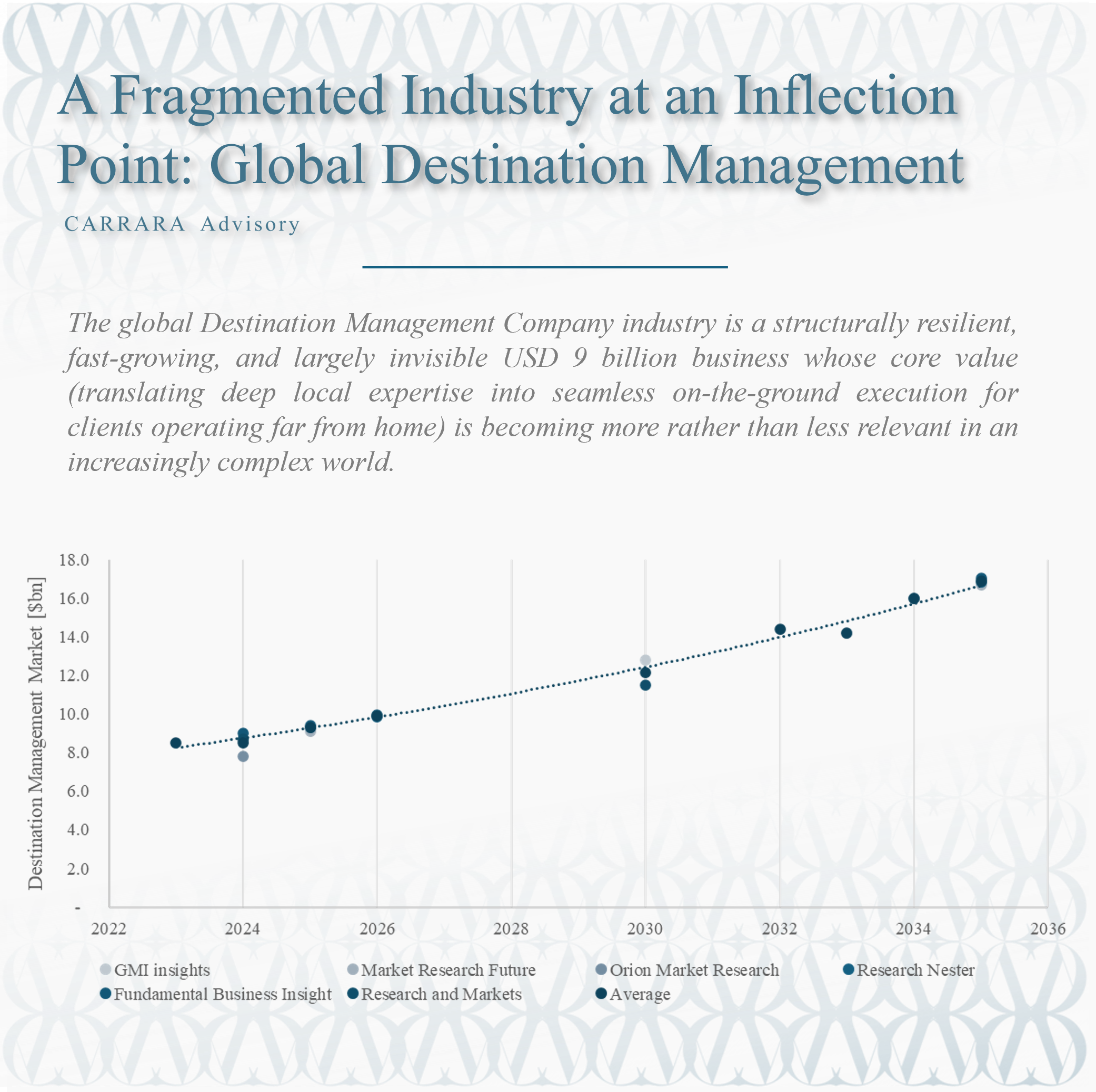

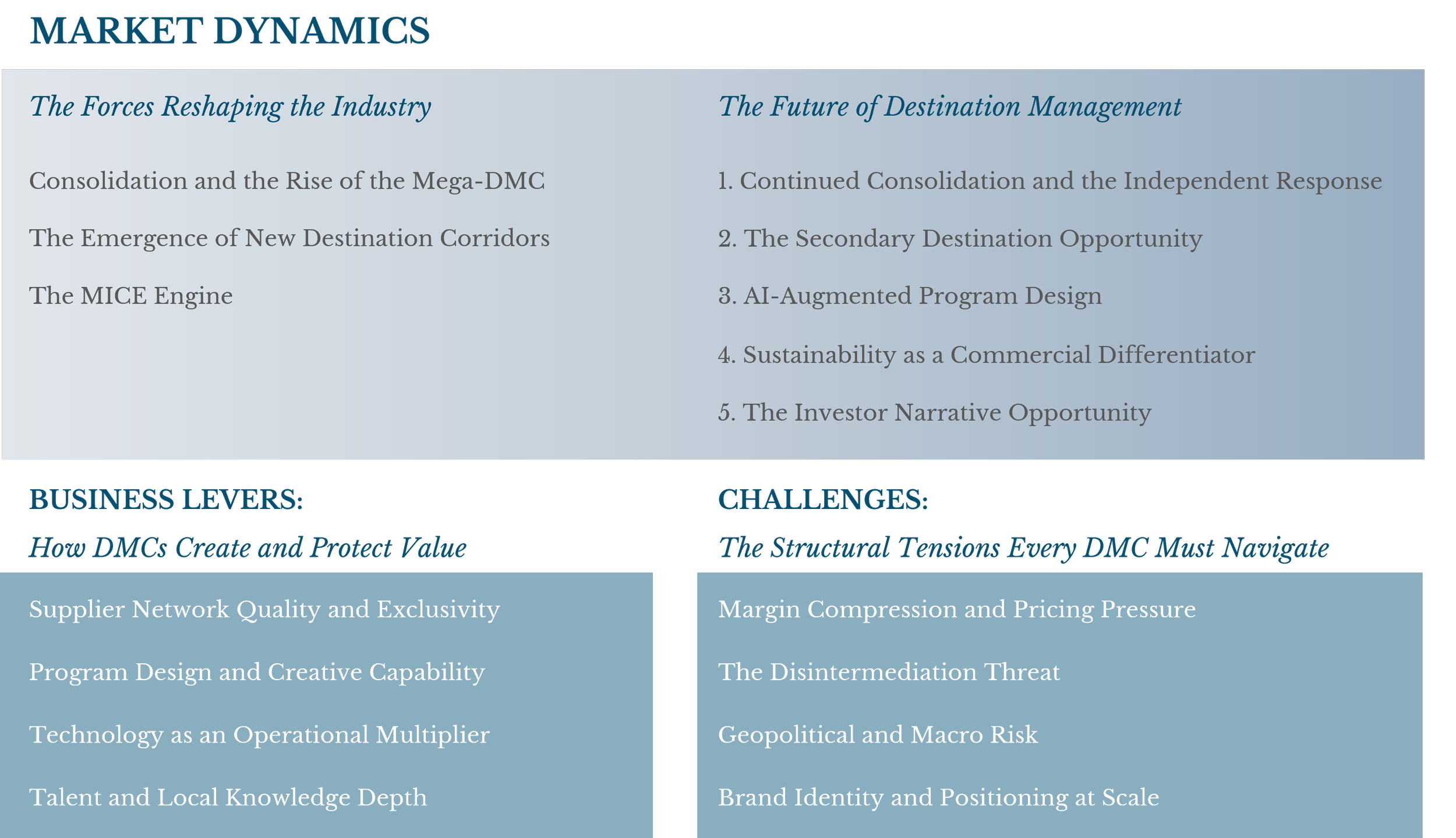

Market Dynamics: The Forces Reshaping the Industry

Consolidation and the Rise of the Mega-DMC

The most visible structural shift in the DMC industry over the past decade has been consolidation. Meeting planners and agency buyers have consistently narrowed their preferred vendor lists, favoring partners with multi-destination reach, investment-grade operations, and the ability to absorb risk at the program level. This has created enormous commercial pressure on single-destination independents and accelerated a wave of mergers, acquisitions, and network alignments.

The formation of Cohera in early 2025 is the most dramatic recent example, but it follows a decade-long trend. As ADMEI President Daniella Bikoulis noted at the close of 2025, "the growing trend of last-minute business, combined with shrinking budgets and rising expectations, will create incredible pressures" on smaller operators. Consolidation will continue, driven not just by commercial logic but by the increasing cost of technology, insurance, and compliance infrastructure that smaller players struggle to afford independently.

The counter-argument, made forcefully by independent operators, is that consolidation sacrifices the very thing that makes DMCs valuable: authentic local knowledge. "Living and working in New Orleans gives us a level of understanding that can't be scaled across a national network," as one long-standing independent operator put it. Both positions contain genuine truth, which is why the market continues to support a range of operating models rather than converging on a single dominant structure.

The MICE Engine

MICE tourism (Meetings, Incentives, Conferences, and Exhibitions) is by a significant margin the highest-value segment of the DMC market. It is also the fastest-growing. Corporate buyers have continued to invest in in-person gatherings as a deliberate strategic response to the over-reliance on virtual meetings that characterized the pandemic period. The incentive travel segment in particular has returned with exceptional vigor: programs are larger, budgets are higher, and the expectations for customization and memorable experience have increased substantially.

The event management segment alone accounted for over USD 3.6 billion in DMC revenues in 2023 and is on track to exceed USD 5.4 billion by 2032. For DMCs, MICE programs represent both the highest revenue opportunity and the highest operational risk. They are complex, time-sensitive, and reputation-critical. They are also the clearest proving ground for what DMC expertise really means: the ability to manage a 500-person program seamlessly across a destination the client has never visited.

The Emergence of New Destination Corridors

The geography of DMC demand is shifting in ways that create genuine competitive opportunity. Saudi Arabia has made the development of international tourism a national strategic priority, with AlUla alone onboarding multiple new preferred DMC partners in 2024 to handle growing inbound demand. The Gulf more broadly (particularly the UAE and Qatar) continues to invest in world-class MICE infrastructure. Central Asia, Eastern Africa, and secondary cities across Europe and Asia are all seeing meaningful growth in inbound demand.

For established DMC groups, these emerging corridors represent an expansion opportunity, but also a strategic test: the skills required to operate a mature destination are different from those required to pioneer a new one. The ability to navigate underdeveloped supplier ecosystems, uncertain regulatory environments, and infrastructure gaps demands a particular kind of operational resilience and local partnership capability.

Business Levers: How DMCs Create and Protect Value

Supplier Network Quality and Exclusivity

The single most important asset a DMC holds is its supplier network. The depth, exclusivity, and quality of relationships with hotels, transport operators, experience providers, venues, and local authorities determines what a DMC can offer that its competitors cannot. The best DMCs hold negotiated rates, access to inventory that is not publicly available, and informal relationships that allow them to solve problems (a room block released at short notice, a permit granted quickly, a supplier willing to go the extra mile) that no amount of money or technology can substitute for.

Building and maintaining this network is a long-term investment. It is not an asset that can be acquired quickly, which is one reason why DMCs with strong destination-level heritage are genuinely difficult to replicate. It is also an asset that can erode quickly if not actively managed, since supplier relationships require ongoing investment, senior relationship ownership, and commercial reciprocity.

Program Design and Creative Capability

The commoditization risk in destination management is real. If a DMC can only offer what any other operator can assemble from the same public inventory, it is competing on price, and that is a race no premium operator can win sustainably. The escape from commoditization lies in program design capability: the ability to create itineraries, experiences, and event concepts that are genuinely distinctive, culturally informed, and commercially compelling.

The best DMCs employ or develop genuine creative talent alongside their operational teams. Program design is not a sales function; it is a product function, and it should be treated as one. The shift from logistics coordinator to experience curator is the central strategic evolution of the DMC industry over the past decade.

Technology as an Operational Multiplier

Technology has historically been an underinvested area for many DMCs. The operational model (built on personal relationships, local knowledge, and human orchestration) has not traditionally demanded sophisticated digital infrastructure. That is changing rapidly. Modern DMC technology stack requirements now include real-time itinerary management platforms, supplier integration APIs, CRM systems capable of managing complex multi-program client histories, and data analytics tools that allow pricing, inventory, and margin management at the program level.

According to a recent Incentive Travel Index survey, 63 percent of respondents believe AI is being used effectively in incentive travel planning, and adoption is accelerating. DMCs that invest ahead of the curve in technology will gain compounding advantages: faster proposal generation, better margin visibility, lower operational error rates, and a data asset about client preferences that becomes increasingly valuable over time.

Talent and Local Knowledge Depth

In an industry where the product is ultimately a human service, talent is a fundamental business lever. The most valuable people in a DMC are not necessarily those with the most formal qualifications but those with the deepest and most current knowledge of their destination: who the right suppliers are, how the local bureaucracy works, what has changed in the last six months, and how to solve a problem that no playbook has anticipated.

Managing talent in a multi-destination DMC group is one of the most complex organizational challenges in the industry. The natural tendency is for each destination team to operate as an independent unit, with its own culture, standards, and commercial logic. Creating coherence across these units (shared service culture, consistent quality standards, group-level knowledge transfer) without destroying the local authenticity that makes each team valuable is the central people challenge of every DMC group at scale.

Challenges: The Structural Tensions Every DMC Must Navigate

Margin Compression and Pricing Pressure

The economics of destination management are under sustained pressure. Rising costs (particularly in staffing, insurance, and supplier inputs) are colliding with client expectations for competitive pricing and, in some market segments, flat or declining budgets. The ADMEI president noted in late 2025 that there is a "disconnect between stagnant or shrinking budgets and client expectations" that is creating real structural stress for operators across the market.

Margin management in the DMC business is complicated by the opacity of the pricing model. Most DMCs earn margin from a combination of service fees and net rates embedded in supplier contracts, and the relative weight of each varies by program type, client relationship, and destination. This opacity creates both opportunity (sophisticated operators can manage margin actively across the program) and risk, as clients who understand the model may negotiate more aggressively or seek to bypass the DMC for certain supplier categories.

The Disintermediation Threat

The growth of digital platforms, online booking tools, and AI-powered travel agents creates a structural disintermediation risk for DMCs, particularly in the leisure segment. If a traveler or even a corporate planner can increasingly self-assemble a destination experience using digital tools, the question of what a DMC adds becomes more acute.

The honest answer is that disintermediation is a real risk for the commodity end of the DMC market, meaning the kind of straightforward airport transfer, standard hotel selection, and generic experience booking that digital platforms can do perfectly well. But the higher the complexity, the higher the value, and the more important the local expertise, the more resilient the DMC's position becomes. A technology platform cannot manage the human dimensions of a crisis at destination. It cannot negotiate a venue owner out of a last-minute price increase. It cannot read a room and adjust a program on the fly. The DMC's defense against disintermediation is not to compete with technology but to invest in the capabilities that technology cannot replicate.

Geopolitical and Macro Risk

DMCs operate in destinations, and destinations are not immune to geopolitical disruption, natural disasters, public health events, and political instability. The pandemic was the most acute version of this risk in modern memory, but the ongoing reality of regional conflicts, climate-related weather events, and shifting regulatory environments means that risk management is a permanent operating challenge rather than an exceptional one.

The DMCs that handled the pandemic period best were those with the clearest crisis protocols, the strongest client communication capabilities, and the most resilient supplier relationships. Risk management is not a compliance function for a DMC; it is a core operational competency that clients (particularly in the corporate segment) evaluate carefully when choosing partners.

Brand Identity and Positioning at Scale

As DMC groups grow through geographic expansion and service diversification, they face a challenge that is deceptively difficult to solve: how to communicate a coherent identity when the business operates across many destinations, serves many client types, and encompasses many different service categories.

Operational excellence and local execution capability are critical differentiators, yet they are often difficult to articulate clearly to clients, partners, and investors. The result is that many DMC groups build substantial operational scale while remaining effectively invisible at the group level. Their reputation lives destination by destination, client by client, and program by program, which is both a strength and a strategic limitation.

Clarity of positioning is not a branding exercise for a DMC group. It is a strategic enabler of growth, partner trust, investor confidence, and internal coherence across a geographically dispersed organization. The DMC groups that are investing in this clarity today are positioning themselves for a different kind of competitive advantage, one that operates above the program level and creates durable commercial value.

The Future of Destination Management: Five Dynamics to Watch

1. AI-Augmented Program Design

The integration of artificial intelligence into the DMC workflow will accelerate substantially over the next three to five years. The most immediate applications are in program proposal generation, itinerary personalization at scale, and supplier inventory optimization. Longer term, AI tools will begin to reshape how DMCs manage client relationships, predict demand patterns, and price complex programs dynamically. The winners will be those who treat AI as an operational multiplier for human expertise rather than a replacement for it.

2. Sustainability as a Commercial Differentiator

ESG requirements are moving rapidly from aspiration to procurement criterion across the corporate segment. DMC clients (particularly large multinationals) are increasingly requiring demonstrable sustainability credentials as a condition of supplier selection. DMCs that can credibly demonstrate carbon accounting, community benefit programs, and responsible sourcing will command a meaningful competitive advantage. Those that treat sustainability as a checkbox will find themselves disadvantaged as these requirements become standard.

3. The Secondary Destination Opportunity

Overtourism in primary destinations (Venice, Bali, Santorini, Barcelona) is creating genuine political and logistical constraints on volume. At the same time, sophisticated travelers are actively seeking less-visited destinations with authentic cultural experiences. For DMCs, this convergence creates a significant opportunity: the ability to develop compelling product in secondary destinations ahead of the demand curve, establishing supplier relationships and operational infrastructure before competitors arrive.

4. Continued Consolidation and the Independent Response

The consolidation trend will continue, driven by technology costs, procurement concentration, and the commercial advantages of multi-destination reach. But the independent DMC is not disappearing. Its competitive position rests on something that consolidation cannot easily replicate: genuine local ownership, deep community embeddedness, and the kind of cultural fluency that comes from living in a destination rather than merely operating in it. The most successful independents will be those who make this distinction explicit and who find the right network relationships to access volume without sacrificing quality.

5. The Investor Narrative Opportunity

Private equity and institutional capital have been circling the DMC space with increasing interest, recognizing the structural growth dynamics and the durable competitive advantages that the best operators have built. The challenge has been the difficulty of valuing and communicating these advantages clearly. DMC groups that invest in articulating a clear investment narrative (one that explains not just what they do but how they create durable value and why their competitive position is defensible) will be best positioned to attract capital on favorable terms and to execute strategic transactions from a position of strength.

Conclusion: Why Understanding DMCs Matters More Than Ever

The destination management industry sits at the intersection of some of the most powerful dynamics in the modern economy: the global expansion of travel and tourism, the growing demand for personalized and authentic experiences, the complexity of operating across borders and cultures, and the acceleration of digital tools that are reshaping how services are delivered and competed for.

DMCs are not a legacy category threatened by disruption. They are a structurally resilient service model whose core value (deep local expertise, trusted supplier networks, and human orchestration of complex experiences) is becoming more rather than less relevant as the world becomes simultaneously more connected and more complex.

The DMC groups that will lead the next decade are those that invest simultaneously in operational excellence at the destination level and strategic clarity at the group level, that treat technology as an enabler rather than a threat, that build sustainability into their core offering rather than bolting it on, and that communicate their value with the same sophistication they apply to executing their programs.

The industry has built something genuinely valuable. The next challenge is to explain it.

About the Authors

This article was produced by senior advisors specializing in positioning, brand architecture, and strategic communications for complex services groups.