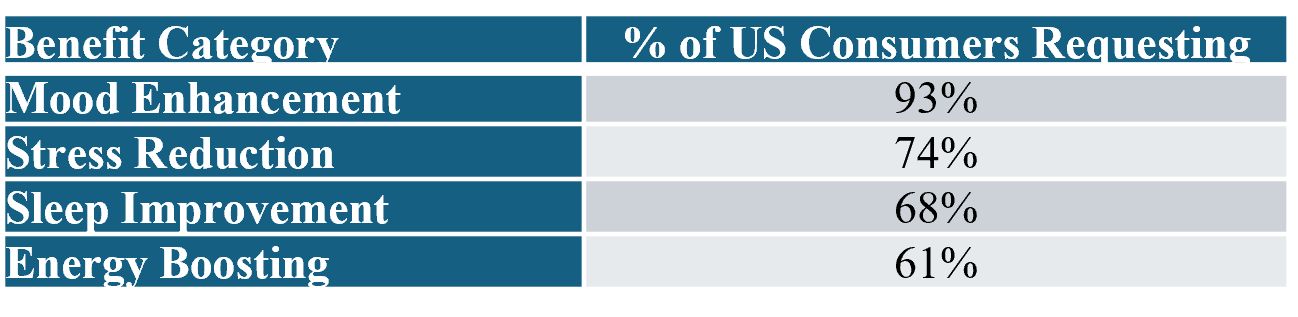

Exhibit 1: Consumer Demand for Functional Benefits in Body Care (2023, US)

Source: Givaudan Active Beauty Research 2023.

Skin type used to mean oily, dry, or combination. CARRARA Advisory sees the industry moving toward emotional segmentation instead, where the consumer's current psychological state, rather than their underlying skin type, determines product choice. Givaudan Active Beauty's research found that 93% of US body care users want formulations with mood enhancing benefits, alongside strong demand for sleep, stress, and energy claims (Exhibit 1).

High income households are the primary driver. Circana data shows these households now cite sensory experience and mood elevation ahead of price or celebrity endorsement as purchase drivers. Marketing is following the shift: before and after wrinkle photography is giving way to biometric visualization, including thermal imaging showing reduced skin temperature, an inflammation marker, or EEG readouts showing increased alpha wave activity, a relaxation marker, after product use.

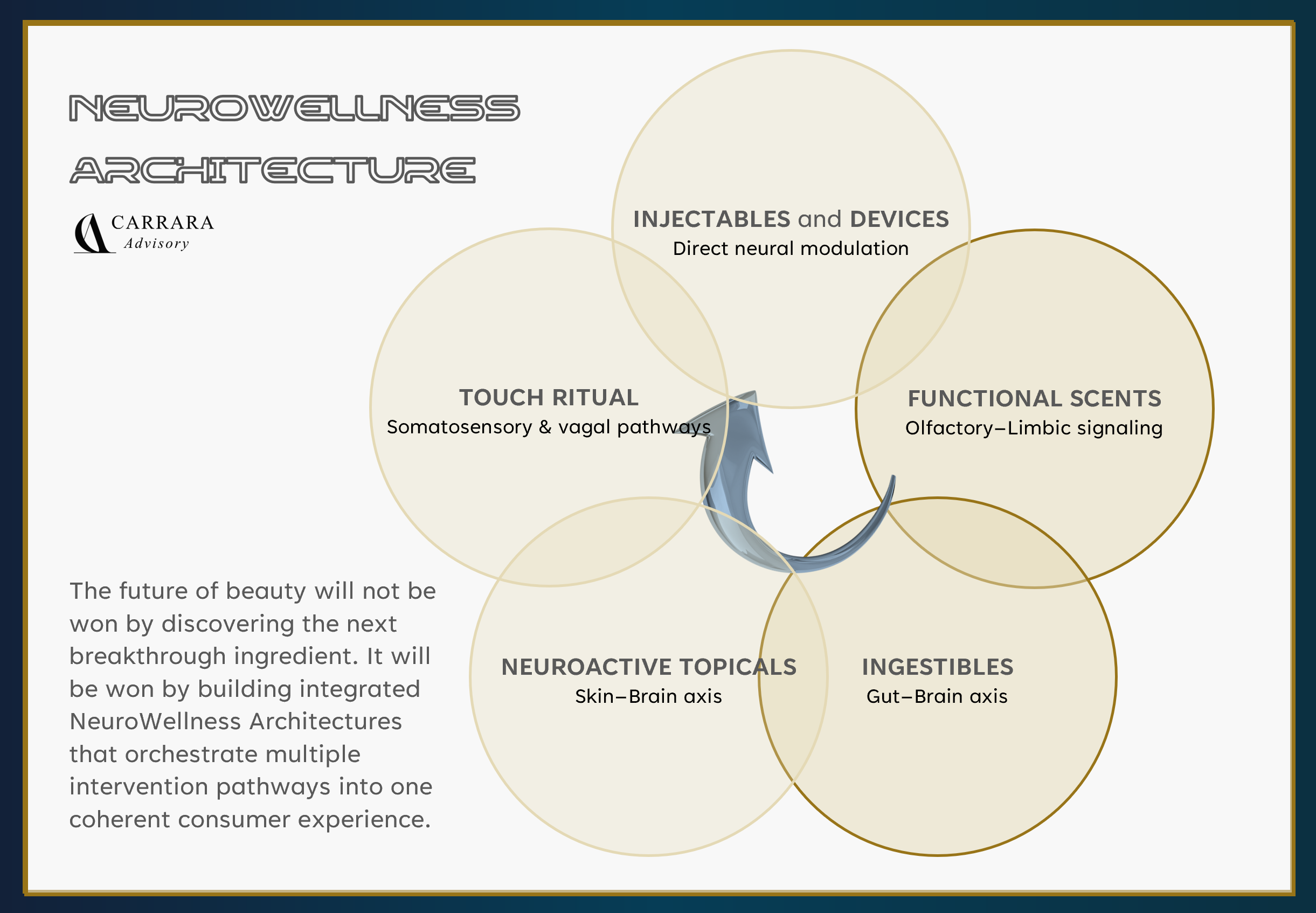

From Ingredient to Architecture: The Five Modality Stack

The most investable signal in this space is the consolidation of five previously separate modalities into one delivery architecture, rather than any single neuro ingredient: functional scent (aromachology), ingestibles (pre, pro, and postbiotics, collagen, and adaptogenic stacks), topicals engineered around neuro actives, ritualized touch (vagus targeted massage and application protocols), and, at the top of the pyramid, injectables and neuromodulation devices. A single standout ingredient no longer defines competitive advantage. Owning multiple nodes across this stack does.

This mirrors the CDMO to platform consolidation already under way elsewhere in beauty. Whoever owns two or more nodes in this loop controls the customer relationship and the repeat purchase logic, not merely a single SKU. Sisley's Neurae already combines topical, textural, and olfactory modalities under one technology umbrella. DSM Firmenich's emotiOn program supplies the fragrance layer to multiple beauty houses independently of any one brand. The growing consumer neurotech category, at home vagus stimulation and neuromodulation devices, is starting to sit alongside these on retail shelves and in spa protocols, rather than in a separate wellness aisle.

For operators, this reframes the M&A target list. A neuro active skincare line without an ingestible or a scent companion is one point of a system someone else is trying to complete, and should be priced and negotiated accordingly. For investors, the relevant multiple should reflect stack ownership and cross modality IP, not ingredient novelty alone.

The Wellness Hospitality Link: Integrating Neurocosmetics into the Guest Journey

Luxury hospitality is the most sophisticated proving ground for this category. Groups such as Raffles and Six Senses are integrating neuro cosmetics into the guest journey beyond the spa treatment room and into in room neuro regulation, using functional fragrance and neuro active skincare to help guests with circadian alignment. A guest who reports a meaningful improvement in sleep quality or perceived stress during a stay is a materially better prospect for the associated retail line.

Some properties are now selecting in room amenities against a pre arrival mood assessment: energy focused neuro cosmetics for a guest traveling on business, serenity focused products for a guest traveling to unwind. This also gives brands a controlled setting to collect performance data under real world stress conditions, such as travel, jet lag, and time zone disruption, conditions that are hard to replicate in a lab.

Functional Fragrance: The Quantification of Affect

Fragrance is the most scientifically advanced sub sector in translating emotional claims into evidence. The 2023 DSM Firmenich merger accelerated this. The combined entity's emotiOn platform uses neuroscience to validate how specific scent molecules trigger emotional responses, letting prestige houses sell mood claims backed by EEG and heart rate variability data rather than adjectives. The program's most current proof point, emotiOn Social Connection, launched in September 2025 and was built on a database of more than 40,000 tested fragrances and a 20 country, 12,000 consumer study, aimed specifically at social confidence and connection rather than general relaxation.

Consumer search behavior backs this up. Spate data shows searches for mood boosting perfume rose sharply in 2023, and L'Oreal's Scent Sation technology, shown at VivaTech 2024, uses an EEG headset to record a consumer's emotional response to different scents and personalize fragrance selection on that basis rather than on stated preference.

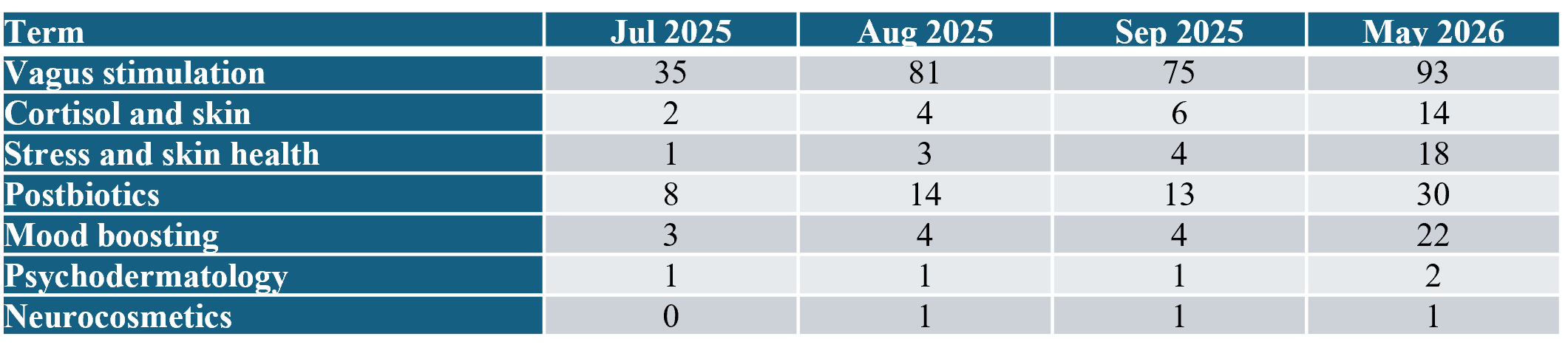

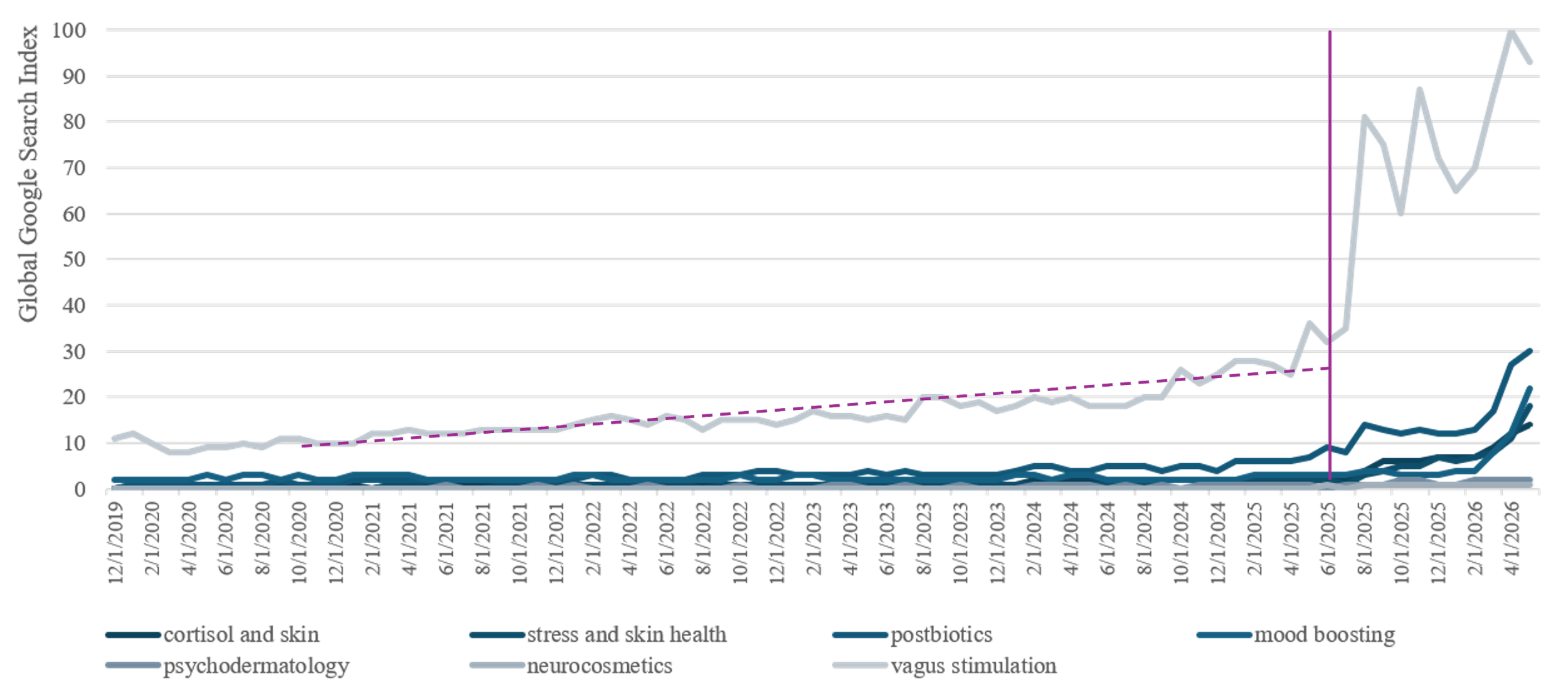

What the Search Data Shows: The August 2025 Inflection

Exhibit 2: Search Interest Index, Selected Months (Google Trends, 100 = peak in series)

Source: Google Trends data supplied by client, 12/2019 to 5/2026.

We did investigate global Google Trends indices for seven terms spanning the stress skin and neurowellness space. Two things stand out. First, six of the seven terms show a visible step change starting in August 2025 rather than a gradual ramp. Index values roughly double month over month for several terms rather than drifting up. Second, the terms did not move together. Vagus stimulation moved first and hardest, the skin and stress terms followed with roughly a one month lag, and the beauty industry's own coined terms, neurocosmetics and psychodermatology, barely moved at all.

The timing lines up with three concrete, dateable events rather than a diffuse cultural drift. An August 2025 randomized controlled trial in Applied Sciences and a separate 2025 study in Frontiers in Human Neuroscience gave vagus nerve stimulation its first consumer scale peer reviewed backing. In roughly the same window, Flow received FDA approval for an at home neuromodulation device, and consumer devices such as Pulsetto and Elemind moved from crowdfunding visibility into retail. That is the point at which vagus nerve stops being an influencer phrase and becomes a purchasable category. The cortisol face narrative, meanwhile, had already been circulating on TikTok since mid 2024 and spent most of 2025 in a mainstream media debunking cycle. Healthline, Healthgrades, and BodySpec all ran explainer pieces between February and October 2025, coverage that, even while correcting the claim, keeps pulling search volume toward cortisol and skin terms.

We read this as three layers of the same funnel rather than three unrelated spikes. Vagus and cortisol terms are the entry point: relatable, social media native, symptom first. Postbiotics and mood boosting sit in the middle, a more legitimizing, protocol driven layer. Neurocosmetics and psychodermatology are the industry's own vocabulary for the purchasable end point of that funnel. The fact that they remain essentially flat throughout the series, even as the underlying consumer interest triples and quadruples, is itself a finding. The market is searching for the symptom and the mechanism well ahead of adopting the industry's branding for it. That looks like a naming and positioning gap rather than a demand gap, and it keeps closing. Every term in the series accelerates again into March through May 2026, roughly coinciding with the Global Wellness Summit naming neurowellness one of its defining trends for the year.

This directly supports the platform argument above. The August 2025 inflection was led by a device and a clinical result, not a skincare launch, which is further evidence that the winning commercial architecture spans modalities rather than sitting inside skincare alone.

Strategic Risk: Avoiding Neuro Washing Through Validated Biometric Testing

As the commercial upside becomes obvious, so does the risk of neuro washing: unsubstantiated claims that a product influences the nervous system or mood. High margin consumers are already more skeptical of these claims than they are of conventional efficacy claims, and both the FDA and EU regulators are increasing scrutiny of neurological language in cosmetics. A product that claims to alter mood or reduce stress too explicitly risks reclassification as a drug, which changes the R&D cost base, the trial requirements, and the tax and distribution profile entirely.

Market leaders are managing this risk with biometric testing rather than adjectives:

EEG: measuring brain wave response to scent and texture to confirm the experience matches the marketing claim.

Cortisol testing: saliva or skin swab measurement of stress hormone reduction after product use.

Heart rate variability (HRV): assessing autonomic nervous system impact, specifically sympathetic and parasympathetic balance.

fMRI: rare and high cost, used to map reward center activation in response to product use.

Shiseido's Feel technology, which measures how skincare texture influences emotional state, is the clearest example of turning a subjective sense of pleasure into an objective, defensible claim. Brands without this level of proof will be at a growing disadvantage as consumers start asking the same questions of mood claims that they already ask of anti aging claims.

The Paradox of Longevity: Affect as a Biological KPI

The neuro emotional pivot is a sub sector of the broader longevity movement, and we think C suites should treat affect as a biological KPI rather than a marketing layer. Chronic psychological stress is one of the strongest known accelerants of cellular aging. Telomere shortening is directly linked to sustained high cortisol, so a product that measurably reduces the skin's stress response is, by that logic, a longevity product. This is pulling beauty, mental health, and biohacking into the same commercial conversation.

WGSN has flagged psychodermatology, where dermatologists and psychologists co-develop products, as a primary growth driver through 2025. These products target the emotional root of flares such as acne, rosacea, or eczema, which are frequently made worse by the nervous system, rather than treating the visible flare alone.

Strategic Implications for Operators and Investors

Moving from appearance to affect requires restructuring R&D and go to market, not just messaging. For operators, that likely means partnering with or acquiring biotech and biometric data specialists. The L'Oreal neuro tech acquisitions and the DSM Firmenich merger are the templates for the consolidation we expect to continue.

For investors, the differentiator is IP in the neuro active space, not story. A brand that can show a 15% reduction in salivary cortisol after 28 days of use is a materially better underwrite than one relying on calming imagery in social content. Retail also has to change. The department store counter is a poor format for selling emotional regulation, and we expect more sensory controlled retail, with lighting, sound, and scent tuned to demonstrate efficacy in real time, in the vein of L'Oreal's Scent Sation headset.

Supply chain is a real constraint. Neuro active botanical extracts need a higher level of traceability and potency testing than standard actives, and climate driven volatility in natural supply is already pushing the category toward precision fermentation for stable, scalable sourcing.

Strategic Considerations for the C Suite

Five mandates for leadership through the end of the 2020s:

Reallocate R&D toward neuro efficacy. Wrinkle depth and hydration metrics no longer justify ultra prestige pricing on their own. Neurae shows the market is ready for a dedicated neuro brand.

Evolve consumer insights past the focus group. Surveys are poor at capturing subconscious response. Adopt eye tracking, facial coding, and EEG to inform packaging, texture, and scent decisions directly.

Manage regulatory risk proactively. Bring legal into the creative process early. Promoting relaxation is a cosmetic claim. Reducing clinical anxiety is a drug claim, and the gap between them is where launches get expensive.

Move retail toward experiential bio hacking. Wellness lounges, offering meditation, light therapy, and in store trial, convert better than a counter demo for this category.

Build the brand narrative around longevity, not trend cycles. It is a more durable position and a better hedge against the usual beauty trend churn.

Closing

The neuro emotional pivot is a continuation of the Clean and Clinical movements rather than a break from them: a more precise understanding of the body applied to the same commercial problem. The August 2025 search inflection, and the device and clinical trial events behind it, are the clearest evidence yet that this has moved from thesis to measurable market behavior. Brands and investors that treat the skin brain axis as an operating model, not a marketing layer, will set the terms of competition in this category over the next decade.

Sources

McKinsey & Company. (2024-01-16). The trends defining the global wellness market in 2024. https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/the-trends-defining-the-global-wellness-market-in-2024

Shiseido Annual Report 2023.

Givaudan Active Beauty Research 2023.

Circana Luxury Beauty Trends 2024.

Spate Beauty Trends 2023.

L'Oreal Financial Report Fiscal Year 2023.

dsm-firmenich, emotiOn Social Connection launch, September 2, 2025.

Global Wellness Summit, The Rise of Neurowellness, Future of Wellness 2026 Trend Report.

Google Trends, client-supplied search index data, December 2019 to May 2026.

Fashionista, Wallpaper, Stylus, and LSN coverage of Sisley's Neurae launch, March to April 2024.