The first quarter of 2026 has offered a revealing and at times sobering update on the state of the global beauty industry.

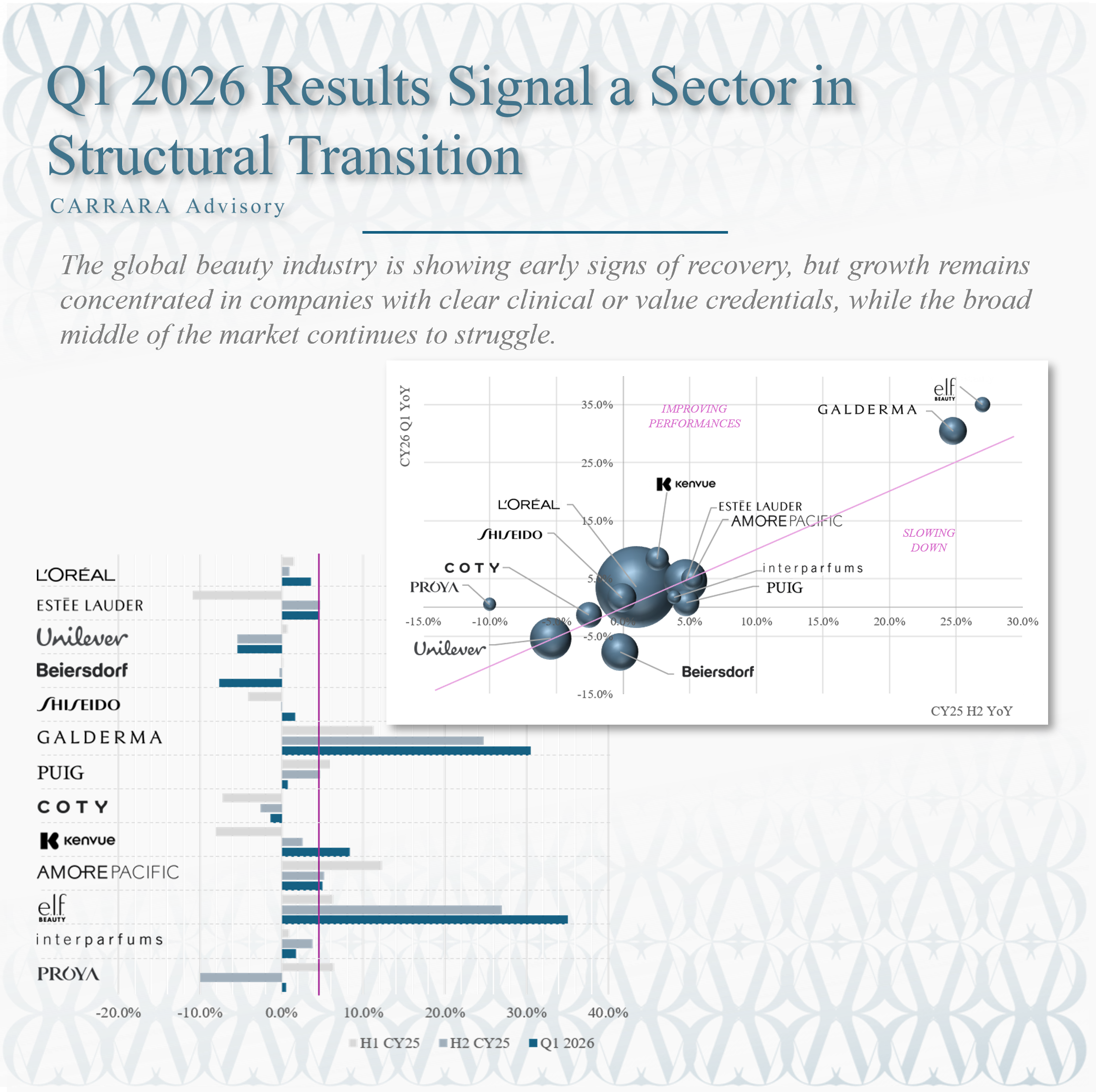

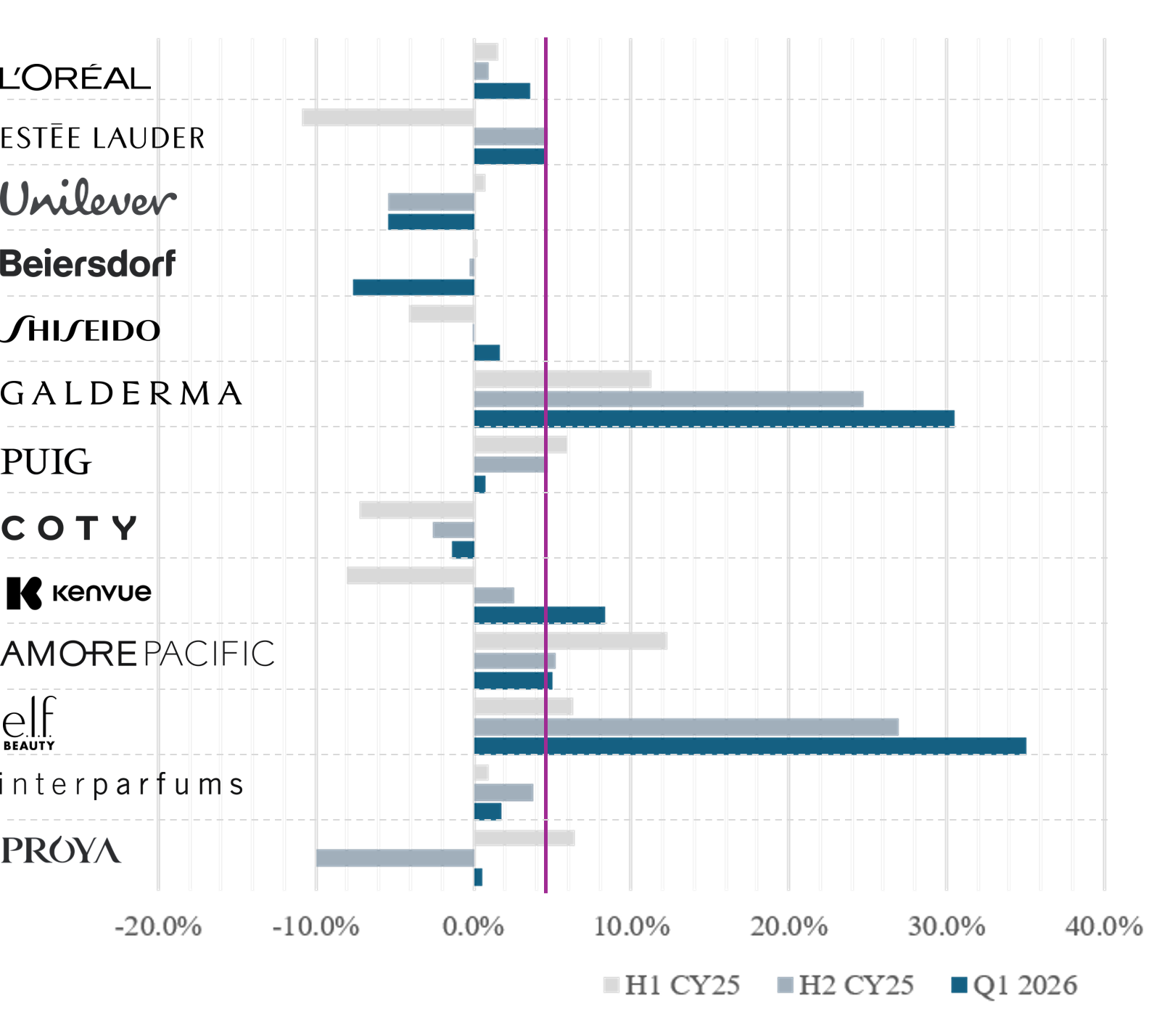

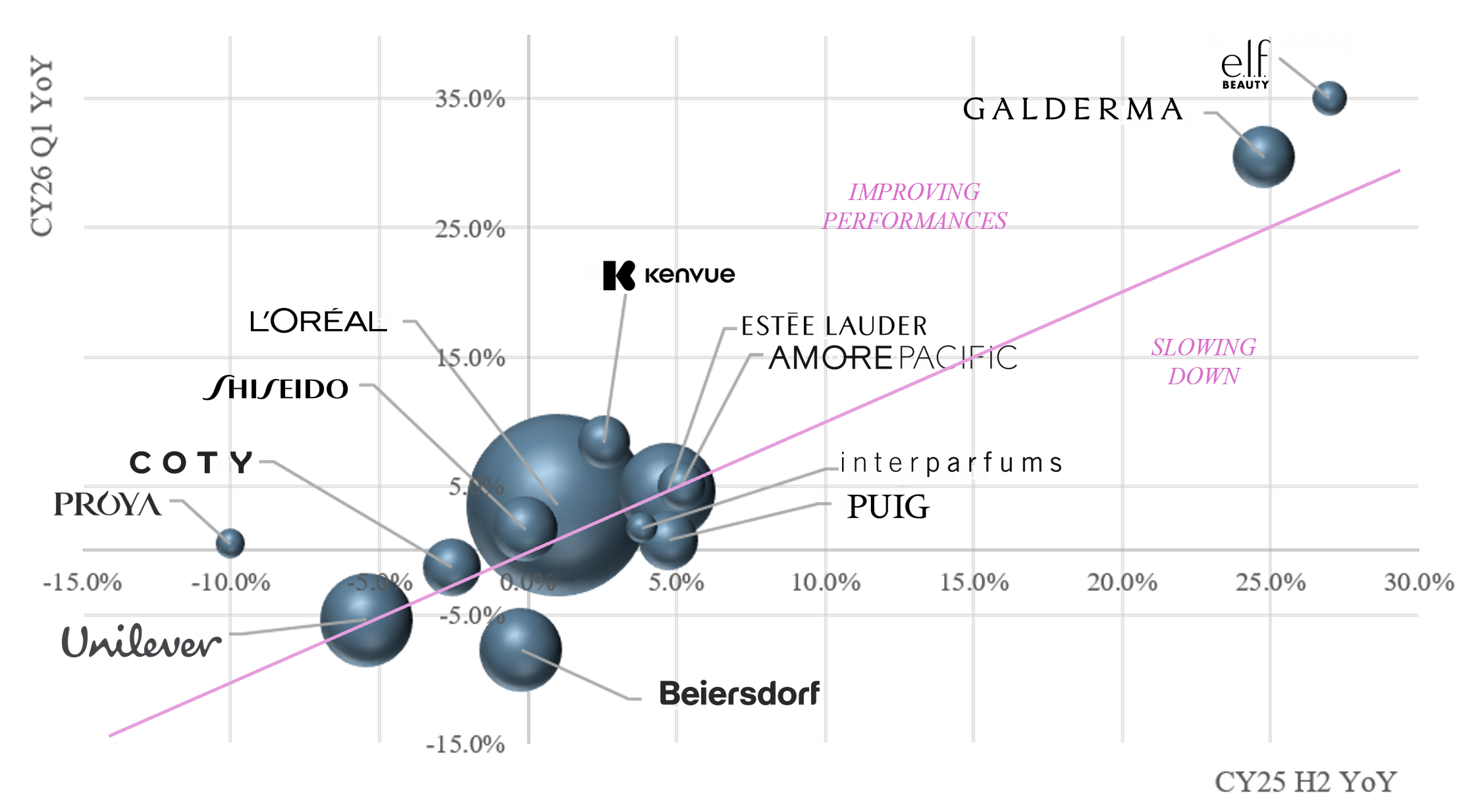

Taken together, the thirteen companies tracked by CARRARA Advisory posted aggregate reported revenue growth of 2.6% -- a meaningful step up from the 1.7% recorded in the second half of 2025 and a clear reversal from the near-flat performance of H1 last year. At nearly $125 billion in combined yearly revenues, this group serves as CARRARA's primary tool for sense-checking the health of the global beauty industry.

There is no single authoritative real-time indicator for global beauty performance: market data providers publish with a lag, and no solid and reliable index captures the full breadth of the sector. What a carefully curated portfolio of publicly reporting companies can provide, however, is a timely and multi-dimensional read on where the industry actually stands.

This quarter CARRARA has expanded its coverage to thirteen companies, adding Galderma, PROYA and Kenvue alongside the existing ten, with the explicit goal of broadening the lens across categories, price tiers and geographies. The universe now spans injectable aesthetics and therapeutic dermatology at one end, mass cosmetics, fragrances and personal care at the other, and everything in between; it includes companies with primary exposure to China, Korea, Europe and the United States; and it ranges from ultra-premium luxury to accessible value. The divergences across these thirteen companies are now sharper than they have been at any point in the past three years -- and it is precisely that breadth of coverage that makes those divergences analytically meaningful.

The headline number, however, masks a story that is far more nuanced. The beauty market at large is not recovering uniformly. What is emerging instead is a bifurcated landscape defined by two accelerating poles: clinical and science-backed efficacy at one end, and accessible value at the other. The comfortable middle ground that once sustained many of the industry's largest and most storied franchises is shrinking.

A Sector Confronting Its Own Slowdown

Before turning to individual company results, the trend line deserves careful attention -- because it tells a story that the industry has rarely had to confront.

For more than two decades, global beauty has been one of the most reliably growing consumer sectors in the world, expanding at a compound rate of roughly 4 to 5% annually through economic cycles, technological disruption, and shifting consumer preferences. The only meaningful interruptions to this trajectory were the 2008-2009 financial crisis, when discretionary spending contracted sharply, and the COVID-19 pandemic in 2020, when physical retail shutdowns temporarily paralyzed large segments of the market. In both cases, the industry recovered quickly and resumed its long-run pace.