The Currency Effect: A Hidden Two-Point Headwind

One of the most underappreciated features of 2025 beauty industry results is how much of the reported growth slowdown was driven not by underlying business performance but by currency impact. Taking the companies where the gap between reported and organic (constant-currency) growth is directly disclosed or reasonably estimable: L'Oreal saw a currency drag of approximately 2.7 percentage points on its USD-reported results, with the company's own disclosures confirming a 3.6% negative FX impact at the euro level. Beiersdorf absorbed roughly 2.4 percentage points of FX headwind, with organic growth of +2.4% comparing starkly to its flat reported result. Coty faced a drag of roughly 2.5 to 3 points, a figure management flagged as a material headwind throughout the year as the dollar strengthened. Puig, also a euro reporter, lost approximately 2.5 points to currency translation. Amore Pacific saw a modest headwind from a weaker Korean won. On the other side of the ledger, Shiseido and Estee Lauder, whose results are already measured in USD or translated from a relatively weak yen, received a modest positive tailwind from currency, partially masking the severity of their underlying business declines.

When we apply these adjustments across all ten companies and weight them by revenue, the picture changes substantially. The aggregate reported growth of +0.5% for the group translates to approximately +2.3% on an organic, constant-currency basis. That means FX effects subtracted roughly two full percentage points from the headline result. Put differently, almost the entire gap between 2025's reported +0.5% and 2024's +4.9% is explained by two factors in roughly equal measure: genuine business deceleration and adverse foreign exchange translation. The beauty industry in 2025 was considerably less weak in operational terms than the dollar-denominated headlines suggest.

This currency headwind also has an important directional asymmetry for 2026 planning. The companies most penalized by FX in 2025, primarily L'Oreal, Beiersdorf, Puig, and Coty, are the most euro-denominated businesses. If the dollar were to soften relative to the euro, these companies would receive a mechanical tailwind in their reported USD figures even with no change in underlying commercial performance. Conversely, any further dollar strengthening would represent an additional headwind. Currency, in short, is not a footnote to the beauty industry's 2025 story; it is a co-author.

Scale as a Liability: The Eight-Point Gap Between Large and Small

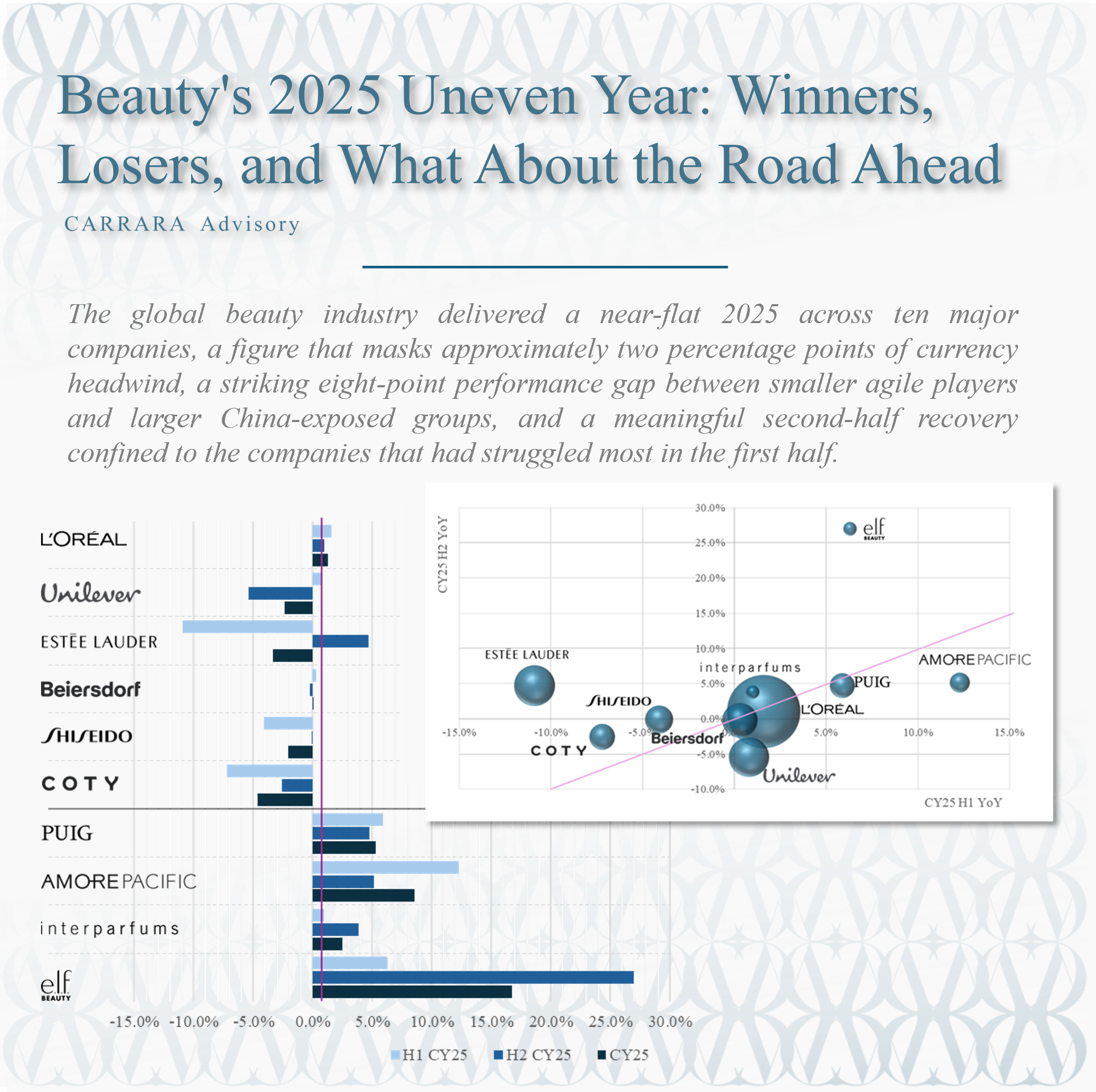

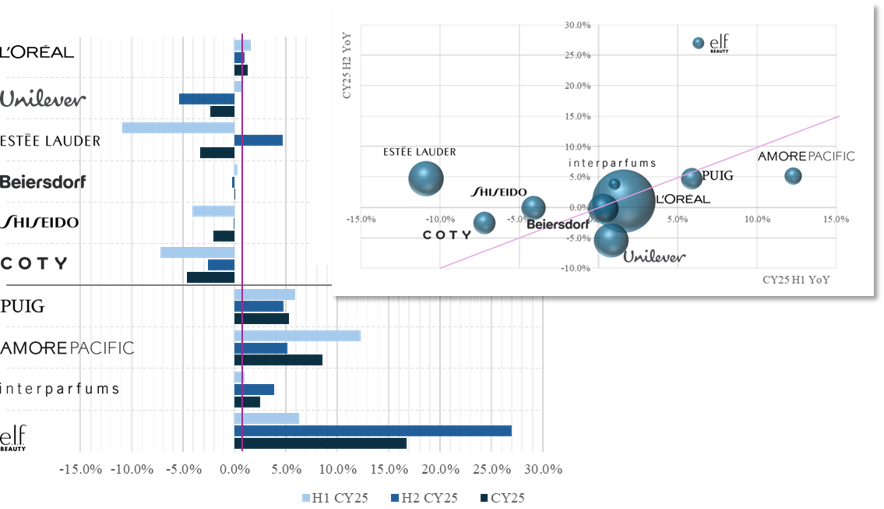

A second structural pattern in the data deserves explicit attention: the consistent and sizable outperformance of the four smallest companies relative to the six largest. Sorting the ten companies by annual revenue, the top six (L'Oreal, Estee Lauder, Unilever, Beiersdorf, Shiseido, and Coty) posted a weighted average revenue decline of -0.6% in 2025. The bottom four (Puig, Amore Pacific, Interparfums, and E.L.F. Beauty) delivered a weighted average growth of +7.3%. That is a gap of nearly eight percentage points between the large-cap and small-cap beauty tiers in this sample.

The reasons are structural rather than coincidental. The largest companies carry the heaviest exposure to the two headwinds that most defined 2025: China and travel retail. Estee Lauder, Shiseido, Coty, and to a lesser extent L'Oreal and Beiersdorf all built substantial revenue bases in China's prestige skin care market and Asia duty-free channels during the boom years. When those channels contracted sharply, the losses were concentrated in the companies large enough to have meaningful positions there. The smaller companies, by contrast, had either not yet built that exposure or had deliberately focused on faster-growing channels and geographies: Western fragrance markets for Puig and Interparfums, K-Beauty's global wave for Amore Pacific, and trend-responsive value innovation in the U.S. for E.L.F.

There is also an agility argument. Smaller organizations can pivot assortment, redirect marketing investment, and respond to emerging trends faster than those managing dozens of brands across scores of markets. E.L.F. Beauty's acceleration from +6.3% in H1 to +27.0% in H2 would be mechanically impossible at L'Oreal's scale. Amore Pacific's double-digit first-half expansion reflected a brand story that focused organizations can amplify more quickly than legacy multinationals. The 2025 data suggests that in a challenging and rapidly shifting environment, focus and agility were rewarded while scale became a liability.

H1 to H2: Five Stories of Recovery, Five of Deceleration

A common narrative about 2025 beauty results is that the industry improved as the year progressed. That is broadly true at the aggregate level, where the group's weighted growth moved from -0.7% in H1 to +1.9% in H2. But the individual company trajectories are considerably more varied.

Five companies genuinely improved from H1 to H2. Estee Lauder recorded the most dramatic swing, moving from -10.9% to +4.7%, a reversal of more than 15 percentage points that reflects both easier prior-year comparisons and real commercial recovery, particularly in the U.S. Coty improved from -7.2% to -2.6%, still negative but directionally meaningful. Shiseido moved from -4.1% to -0.1%, essentially returning to flat. Interparfums accelerated from +1.0% to +3.8% as a strong European Q4 offset ongoing U.S. softness. And E.L.F. Beauty posted the most spectacular second-half result of any company in the group, surging from +6.3% to +27.0%.

The other five companies saw their growth rates decelerate from H1 to H2. L'Oreal slipped modestly from +1.6% to +1.0%, a small move largely explained by a demanding comparison base from a strong Q4 2024. Beiersdorf edged from +0.3% to -0.2%, also marginal. Puig decelerated from a strong +5.9% to +4.7%, reflecting some normalization after an exceptional early-year. Amore Pacific slowed more sharply from +12.3% to +5.2%, partly a consequence of very strong H1 2024 comparisons. And Unilever experienced by far the steepest H2 deterioration in the group, falling from +0.8% to -5.4%, heavily influenced by portfolio restructuring, the separation of its Ice Cream division, and pressures in personal care.

The pattern that emerges is not one of universal improvement. For companies that began 2025 in genuine crisis, Estee Lauder, Coty, and Shiseido, the second half represented a real turning point. For companies that started with momentum, tougher comparisons and broader market deceleration created a natural headwind. And for Unilever and Amore Pacific, structural and portfolio-specific factors created their own trajectories, independent of any simple cyclical narrative.

L'Oreal: The Benchmark Holds, But Barely

As the world's largest beauty company with nearly $47.7 billion in revenues, L'Oreal occupies a category all its own. Its +1.3% reported growth in 2025 may look unimpressive on the surface, but when viewed through a like-for-like lens, excluding the negative impact of currency fluctuations, growth was a much stronger +4.0%. Currency headwinds cost the company roughly 3.6 percentage points of reported growth, a reminder that dollar-denominated results tell only part of the story for this deeply international group.

L'Oreal's 2025 story was one of resilience built on portfolio breadth. The Professional Products division achieved an important milestone, recording over five billion euros in annual revenue for the first time in its history, driven by strength across premium haircare and a deliberate push into both e-commerce and selective distribution channels. The Dermatological Beauty division, home to brands like Eucerin, CeraVe, and SkinCeuticals, continued to advance ahead of the broader skin care market. Digital commerce became a meaningful part of the revenue mix, eclipsing 30% of total group sales. The Luxe division, which houses globally recognized fragrance lines under Yves Saint Laurent, Valentino, and Prada, saw its momentum build progressively through the year, finishing with double-digit growth in the fourth quarter as consumer confidence in China's luxury market began to return.

On the strategic front, L'Oreal committed to two of its most significant moves in years. The acquisition of Kering Beaute's brand portfolio broadens its position in ultra-premium beauty, while increasing its ownership stake in Galderma opens a pathway into the fast-expanding medical aesthetics adjacency. The group maintained its longstanding pattern of growing faster than the broader beauty market in 2025. CEO Nicolas Hieronimus conveyed a constructive tone on the outlook, pointing to improving market conditions and an accelerating innovation pipeline as reasons for confidence heading into 2026.

Estee Lauder: A Company in Painful Transition

If L'Oreal's story in 2025 was one of managed resilience, Estee Lauder's was one of managed crisis. Revenues fell -3.3% for the calendar year, driven by an exceptionally painful first half in which sales declined nearly -11%. The full fiscal year ending June 2025 saw revenues drop approximately 8%, making it the third consecutive year of organic sales declines for the company.

The causes are well understood. Estee Lauder spent years building a disproportionate reliance on Asia travel retail and China's prestige skin care market during the period when both channels were among the fastest-growing in global beauty. The sharp reversal in both, as Chinese consumer sentiment contracted and cross-border travel normalized at lower volumes than expected, hit Estee Lauder harder than almost any other major company. Skin care, its dominant revenue category, bore the brunt, with key franchises from the flagship Estee Lauder brand and La Mer posting steep declines.

The second half of calendar 2025 showed early evidence that the worst may be behind the company. Revenue grew by +4.7% in that period, driven by improving performance in the U.S. market where several key brands including Clinique and The Ordinary regained shelf momentum. The fragrance portfolio, led by Le Labo and Jo Malone London, held its footing throughout. Under new CEO Stephane de La Faverie, the company has been executing a sweeping restructuring program called Beauty Reimagined, which has involved thousands of job reductions and the impairment of assets across several brands including TOM FORD and Too Faced. The road back to consistent growth runs through 2026 and into 2027.

Unilever: Beauty Bright Spot in a Complicated Portfolio

Unilever's aggregate beauty-related revenues of approximately $13.9 billion in calendar year 2025 showed a -2.3% decline, a figure heavily influenced by the company's ongoing portfolio transformation and the separation of its Ice Cream business. Stripping out the impact of currency, net disposals, and structural changes, the underlying picture was more constructive: Unilever's Beauty and Wellbeing segment generated approximately 12.8 billion euros in turnover in 2025 with underlying sales growth of around 3.5% for the full group, with momentum improving as the year progressed and a particularly strong fourth-quarter performance.

Under CEO Fernando Fernandez, who assumed leadership in 2025, Unilever has made beauty, wellbeing, and personal care the explicit engine of its growth agenda, targeting premium positioning and digital commerce as the primary levers. Several of its newer or recently acquired brands, including K18, Nutrafol, Hourglass, and Liquid I.V., delivered double-digit growth. Dove continued its role as a steady anchor across markets. Gross margin expanded significantly, reaching nearly 47%, as the product mix shifted toward higher-value categories. The company's underlying sales performance, while below 2024 levels, still compared favorably to most of the other large players tracked here. The direction of travel under Fernandez is clear: Unilever is deliberately reshaping itself into a more focused beauty and wellness business, with less of its identity tied to commodity household products.

Beiersdorf: Derma Carries, Nivea Rebuilds

Beiersdorf closed 2025 with group sales of approximately 9.9 billion euros and organic growth of +2.4%, flat in reported terms at approximately $10.7 billion after adverse currency effects. The result was labeled solid by management, but it represented a significant step-down from the company's exceptional 2024 performance when organic growth exceeded 6.5%.

The internal divergence within Beiersdorf's portfolio was striking. The Derma business, home to Eucerin and Aquaphor, recorded its fifth consecutive year of double-digit organic growth, advancing by close to 12% for the full year. The Eucerin franchise's epigenetic serum, launched using the proprietary Epicelline ingredient, remained a standout performer well into its second year, driving outsized results in North America where Eucerin Face more than doubled in key quarters.

NIVEA, by contrast, advanced less than 1% organically for the full year. The brand faced a challenging environment on several fronts simultaneously: a structural reset of its China business, decelerating mass skin care markets in several emerging economies, and a portfolio that had grown skewed toward face care at the expense of other categories. Beiersdorf's response centered on a new epigenetics-based serum for the NIVEA franchise, introducing the same Epicelline ingredient that had powered Eucerin's success into the mass market for the first time. The September 2025 launch prompted a meaningful uptick in NIVEA's sales trajectory that month and established a platform for improved performance in 2026. CEO Vincent Warnery described 2025 as a demanding year for the skin care industry overall, while noting that Beiersdorf consistently outpaced the broader market.

Shiseido: Turnaround in Progress

Japan's largest beauty company posted a -2.1% revenue decline in 2025, generating approximately $6.8 billion in revenues. As with many peers, the challenge was concentrated in the first half, where revenues fell -4.1%, while the second half was essentially flat at -0.1%.

Shiseido has been executing a structural overhaul for several years, having reduced its global workforce by roughly one-quarter over five years while divesting non-core brands. The ongoing drag from Drunk Elephant in North America, where sales fell roughly 10% for the region overall, continued to weigh. However, the company's namesake prestige brand and Cle de Peau Beaute performed well in Japan, Asia-Pacific, and travel retail. Shiseido also revised down its estimated tariff impact to $20 million, suggesting some macroeconomic pressures eased versus initial fears. Management has guided toward a 7% profit margin return by 2026 under its Action Plan 2025-2026.

Coty: Fragrance Strength Cannot Fully Offset Structural Weakness

Coty closed its fiscal year 2025 with revenues down approximately -4.6% in calendar year terms, generating roughly $5.8 billion in sales. The company's two-speed portfolio was on full display: Prestige fragrance showed remarkable resilience, with ultra-premium fragrance growing +9% on a like-for-like basis and overall prestige declining just -1%. Consumer Beauty, which includes mass-market color cosmetics and body care, fell -8%, dragged down by weakness in the U.S. and in Asia-Pacific.

The result underscored both Coty's strengths and its structural challenges. Across all fragrance price points, the category remained a genuine growth engine, with Burberry and Hugo Boss both performing well. CEO Sue Nabi articulated a consumer trend she has called 'treatonomics': the phenomenon of consumers choosing small, mood-lifting indulgences even as they cut back on larger discretionary purchases. Fragrance, particularly in the accessible luxury tier, fits that pattern well. But mass color cosmetics continued to surrender ground to value-oriented challengers and private label alternatives, prompting the company to take a $212.8 million write-down on its Consumer Beauty color portfolio. In response, Coty refreshed its U.S. commercial leadership and pivoted toward fragrance mist extensions as a higher-margin, accessible product category that bridges its two business segments.

The Outperformers: Puig, Amore Pacific, E.L.F. Beauty

Against a backdrop of broadly flat or declining revenues among the largest players, three companies stood out as clear outperformers in 2025.

Puig, the Barcelona-based group behind Carolina Herrera, Rabanne, Charlotte Tilbury, and Uriage, delivered +5.3% reported growth to approximately $5.5 billion in revenues, achieving record full-year sales and a 12% increase in net profit. At constant currency the growth rate was considerably stronger at roughly +7.8%, ahead of the premium beauty market overall. Fragrance continued to anchor the group's performance, with its major houses all ranking among the global top ten in their respective tiers. Charlotte Tilbury extended its dominance in U.K. prestige makeup and climbed to third place in the U.S. category, a meaningful milestone for a brand that only a few years ago was primarily a British phenomenon. Makeup as a category was a genuine rebound story for Puig in 2025, growing over 10% and reversing a softer prior period. Geographically, Asia-Pacific was the fastest-growing region in the first half, and the Americas generated double-digit constant-currency growth across the full year, reflecting deliberate investment in distribution and marketing that peers found harder to execute.

Amore Pacific, the South Korean beauty giant, posted +8.5% growth to approximately $3.4 billion in revenues, building on a +5.9% result in 2024. The company's international expansion, fueled by the global K-Beauty wave and the resonance of brands like Sulwhasoo, Laneige, and its namesake Amorepacific label, continued to drive meaningful outperformance. The international K-Beauty boom, amplified by TikTok discovery and deep product innovation, has created a structural tailwind for Amore Pacific that appears likely to persist. The company's collaboration with Sephora on a multi-brand K-Beauty pop-up in New York was emblematic of how the brand is building Western distribution and awareness in parallel with its Asian core.

E.L.F. Beauty was arguably the most dramatic story in the industry in 2025, delivering +16.7% growth for the full calendar year, including a stunning +27.0% surge in the second half. With approximately $1.5 billion in revenues, E.L.F. remains much smaller than the industry giants, but its growth trajectory has been extraordinary. Its fiscal year ending March 2025 saw revenues climb by well over a quarter year on year, and the brand added nearly two full percentage points to its share of the U.S. mass cosmetics market. Its model of rapid, trend-attuned product development at accessible prices continued to attract consumers who elsewhere were tightening their spending. The company closed the fiscal year by announcing the acquisition of rhode, Hailey Bieber's skin care brand, for up to $1 billion, diversifying its portfolio with a high-growth, culturally resonant asset that extends its reach into prestige-adjacent territory.

Interparfums: Steady in a Normalizing Fragrance Market

Interparfums, the licensed fragrance specialist behind Coach, Lacoste, Montblanc, and other brands, delivered +2.5% growth to approximately $1.5 billion in revenues in 2025. The result masked a difficult U.S. environment, where full-year sales fell -6%, offset by strong European performance in Q4 with Lacoste growing +28% for the full year and Montblanc +22% in Q4 on the success of the new Montblanc Explorer launch. The company finished the year strongly, with Q4 global sales up +7%. Looking into 2026, management has guided for approximately flat growth, reflecting ongoing macroeconomic uncertainty and investment in newly acquired licenses including Off-White and Longchamp, with a more favorable 2027 outlook as major innovation pipelines build out.

The China Question: Still the Most Important Variable

A recurring theme across virtually every company in this analysis is China. The world's second-largest beauty market entered a period of consumer confidence challenges and structural changes in retail behavior that disrupted the business models of many global players who had spent a decade building exposure to the market.

For Estee Lauder, China and Asia travel retail were the primary drivers of multi-year decline. For Shiseido, the China repositioning effort weighed on Drunk Elephant and key prestige lines. For L'Oreal, North Asia showed meaningful Q4 recovery as the selective beauty market returned to growth, with L'Oreal Luxe posting double-digit Q4 gains in the region. Beiersdorf's La Prairie, one of the most China-exposed luxury skin care brands globally, saw sales decline in the high single digits for the full year, though Q3 showed sequential improvement with +1.6% growth. Amore Pacific and Puig, whose China exposure is more limited relative to their growth in broader Asia-Pacific and Western markets, were shielded from the worst of this dynamic.

The China recovery that many had hoped would accelerate in 2025 proved gradual and uneven. Signs of stabilization are present, but a full return to the growth rates that characterized 2021-2022 in China appears to remain some distance away. Companies that had concentrated exposure to the market continued to pay a price. Those that had diversified geographically or that had leaned into strong local market execution in Europe, the U.S., or Southeast Asia were comparatively insulated.

Fragrance: The Category That Kept the Industry Afloat

Across this group of companies, fragrance emerged as the single most consistent bright spot in 2025. Puig built its record year largely on the back of fragrance. Coty's prestige fragrance segment held up while color cosmetics faltered. Interparfums grew its European franchise on the strength of Coach, Lacoste, and Montblanc. L'Oreal's Luxe division was heavily supported by blockbuster fragrances from Yves Saint Laurent, Valentino, and Prada. Amore Pacific acquired the Maison Goutal niche fragrance brand through its Interparfums SA entity, signaling its own conviction in the category's longevity.

Consumer demand for fine fragrance has been one of the defining beauty trends of the past five years, and 2025 showed signs of some normalization at the high end of the market, with luxury fragrance facing the same Chinese consumer headwinds as prestige skin care. But the category's breadth, from ultra-premium niche to accessible fragrance mists, continued to generate growth opportunities for players able to operate across price tiers and geographies. The fragrance 'wardrobe' concept, where consumers collect multiple scents for different moods and occasions, appears to have extended the category's structural growth trajectory.

The Value Proposition Under the Microscope

One structural shift that 2025 results illuminate clearly is a growing bifurcation in consumer behavior. At one end, shoppers are trading down or at least scrutinizing value more carefully in mass beauty, leading to softness in categories like drugstore color cosmetics and mass body care. At the other, aspirational and prestige consumers continue to spend on skin care, fragrance, and beauty that feels indulgent or therapeutic.

E.L.F. Beauty's extraordinary performance sits at the value end of this spectrum, but it succeeds not by being cheap, but by being exceptionally responsive to trends and by offering genuine quality at a price point that requires no trade-off rationalization from the consumer. The brand's consistent share gains in U.S. mass cosmetics come almost entirely at the expense of heritage players who have been slower to innovate. Its acquisition of rhode extends this playbook into prestige-adjacent skin care.

At the prestige end, companies like Puig and Amore Pacific have shown that well-positioned brands with strong innovation pipelines and cultural relevance can grow meaningfully even in a cautious spending environment. The challenge for the middle tier, which includes much of Estee Lauder's portfolio outside of hero brands and La Mer, is that the market has become more ruthlessly meritocratic.

Looking Ahead: What 2026 Might Bring

The aggregate +0.5% growth in 2025 for these ten companies reflects a beauty industry that is healthy at its poles but under genuine pressure in the middle. The structural drivers that have supported the industry's outperformance relative to broader consumer goods over the past decade, including premiumization, digital commerce growth, the emergence of new beauty-consuming demographics in Asia, and the expansion of the fragrance category, remain intact. But the easy gains of the post-pandemic recovery period have been fully absorbed, and growth now requires genuine execution rather than simply riding a favorable macro environment.

Several key themes are likely to define 2026 performance. China's recovery trajectory will remain the single most important variable for the industry's largest players, particularly L'Oreal, Estee Lauder, Shiseido, and Beiersdorf's La Prairie. The impact of U.S. tariffs on imported beauty products represents a meaningful new headwind, with Interparfums estimating a direct impact and multiple companies citing tariff uncertainty in their outlooks. E-commerce and social commerce, particularly TikTok Shop and direct-to-consumer models, will continue to reshape distribution and brand discovery in ways that favor agile brands and disadvantage legacy retail-dependent ones.

The companies best positioned for 2026 appear to be those with geographic diversification, genuine brand equity in fragrance and skin care innovation, and the organizational agility to adapt their distribution and communication models to a rapidly evolving retail landscape. Puig, with its record results and strong momentum in both fragrance and makeup, enters 2026 from a position of notable strength. Amore Pacific has structural tailwinds from K-Beauty's global ascent. E.L.F. Beauty has a growth model that has proven remarkably durable. L'Oreal, despite the currency drag that masked its underlying momentum, retains its position as the market's benchmark and continues to invest aggressively in Beauty Tech and M&A.

For Estee Lauder and Shiseido, 2026 is a pivotal year of execution. Both companies have laid out credible turnaround frameworks, and early signs of H2 2025 stabilization provide some basis for optimism. But the margin for error is narrow, and the gap between their internal targets and current market expectations reflects just how much work remains.

The beauty industry's fundamental proposition to consumers, that investment in how you look and feel delivers disproportionate personal value relative to its cost, has not changed. What has changed is the competitive intensity, the pace of trend cycles, and the sophistication of consumers in evaluating that proposition. The winners of 2025 understood that. The companies still fighting their way back are learning it the hard way.